{kind=link}

U.S. Highlights

- Nonfarm payroll gains came in lower than expected in July, with the unemployment rate heading higher. The numbers add to other data suggesting that the U.S. labor market is losing steam.

- While the Federal Reserve held rates steady at their July meeting as widely expected, Chair Powell gave the strongest indication yet that a September rate cut is on the table.

- The manufacturing sector continued to struggle, as the ISM manufacturing index remained in contraction territory.

Canadian Highlights

- This week’s market action was influenced by events south of the border. The Fed decision and weak U.S. jobs report lead Canada’s 10-year and 5-year government bond yields more than 30 basis points lower.

- The key Canadian economic report, monthly GDP by industry, exceeded expectations and solidified stronger-than-expected growth in the second quarter.

- Looking ahead to next week’s jobs report, the Bank will likely be focused on the degree of slack in the labour market as they calibrate the pace of interest rate cuts.

U.S. – It’s A Different World

The main highlights of the week were developments in the labor market and a mid-week update from the Federal Reserve. Several reports showed that conditions in the labor market were cooling, while the Fed largely lived up to expectations by holding rates steady. Their signals about a possible cut at the September meeting were generally of more interest to markets. In response to the September signal, stock markets rallied, and bond yields pulled back. This morning’s jobs number was even more of a market mover, with 10-year yields down 13 basis points relative to yesterday’s close.

What a difference a year makes. The U.S. economy today, with annualized growth slowing from about 4% towards a more trend-like 2%, inflation down and unemployment ticking up, looks starkly unlike it did a year ago according to Fed Chair Powell. After issuing a statement keeping the policy rate unchanged, at his press conference, Powell noted that last year, it was a completely different economy with higher inflation and a robust job market. Now, he notes, on the employment front, indicators show the job market has gradually normalized from “overheated” conditions and the Fed is able to weigh prices and the labor market more equally as inflation has cooled.

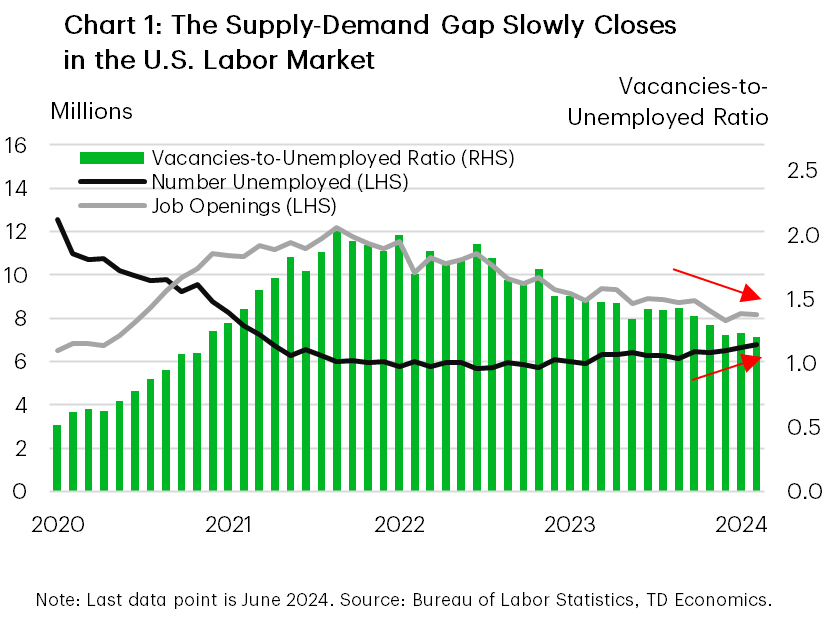

Reports out this week supported his statements on the job market. First up, the more backward-looking JOLTS data showed that the number of job openings in June inched down relative to May. While there are still plenty of jobs available relative to the more than 6.8 million unemployed job seekers in June — the gap has narrowed with the vacancies-to-unemployed ratio falling relative to its value in May (Chart 1). Other elements of the report also supported a softening labor market narrative – the hires rate ticked down and the quits rate was unchanged from May’s downwardly revised 2.1% (which is below where it was immediately prior to the pandemic). Additionally, the Employment Cost Index (ECI) report, which the Fed watches closely for wage trends, slowed at a faster-than-expected pace in Q2.

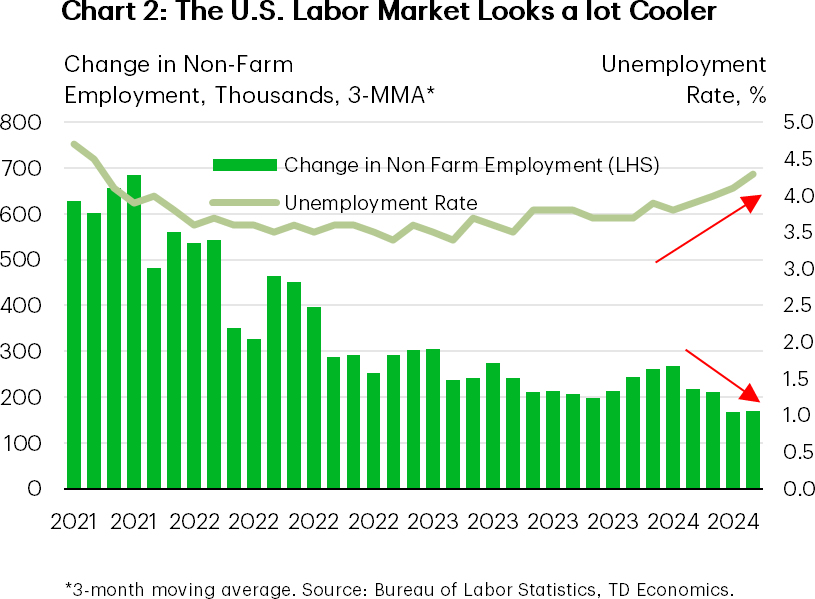

The signal from the more recent July payrolls report was generally in line with the JOLTS and ECI data. The economy added 114k jobs in July, missing expectations (Chart 2). The unemployment rate rose for the fourth consecutive month and annual wage growth decelerated to the slowest pace in over three years. Together, the three employment reports suggest that demand for workers continued to slow and add further evidence that the labor market is cooling.

On the production side, the ISM Manufacturing Index declined again in June. The series fell 1.7 points to 46.8, marking its fourth consecutive month in contraction territory after a short-lived reprieve in March. Demand continued to slow and output conditions worsened. Persistent contraction in the manufacturing sector alongside slowing consumer demand, present downside risks to US growth, which has already come off the above trend pace of last year.

As Chair Powell hinted at, the U.S. economy is in a different world now. As both sides of the Fed’s dual mandate come into sharper focus, a September cut is almost a guarantee and the chance for three rate cuts this year has certainly risen.

Canada – Strong Second Quarter Unlikely to Move the Needle on Rate Decision

This week’s market action was heavily influenced by the U.S. Federal Reserve’s interest rate decision, Chair Powell’s subsequent press conference, and Friday’s employment report. Canada’s bond market mirrored the rally of its southern counterpart, rising throughout the week and accelerating on Friday. Given the inverse relationship to prices, Canada’s 10-year and 5-year government bond yields fell by roughly 30 basis points.

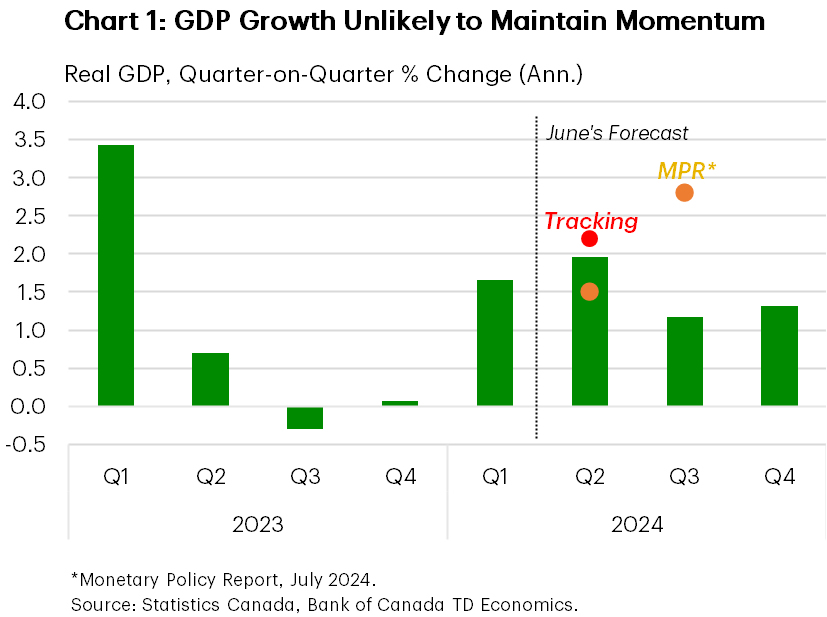

On Canada’s economic front, the key report was the monthly GDP by industry. Growth exceeded expectations, showing a 0.2% month-on-month growth in May, with the advance estimate for June suggesting a 0.1% increase. Assuming no revisions, this report solidifies expectations that second-quarter GDP will be stronger than previously anticipated, around 2.2% annualized, and growth in the third quarter is now looking a bit stronger than we had expected at the time of our June forecast. The Bank of Canada (BoC), on the other hand expects a solid out turn for the economy in Q2, forecasting 2.8% growth in its recent Monetary Policy Report (Chart 1).

Economic growth was broad-based in May, with both goods-producing and services-providing sectors expanding. The most significant contributions came from non-durable manufacturing, particularly petroleum refineries, which rebounded after maintenance work in April. On the services side, aside from the public sector’s significant contribution, the largest impacts came from accommodation & food services as well as finance & insurance, driven by investment activity in bonds and mutual funds. An interesting detail highlighted by Statistics Canada was the increase in arts, entertainment, & recreation sector, which was bolstered by three Canadian teams playing in the NHL playoffs in May. While these contributions are noteworthy, some of them share a common characteristic of being temporary effects. So while the report shows that there is still resilience in the economy, the momentum is not strong enough to push economic growth above trend levels.

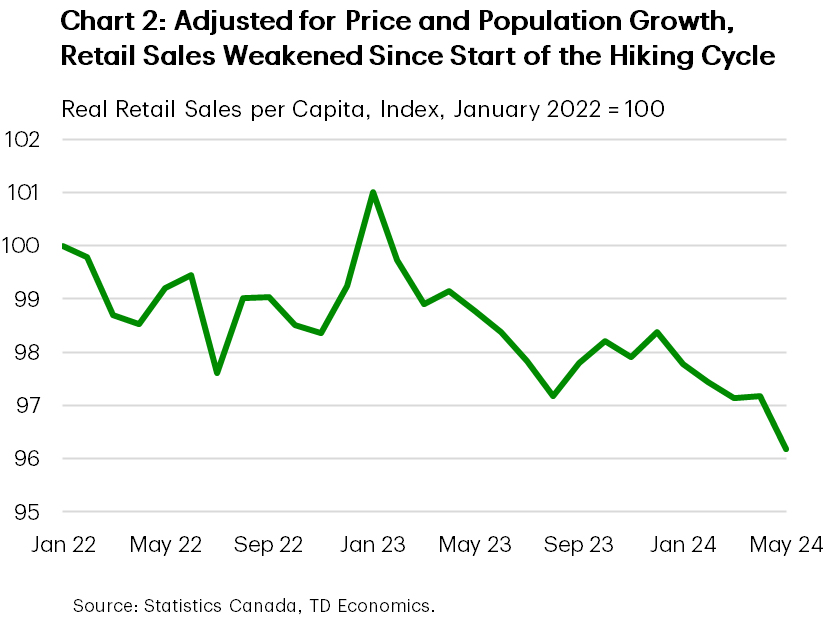

For another perspective, consider the state of the Canadian consumer. Higher frequency data on consumption, including spending at retail stores and restaurants, as well as our own card spending data, indicates a more cautious consumer who may still be spending, but without extravagance. Furthermore, one factor masking consumer weakness is population growth, which has exceeded estimates for several quarters and partly explains positive economic surprises. In fact, when adjusted for price and population gains, retail spending has weakened since the start of the Bank’s hiking cycle and contracted for most of this year (Chart 2). With new government restrictions on non-permanent residents taking effect, slower population growth is likely to become a headwind for the economy.

Next week it’s Canada’s turn for jobs numbers. Canada has been seeing cooler labour market conditions for a while now. The Bank will be focused on the degree of slack in the labour market and wage growth trends as they calibrate the pace of interest rate cuts. Market consensus suggests that the BoC is likely to proceed with a third consecutive rate cut in September.