. Last month’s reading was revised down by about 30k. The unemployment rate unexpectedly rose to 4.3%, the highest since Oct 2021, and hourly earnings only rose by 0.2% m/m (3.6% y/y). It’s a big disappointment across the board that followed on a long streak of weak(er) data, including yesterday’s, and adds to a growing sense of the US economy & labour market rapidly losing momentum.){kind=link}

Markets

Markets are trembling. US payrolls missed expectations by a significant margin as employment only grew by 114k (175k consensus). Last month’s reading was revised down by about 30k. The unemployment rate unexpectedly rose to 4.3%, the highest since Oct 2021, and hourly earnings only rose by 0.2% m/m (3.6% y/y). It’s a big disappointment across the board that followed on a long streak of weak(er) data, including yesterday’s, and adds to a growing sense of the US economy & labour market rapidly losing momentum. The Fed on Wednesday stopped short of announcing a September rate cut but markets fear policymakers are behind the curve. US money markets sharply rose easing bets with more than 100 bps of cuts priced in for 2024 alone. That implies at least one 50 bps rate cut, something Powell just two days ago said they were not considering. He did keep the door ajar: “If we see something that looks like a more significant downturn [in the labour market], that would be something that we would have the intention of responding to.” US yields at some point dropped a whopping 30 bps at the front before cutting losses to a still-massive 19 bps. The 2-yr yield tanked to the lowest level since June 2023 (3.95%) with technically little in the way to 3.55% (March 2023 low, regional banking crisis). The 10-yr (-12 bps, 3.85%) tested the YtD/December 2023 at 3.81%. A break paves the way for a return to 3.64%-3.66%/3.50%. Bund yields got caught in the slipstream, dropping between 4.6 and 10 bps in a similar curve shift. The 2-yr is attacking the YtD low at 2.35%, the 10-yr lost support at 2.20% and has intermediate support at 2.08% as a final hurdle ahead of the 1.89% December 2023 low. Stocks sold off in Europe (-2.2%) as well as in the US. Risk aversion and earning misses by the likes of Intel and Amazon makes the Nasdaq go belly up. The tech-heavy index (-2.5%) loses support at 1700. The S&P500 (-1.6%) gaps below 5400 support. The VIX volatility index rises to the highest level since October 2023. Unlike yesterday, the dollar is unable to offset the interest rate support losses through the vulnerable market climate. It is losing against peers with EUR/USD jumping towards the 1.09 barrier, DXY falling off a cliff to 103.43 in the biggest move in 9 months and USD/JPY hitting the lowest level since mid-March at 147.6. EUR/GBP heavily tested the 0.85 barrier but for now is not pushing through. Sterling does gain against a weak dollar with GBP/USD reversing about 75% of yesterday’s decline (1.282).

News & Views

Huang Yiping, a key advisor to the Chinese central bank, was unusually vocal on what he believes are insufficient policies to get the economy steamrolling again. Huang said that authorities should change their focus from investment and exports to domestic consumption. He suggested offering cash handouts as well as take a looser stance vs fiscal health (e.g. by dropping the 3% budget deficit rule). Huang proposed an inflation target of 2 to 3% for the central bank instead of regarding 3% implicitly as a ceiling. Huang suggested the central bank adopt the aggressive policies taken by the likes of the Fed and ECB to prop up the economy. But the PBOC is wary to do so, given that it is also tasked with preserving currency stability. USD/CNY by mid-July hit an 8-month high around 7.28. The pair witnessed some sharp swings over the past few days, including a dollar-driven sharp drop to 7.18 currently.

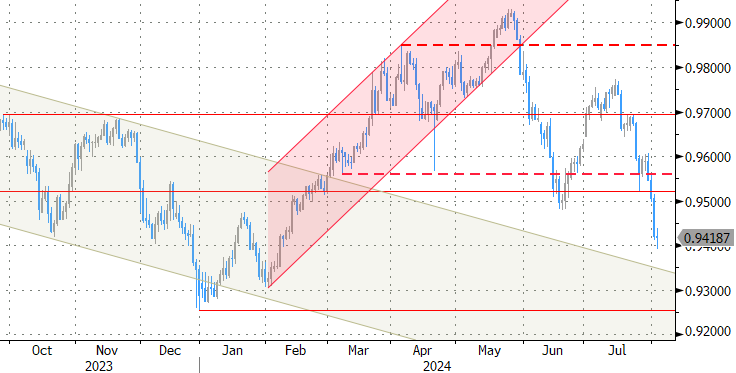

Swiss inflation eased by 0.2% m/m in July. The yearly figure came in at 1.3%, matching the June reading. Both numbers were exactly as expected. The core gauge (ex. fresh and seasonal products & energy) was unchanged too, at 1.1%. Swiss Statistics said that package holidays, air travel and clothing saw prices falling, while the costs of hotels and fruit and vegetables rose. The Swiss National Bank was among the first to cut rates in March of this year. It did so again in June, to 1.25%. With inflation steady and within the target range of 0-2%, the SNB is expected to deliver a third cut in September. It doesn’t need to worry about a weak CHF – as it did back in May – as the recent sharp risk-off triggered some major safe haven flows towards the currency. EUR/CHF went from the 0.975 area mid-July to 0.94 earlier today. Barring a brief episode at the start of this year, that’s the strongest CHF level in decades.

Graphs

Vix volatility index jumps to highest since October last year amid market tremors

US 2-yr yield slides to lowest level since June 2023 as markets fear Fed is behind the curve

EUR/CHF: Swiss franc enjoyed strong safe haven flows in recent days. With stable inflation, SNB seems ready to cut again in September

Nasdaq opens below 17k support barrier on fears the economy is slowing down faster than expected