{kind=link}

- Fed meeting and Middle East developments in the foreground

- Tuesday’s eurozone GDP figures could produce a surprise

- Wednesday’s inflation report unlikely to unsettle ECB expectations

- Euro remains under pressure against the pound

Fed meeting overshadows key Euro area data

With the market digesting the latest developments in the US presidential race and preparing for Wednesday’s Fed meeting, a rather busy calendar is in store for euro traders this week. The preliminary GDP print for the second quarter of 2024, the eurozone unemployment rate and, more importantly, the preliminary July inflation report could prove market-moving ahead of the expected summer lull.

The latest ECB gathering proved the least exciting one in 2024, but there were some clear messages from President Lagarde. She was adamant about the new “no pre-commitment” dogma and highlighted that the ECB is data dependent and not data-point dependent. This rhetoric was part of her effort to appease the ECB hawks following the rather eventful June meeting, which ended with a rate cut, but created a strong rift within the ECB ranks and substantially raised the bar for the next rate cut.

ECB members have taken a back seat lately as the political situation in the US unfolds and the Summer Olympic Games in Paris are underway. Maybe this is the best time to collect their thoughts and plan the strategy for the rest of 2024 away from the spotlight but paying close attention to the incoming data releases. These figures have been painting a rather bleak picture of the euro area, potentially justifying the ECB doves’ insistence for the June rate cut.

Eurozone Q2 GDP will be released on Tuesday

On Tuesday, the preliminary GDP print for the second quarter of 2024 will be published. Q1 was stronger than expected, dissipating concerns about a protracted recession. Considering the ECB rate cut in June, the fluid political environment in the euro area and the overall negative market sentiment, one would have expected a rather weak set of forecasts on Tuesday.

However, the market is forecasting a small acceleration to the annual eurozone aggressive figure to 0.6% from 0.4% with the quarterly print seen decelerating a tad. Spain and Italy will most likely continue to grow strongly, covering the momentum loss potentially seen in both Germany and France.

Interestingly, with last week’s US GDP figure surprising on the upside and the eurozone PMI services surveys enjoying a strong uptrade during the second quarter of 2024, there is a small possibility for an upside surprise on Tuesday, which would be rather welcomed by the ECB hawks. On the flip side, the European election in early June and the subsequent double parliamentary elections in France might have significantly impacted consumer appetite and business activity in the region.

Preliminary German CPI on Tuesday, eurozone aggregate print on Wednesday

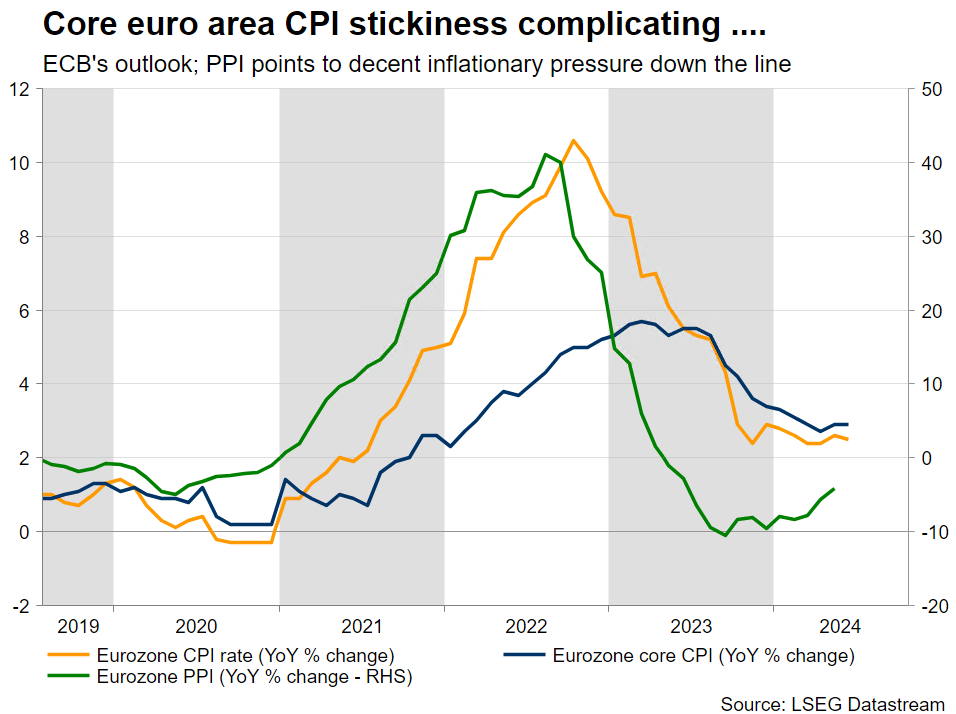

Later on Tuesday, the preliminary CPI prints from the German states will start to trickle in with the German national figure expected around 12.00 GMT. CPI is seen stable at 2.2% year-on-year growth and thus opening the door for a downside surprise at Wednesday’s euro area aggregate release.

At 09.00 GMT on Wednesday morning, the eurozone headline CPI is forecast to show a 2.4% y-o-y increase, down from the June 2.5% print, with the core indicator also edging slightly lower to 2.8%. The next CPI report will be published in late August, with the hopes of a continuation of the recent downward trend cementing market expectations for a September rate cut, regardless of what the Fed opts for.

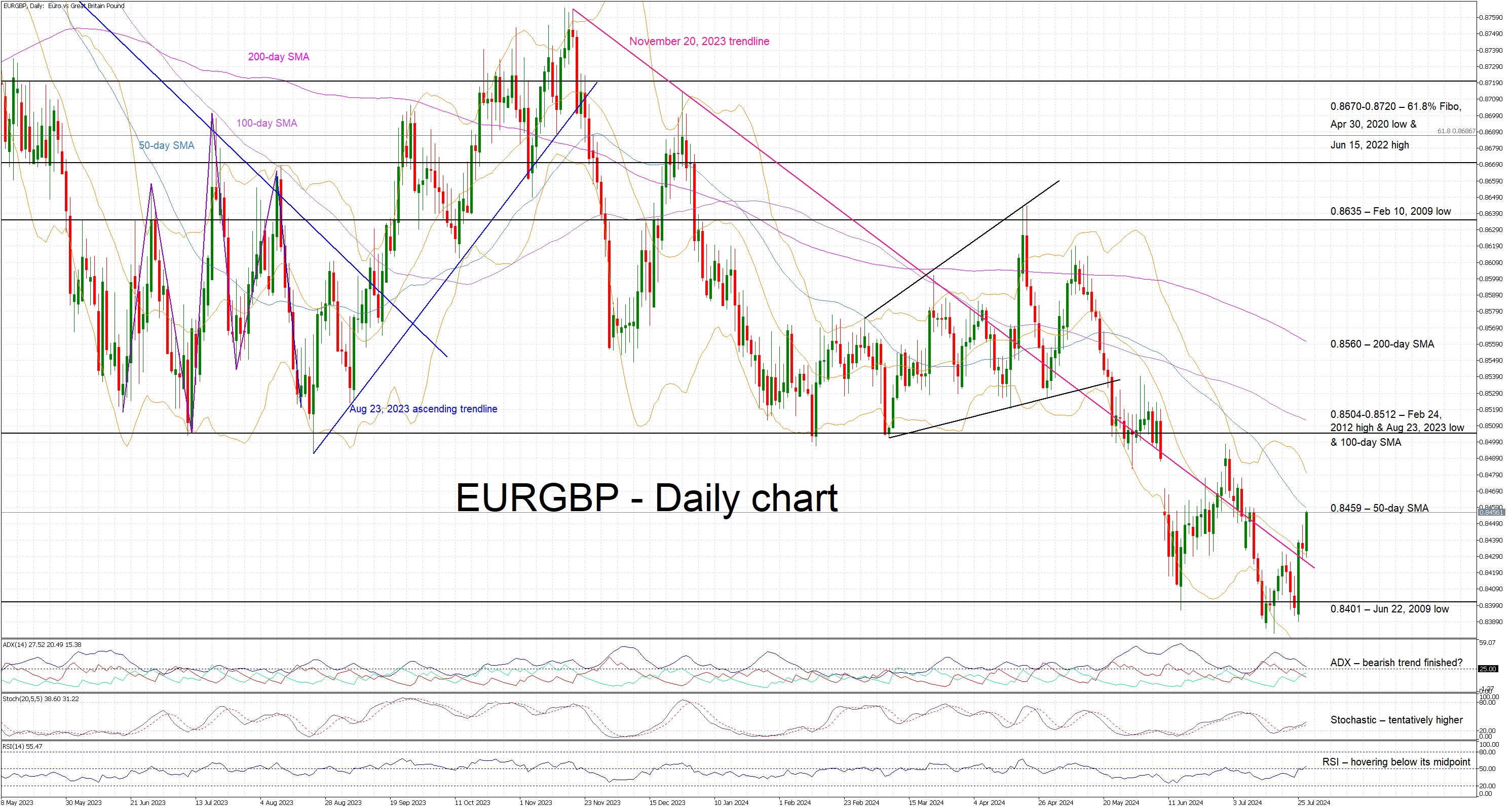

Euro/pound downtrend persists

Despite last week’s recovery, the euro remains under pressure against the pound. The worsening economic outlook for the euro area and the new-found political stability in the UK have been supporting the ongoing pound appreciation.

The BoE could surprise with a rate cut on Thursday, but unless the eurozone data produces consistent upside surprises this week, the bearish trend in euro/pound is unlikely to be reversed soon. Having said that, a confident break above the November 20, 2023 trendline could open the door for a test of the early June peak at 0.8498.