{kind=link}

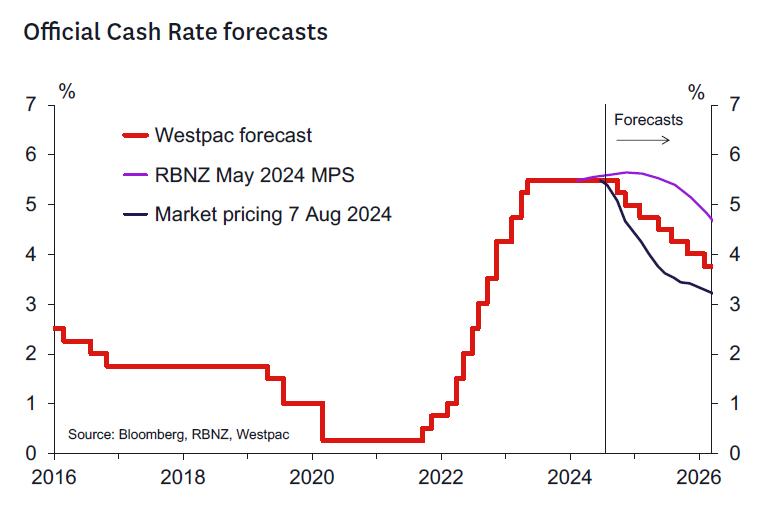

- We expect the RBNZ will leave the OCR at 5.5% at the August Monetary Policy Statement.

- We expect a significant revision in the forward view for the OCR consistent with potential easing in October and November, leaving the year end OCR at 5%.

- We also expect significant downward revisions to the 2025 and 2026 OCR profiles.

- We expect significant downward revisions to the RBNZ’s growth projections for 2024.

- The RBNZ’s short term CPI forecasts will likely be reduced, consistent with the downside surprise seen in the June quarter CPI.

- Further out, inflation will continue to fall more slowly – although the CPI may now be forecast at 2% somewhat earlier than in the May Statement.

Key developments since the May Monetary Policy Statement.

Overall, a broad range of activity and pricing indicators have pointed to a more favourable inflation outlook compared to what the RBNZ had contemplated at the time of the May meeting. We think the following are the key developments.

- Inflation (↓): The CPI rose a less than expected 0.4%q/q in Q2, lowering annual inflation to 3.3% and making it likely that inflation will move back inside the target band in Q3. The RBNZ will likely welcome the lower outcome, as the more favourable narrative will feed back into inflation expectations. However, the RBNZ will be concerned that all the downside surprise was attributable to lower-than-expected prices for tradables (mostly goods), whereas non-tradables (mostly services) prices continued to inflate at a pace that is inconsistent with inflation returning to the midpoint of the target band.

- Inflation expectations/pricing indicators (↓): Survey measures of firms’ intentions to raise prices (such as those in the QSBO and ANZ business surveys) have moved markedly lower in recent months to levels that are now just a little above their historical ranges. Direct measures of business and consumer inflation expectations have also continued to move lower.

- Activity (↓↓): While GDP grew 0.2% in Q1, in line with the RBNZ’s expectations, high frequency top-down indicators (such as the Business NZ PMIs) suggest that the economy has likely contracted significantly in Q2. Westpac estimates a 0.6% decline in GDP, in sharp contrast to the RBNZ’s forecast of modest growth. And at this stage there is little sign that the economy is going to rebound in Q3. This means that the “output gap” – a key variable in the RBNZ’s inflation forecast framework – is likely to be tracking more negatively than was forecast, implying weaker medium-term term pressures on domestic inflation.

- Labour market (↓): The Q2 surveys provided no surprises for the RBNZ, at least as far as the key headline numbers are concerned. The unemployment rate increased to 4.6% and private labour costs increased 0.9%q/q in Q2 – exactly in line with the RBNZ’s May projections. A 1.2% q/q decline in hours worked may have been a downside surprise (the RBNZ does not forecast this series) and may add to the RBNZ’s sense that GDP likely contracted in Q2 (especially as the employer-based QES survey also reported a 0.9%q/q decline in hours paid).

- Housing market/population growth (↓): Reflecting the broader malaise in the economy, the housing market has remained weak in recent months with a surplus of listings causing house prices to nudge lower. Meanwhile, the migration cycle appears to be turning down more quickly than the RBNZ had forecast in May, suggesting less support for the housing market than had been suggested by earlier forecasts. Lower mortgage rates and interest rate expectations could be a significant offset, however.

- Global growth (→): We doubt the RBNZ’s assumptions for the global growth outlook has changed much in recent months. They may discuss some downside risks to growth in China, especially as far as consumer activity has concerned, and given recent equity market volatility. There has been some softening of activity indicators in Europe of late. The US economy has continued to grow at a steady pace, albeit not sufficient to prevent a gradual uptrend in the unemployment rate. Lower official interest rates offshore could be seen as a supportive factor.

- Commodity prices (→): Commodity prices have been a mixed bag since May. Dairy prices are little changed, while meat prices have improved slightly (albeit remaining very low in the case of sheep meat). Log prices have remained low after falling sharply in April, while aluminium prices have fallen sharply.

- Financial conditions/exchange rate (↑↑): Financial conditions have eased markedly in recent months as wholesale interest rates have moved to anticipate significant policy easing in both New Zealand and the US. In addition, the trade weighted exchange rate (TWI) currently sits at 69.8, versus the RBNZ’s medium-term assumption of 71.0.

The communications objective.

We think the RBNZ will be aiming to deliver a “hawkish cut” to their OCR outlook while NOT cutting the OCR, thus sanctioning some – but not all – of the easing of monetary conditions seen in recent months. They will be setting the scene for cuts in October and November of 50 bp in total and leaving open the option to scale easing either up or down should the data or financial conditions warrant. The RBNZ will be reluctant for the market to run any further ahead of it than it currently is. We suspect the RBNZ has no fixed view on the longer-term path for the OCR given the significant uncertainties ahead.

Scenarios.

We see three main scenarios and one outside scenario:

- Baseline case (50% probability): the RBNZ leaves the OCR unchanged but indicates at least one 25 bp cut and a 50% chance of a further 25 bp cut by year end (this would be represented by a Q4 OCR forecast in the 5.1-5.2% range). The forward profile will likely be revised down such that the OCR will be implied to be between 4.25 and 4.5% by end 2025.

- Hawkish case (30% probability): the RBNZ leaves the OCR unchanged, and the projection implies just one 25 bp cut in November 2024 (i.e., a Q4 OCR forecast in the 5.35-5.45% range). The forward profile would be consistent with 2-3 cuts in 2025 leaving the OCR in the 4.5-4.75% range by the end of 2025.

- Dovish case (15% probability): the RBNZ cuts the OCR by 25 bp and indicates two further 25 bp cuts in 2024 taking the OCR to 4.75% by year end (i.e., a Q4 OCR forecast in the 4.9-5 % range). The forward profile will be revised down to reach short run neutral of around 3.75-4% by end 2025.

- A super dovish case (5% probability): the RBNZ cuts the OCR by 25 bp and indicates a total of 100 bp by end 2024 including one 50-point cut – likely in November. This would see the Q4 OCR forecast in the 4.8-4.9% range. The RBNZ would indicate the possibility of cutting the OCR to their long run neutral level of 2.75- 3% by the end of 2025.

Review of the June 2024 labour market reports.

Today’s survey results showed that the labour market is continuing to soften, but no faster or slower than the RBNZ was anticipating. The unemployment rate rose from 4.4% to 4.6% for the June quarter, in line with the RBNZ’s forecast in its May Statement. The household survey showed a surprising lift in employment, though this was most likely payback from the surprisingly weak result in the March quarter. Employment has risen by just 0.6% over the last year, far less than what was needed to absorb the 2.6% growth in the working-age population.

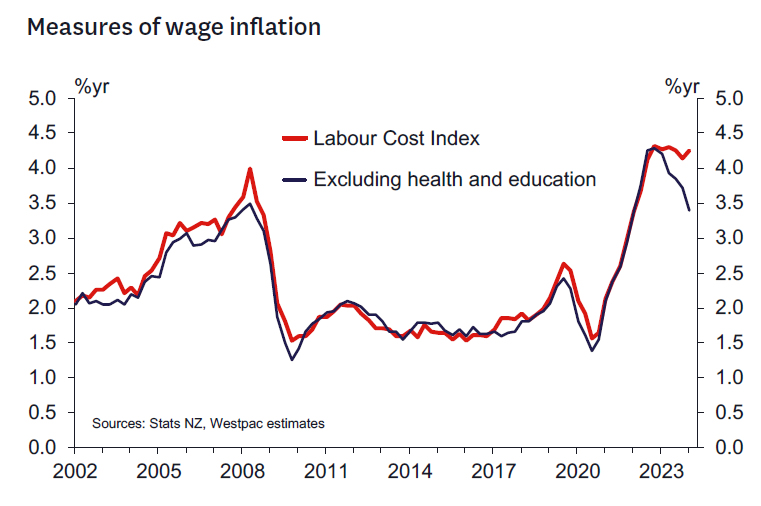

Despite the increasing slack in the labour market, wage inflation has been slow to reflect this. The Labour Cost Index rose by 1.1% for the June quarter, with the annual growth rate actually ticking up slightly to 4.2%. Private sector wages rose by 0.9% for the quarter, in line with the RBNZ’s forecast.

The overall wage index continues to be boosted by pay increases in the health and education sectors, which were agreed by the previous government and implemented in stages. We estimate that excluding these sectors, labour costs rose by 3.4% in the year to June. That pace has slowed from its highs, but is still some way above what would be consistent with the RBNZ’s 2% inflation target. Wage growth will be of interest to the RBNZ, given that much of the remaining ‘stickiness’ in inflation relates to domestic services where labour is a major input cost.