{kind=link}

U.S. Highlights

- After an eerily calm few months, a fresh dose of volatility descended across global financial markets this week.

- Top Fed officials speaking this week noted that they are getting ‘closer’ to cutting interest rates. Financial markets have fully priced the first cut to come in September.

- Retail sales and industrial production data for June came in better than expected, while homebuilding remains under pressure.

Canadian Highlights

- Economic data was under the microscope this week, ahead of the Bank of Canada’s interest rate decision on July 24th. An interest rate cut is universally expected, with both business sentiment and retail sales pointing to weak demand in Canada’s economy, which should help ease inflation pressures going forward.

- However, if Governor Macklem opts to surprise markets with a hold, he will likely cite a lack of progress on core inflation metrics in recent months, driven by services inflation moving in the wrong direction recently.

U.S. – Nearing the Pivot Point

After an eerily calm few months, this week brought a fresh dose of volatility across global financial markets. The equity selloff was heavily concentrated across the tech sector, following some speculation that the Biden administration is considering implementing new rules to clamp down on companies exporting chipmaking equipment to China. While the selloff widened as the week progressed, small-cap stocks still managed to end the week 2% higher and are up 8% over the past nine trading days. The S&P 500 is down nearly 0.5% over that same period. The recent outperformance has largely been driven by market participants becoming increasingly confident that the Fed will begin easing its policy stance over the coming months. At the time of writing, market odds are fully priced for the first cut to come in September, with 63 bps of easing expected by year-end.

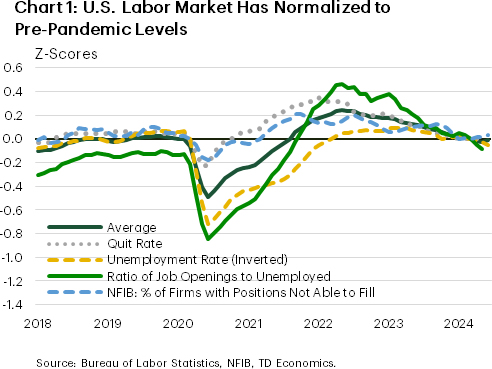

Based on how recent data has trended, investors have good reason to suspect that the Fed will likely begin dialing back its policy rate come September. Last week’s CPI report showed inflationary pressures cooling faster than expected, while recent readings of the labor market suggest that nearly all the pandemic imbalances have been restored (Chart 1). Speaking at an event at the Washington Economic Club this week, Powell reiterated the point on the labor market, citing “… essentially we’re back at equilibrium”. On inflation, Powell noted that recent readings have “added somewhat to confidence”. Other Fed officials including Williams and Waller echoed Powell’s sentiment this week, noting that the improved inflation trajectory has brought the Fed “closer” to cutting interest rates and that the current economic data are consistent with the Fed achieving a ‘soft landing’.

Indeed, economic data out this week support the notion that while the economy is slowing, it’s not falling off a cliff. Retail sales were flat in June, but that was largely related to a sharp pullback in auto sales due to a cyber attack on a software firm that supports car dealers across the country. Meanwhile, the control retail group – used in the BEA’s calculation of PCE – rose by a healthy 0.9% m/m, while revisions to prior months showed a stronger pace of consumer spending in April/May. Consumer spending is tracking around 2% annualized for Q2, a touch higher than Q1’s 1.5% but handily below the +3% pace averaged through the second half of last year.

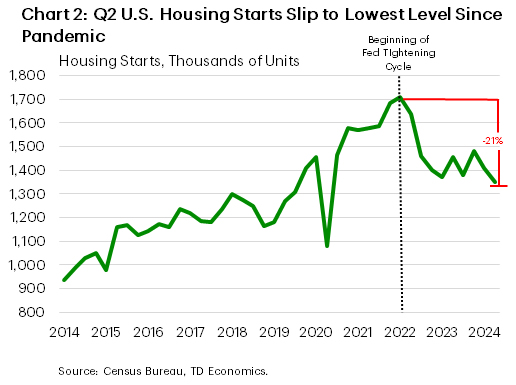

Meanwhile, industrial production data for June rose by a respectable 0.6% m/m and recorded its largest quarterly gain since Q2-2021. Encouragingly, the manufacturing index has now posted gains in four of the last five months and is closing in on levels not seen since the Federal Reserve first started hiking interest rates back in March 2022. Conversely, home building activity continues to feel the pinch of higher rates, with Q2 housing starts slipping to a new post-Fed tightening low (Chart 2).

All told, it’s becoming increasingly clear the U.S. economy is downshifting from last year’s breakneck rate of expansion to something closer to a trend-like pace. Provided the next two inflation readings don’t show any meaningful reversal in recent trends, the Fed likely has a clear path to start cutting rates in the coming months.

Canada – Will the BoC Focus on the Fly or the Ointment?

This week’s economic data was under the microscope coming ahead of the Bank of Canada (BoC) interest rate announcement and updated Monetary Policy Report on July 24th. Canada’s inflation data garnered the highest scrutiny, and it came in lower than consensus expectations with a 2.7% reading – the slowest pace in more than three years. This reading cemented market bets for a quarter-point interest rate cut next week. We agree that is the most likely outcome, however, a renewed uptick in services inflation could spook the BoC into holding rates steady.

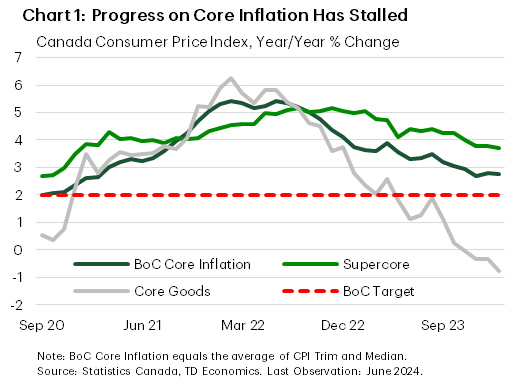

Scratching beneath the surface on CPI inflation, there is one fly in the ointment. The BoC’s preferred core inflation measure didn’t make any progress in June, stuck at 2.8% year-on-year (y/y) on average (Chart 1). Narrowing in on the most recent three months, core inflation pressures picked up from 2.5% in May to 2.9% in June. If the Bank of Canada opts to surprise markets next week and take a pause on rate cuts, this will likely be the reason that they cite.

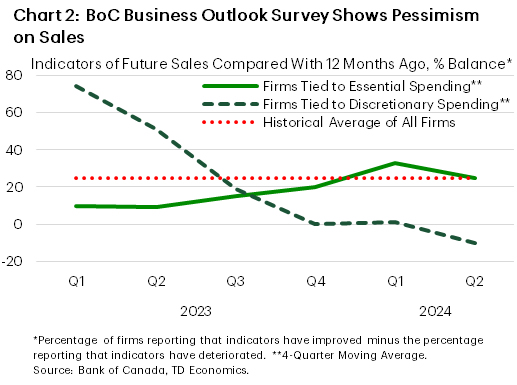

It will come down to how much weight the Bank of Canada puts on this particular fly. Other activity and sentiment indicators are sending very clear signals that the Canadian economy is bending under the weight of higher rates. The BoC’s Business Outlook Survey for the second quarter was one such sign. The survey described business sentiment as low, and the main factors businesses mentioned were weighing on sentiment were: elevated interest rates, weak demand for non-essential goods and services, and ongoing high costs. Businesses expectations for future sales also remained historically low, and those tied to discretionary consumer spending are particularly weak (Chart 2). Businesses also expect growth in their selling prices to continue easing, which is good news for future progress on the Bank’s inflation target.

May retail sales were another sign that the consumer is also weakening. Sales were down more than expected on the month, with eight of nine industry categories and nine of ten provinces seeing sales fall. Sales were also down 0.7% month/month (m/m) in real terms. The one area to gain ground was motor vehicle and parts dealers (+0.8% m/m), led by an increase at new car dealers. Apart from that, there were no other silver linings in May retail sales. Even the advance retail indicator is pointing to another decline in sales for June.

Now it is over to the BoC’s announcement, which will also update the bank’s economic forecast. Since the last update in April, inflation has fallen slightly faster than the Bank had expected, and growth has been weaker. What we don’t know is how many rate cuts the Bank had assumed within that view. But whatever it was, there is a strong argument for a bit more easing now. The fact that the U.S. Federal Reserve is also looking like they could cut a bit earlier than was thought a few months ago helps the case for a BoC cut. That reduces any BoC worries about spreads widening too much and weakening the Canadian dollar, which would complicate their job reining in inflation.