{kind=link}

Summary

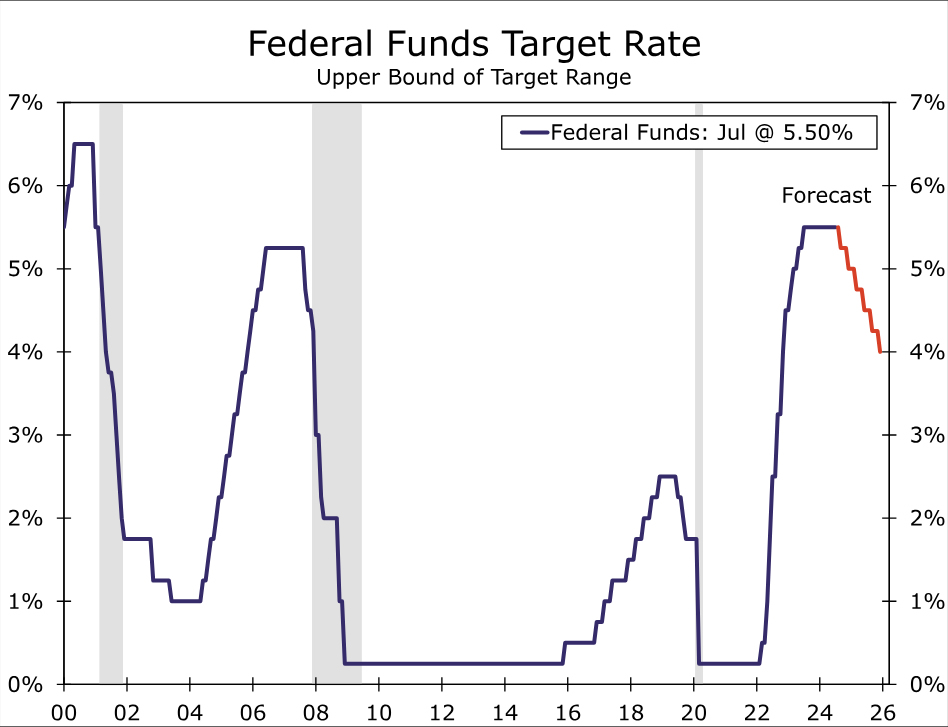

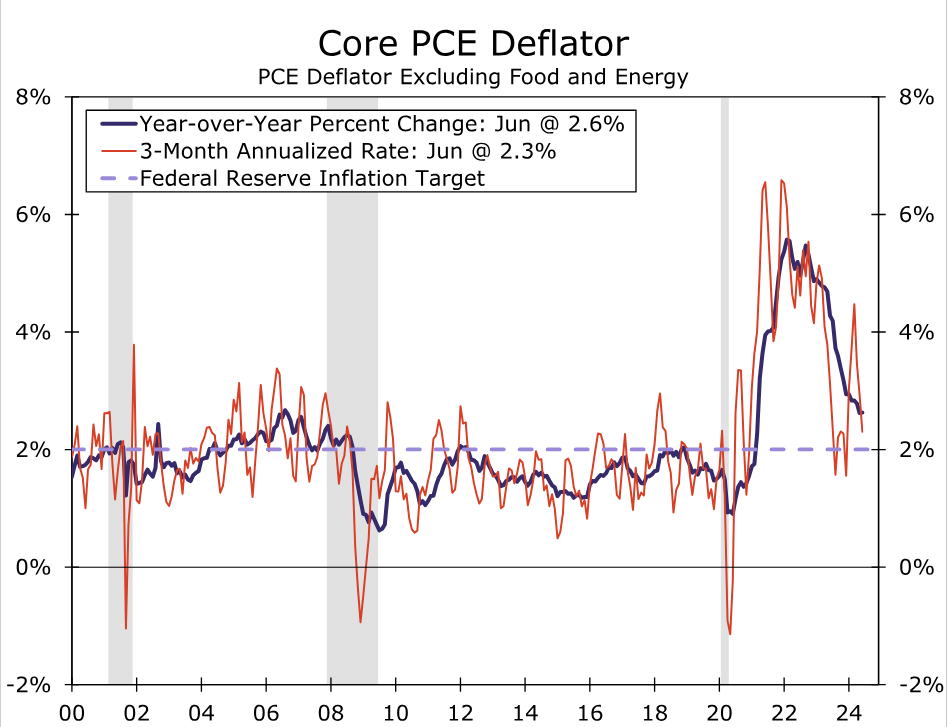

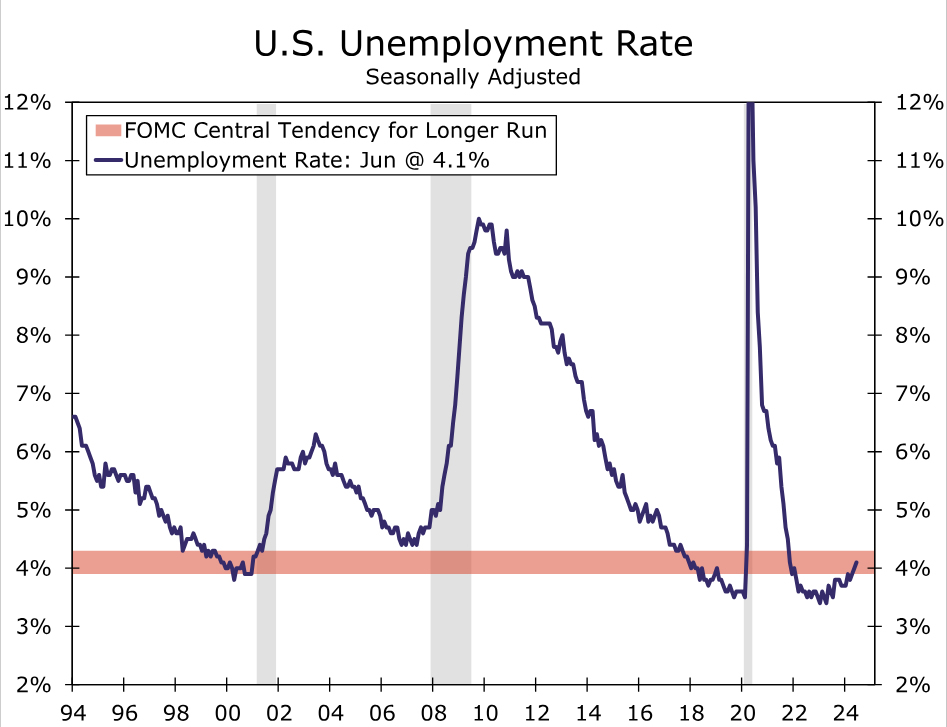

As was widely anticipated, the FOMC left the fed funds rate unchanged at the conclusion of today’s meeting, but it opened the door to potentially easing policy at its next meeting on September 18. While inflation remains above the FOMC’s 2% target, it has fallen significantly since the Committee last raised rates a year ago. At the same time, the labor market has cooled sufficiently and now resembles its pre-pandemic state. In its post-meeting statement, the FOMC noted the improving balance between its employment and inflation goals and emphasized it is growing more mindful of the risks to the labor market by noting it is “attentive to the risks to both sides of its dual mandate”, rather than previously only noting its attention to inflation risks.

We suspect today’s decision, post-meeting statement and Powell’s press conference statements reflect a compromise among the Committee members. While some more dovish members were likely inclined to reduce the policy rate at today’s meeting, more hawkish members are likely wanting to see more data. To thread the needle, we think Chair Powell arrived at a compromise: hold rates steady at this meeting, but send overt signals to the market and broader public that the base case is for rate cuts starting soon. We look for the FOMC to cut the fed funds rate by 25 bps at its next meeting, with a further 25 bps cut in December and an additional 100 bps of easing in 2025.

FOMC Sits Tight but Signals Rate Cuts Are Coming Soon

The FOMC made no policy changes at the conclusion of today’s meeting, but opened the door to a rate reduction as soon as its next meeting on September 17-18. For a year now the FOMC has left the fed funds rate unchanged at a 23-year high of 5.25–5.50% to put downward pressure on inflation. While inflation is still not back to the Committee’s 2% target, the core PCE deflator has fallen meaningfully from a year-over-year pace of 4.6% when the FOMC last hiked rates a year ago to 2.6% today. The result has been a passive tightening in policy with the real fed funds rate rising over the past year. At the same time, the jobs market has continued to cool and by most measures has returned to its pre-pandemic state. The unemployment rate has risen from its cycle-low, nonfarm payrolls gains over the past three months have been the slowest in more than three years and labor cost growth has cooled noticeably.

The post-meeting statement indicated that the FOMC now sees the risks of a too hot economy or a too cool one as more equally balanced. The statement now reads that the Committee “is attentive to risks to both sides of its dual mandate”, rather than only emphasizing the risks to its inflation mandate as it had in the prior statement. The change of tone comes as the Committee noted softer conditions in the labor market, including job gains having “moderated” and the unemployment rate having “moved up” even if it “remains low.” Meantime, the Committee acknowledged “some further progress” in lowering inflation back to 2%. While the changes marked a step toward eventual easing, they stopped short of fully committing to a rate cut in September to give the Committee flexibility to react to incoming data over the next seven weeks. That said, the implicit signals for looming rate cuts were there: Chair Powell stated in the press conference that “a rate cut could be on the table in September” and “the broad sense of the committee is that the economy is moving closer to the point at which it will be appropriate to reduce our policy rate.”

We suspect today’s decision, post-meeting statement and Powell’s press conference statements reflect a compromise among the Committee members. We believe the more dovishly inclined FOMC participants probably made the case for cutting rates at today’s meeting. As outlined above, inflation is nearly back to the central bank’s target, and the economy has begun to show signs that restrictive monetary policy is taking its toll. Put more simply, if the overwhelming consensus is that a 25 bps cut is appropriate in seven weeks, why wait?

That said, we think the hawks on the Committee likely pressed Powell from the opposite direction. Inflation has been above target for more than three years (and counting), and while the economy appears to have decelerated this year, it has not fallen off a cliff. Given how tough the job has been bringing inflation down, what’s another seven weeks of waiting in exchange for a few more inflation and employment readings? To thread the needle, we think Chair Powell arrived at a compromise: hold rates steady at this meeting, but send overt signals to the market and broader public that the base case is for rate cuts starting soon.

We believe economic conditions have softened sufficiently to drive inflation even closer to 2% in the months ahead, and that risks to the labor market are mounting. While thus far cooling in the labor market is consistent with conditions “normalizing”, the increasingly restrictive stance of policy risks threatening the employment side of the FOMC’s mandate. We look for the Committee to reduce the fed funds rate by 25 bps at its September meeting as a result, with a further 25 bps cut in December and an additional 100 bps of easing in 2025.