{kind=link}

- Wednesday’s PMI surveys key for both the Fed and the BoE

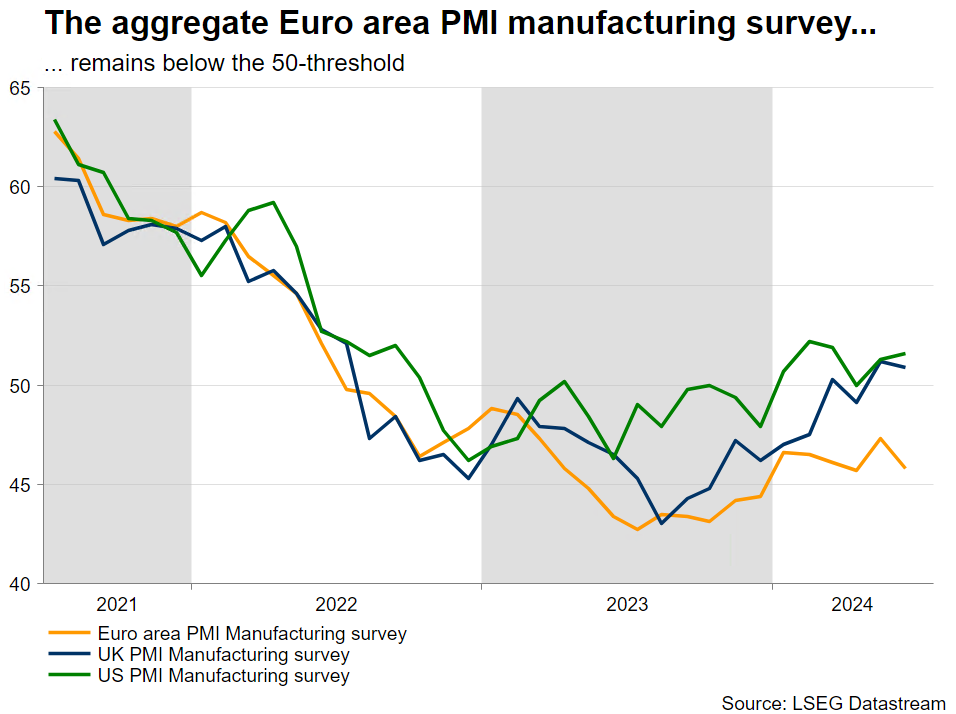

- Eurozone PMI manufacturing survey could disappoint again

- US PMIs unlikely to unsettle September Fed expectations

- UK figures could surprise on the upside after the general election

Important PMI survey prints this week as both the Fed and the BoE meet soon

Despite last week’s stock market correction and the latest developments in the US Presidential race dominating the headlines, economic data releases this week should attract the market’s interest. Both Thursday’s advance US GDP print for the second quarter of 2024 and Friday’s PCE report are expected to have an impact on the market.

On Wednesday, though, the preliminary PMI surveys for July will be published. The importance of these figures cannot be underestimated as the market is trying to predict the likely timing of their next rate moves.

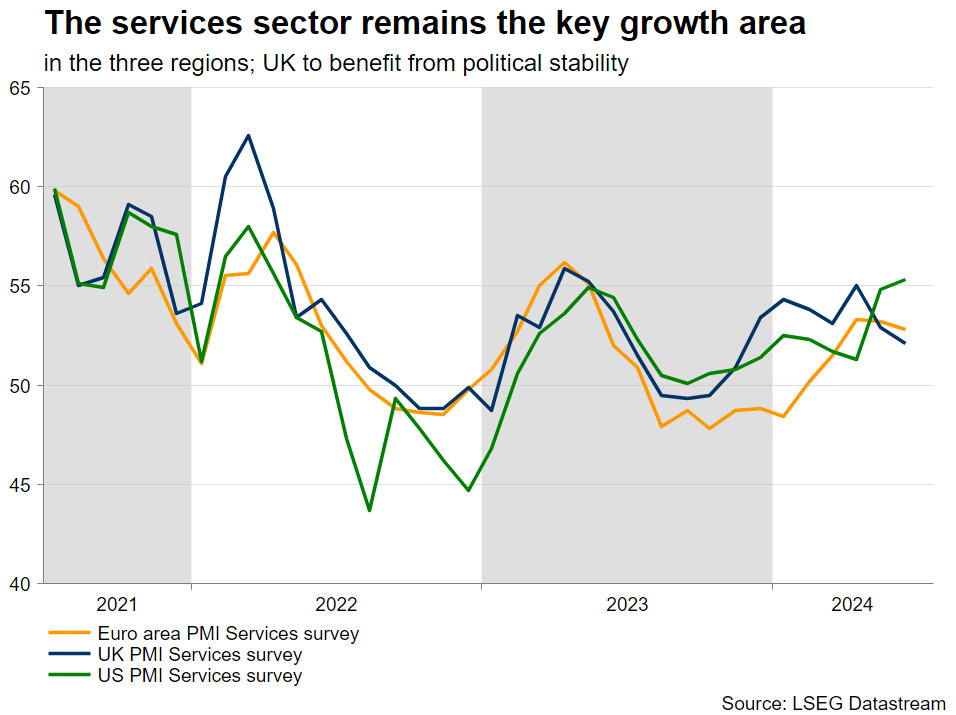

Could the euro area services sector save the day again?

As widely expected, last week’s ECB meeting did not produce any surprises. Rates were kept stable, and President Lagarde appeared moderately balanced with a willingness to advertise the new “no pre-commitment” dogma. The door to a September rate cut remains open, especially if the Fed signals its readiness to start easing its monetary policy stance soon.

President Lagarde mentioned the PMI surveys during last Thursday’s press conference in order to highlight the divergent dynamics seen in the services and manufacturing sectors and their impact on inflation. The services sector pulled the eurozone out of the recession, and its respective PMI survey continues to hover at levels consistent with soft growth.

The same cannot be said for the smaller manufacturing sector, which has remained stuck below the 50-level for the past two years. The main culprit of this abysmal performance is Germany where the once-mighty manufacturing segment has lost part of its competitiveness edge against other powerhouses due to the lack of cheap Russian energy. Similarly, the French manufacturing sector continues to underperform, which is somewhat expected considering the recent political unrest.

Focusing on Wednesday’s prints, the market expects a small improvement across the board. The eurozone aggregate services indicator should edge higher to 53, while the manufacturing survey is expected to climb to 46.1.

US PMI surveys to give useful information to the Fed

While the Fed’s preferred set of indicators remains the Institute for Supply Management (ISM) indices, going into the July 31 gathering, Fed members will probably have access only to the already-published PMI surveys. And these PMIs accurately depict the economic advantage of the US against the eurozone as the composite PMI survey indicator jumped in June to the highest level since May 2022.

Like the euro area, the services sector is the key growth area of the US economy with the respective PMI services survey climbing to a 2-year high. However, contrary to the eurozone, the PMI survey for the manufacturing sector has recently climbed above the 50-threshold, and it appears to be on a gentle upward trend.

The market is currently forecasting a small pickup in the PMI manufacturing survey but a decent correction in the services one. Confirmation of these figures is unlikely to change the Fed outlook, with the market fully pricing in a 25bps rate cut in September. Actually, weaker data prints could allow the Fed to start cutting rates with a clear conscience, despite the currently elevated inflation rates. The July 31 meeting might prove uneventful, but the Jackson Hole symposium at the end of August could prove pivotal in the current cycle.

The UK could benefit from political stability

A different picture emerges in the UK where the PMI services survey remains above the 50-threshold, but it has failed to achieve the progress seen in other regions. The recent general election has probably improved sentiment in this sector and hence it will be interesting to see if the recent weakness reversed on Wednesday.

Interestingly, the manufacturing sector has been recovering aggressively from the 2023 trough and has actually returned above the 50 mark in the past two months. This is quite noteworthy considering the very weak prints seen in the eurozone, but the strong UK domestic demand could possibly explain the manufacturing sector’s solid performance.

The market expects a positive set of figures with the services survey climbing to 52.5 and the manufacturing one edging to 51.1. The BoE meets on August 1, the day after the Fed gathering, with the market recently scaling back its expectations for an August rate cut. A strong downside surprise from Wednesday’s PMIs could tempt the BoE doves to put a rate cut on the table at the next gathering.