will ease monetary policy again in the coming months and over the course of 2025. Lower interest rates have been a source of renminbi depreciation; however, policymakers have mounted an effective defense of the currency as appetite for a weaker currency seems limited. Longer-term, we remain optimistic on the prospects for the renminbi despite underwhelming initial takeaways from China's Third Plenum.){kind=link}

And The Third Plenum Suggests No Major Economic Model Adjustments

Summary

Recent GDP and activity data from China were underwhelming, and as a result, we have revised our 2024 annual GDP growth forecast lower. With activity sluggish and price pressures still subdued we reiterate our view that the People’s Bank of China (PBoC) will ease monetary policy again in the coming months and over the course of 2025. Lower interest rates have been a source of renminbi depreciation; however, policymakers have mounted an effective defense of the currency as appetite for a weaker currency seems limited. Longer-term, we remain optimistic on the prospects for the renminbi despite underwhelming initial takeaways from China’s Third Plenum.

Revising Down Our China GDP Growth Forecast

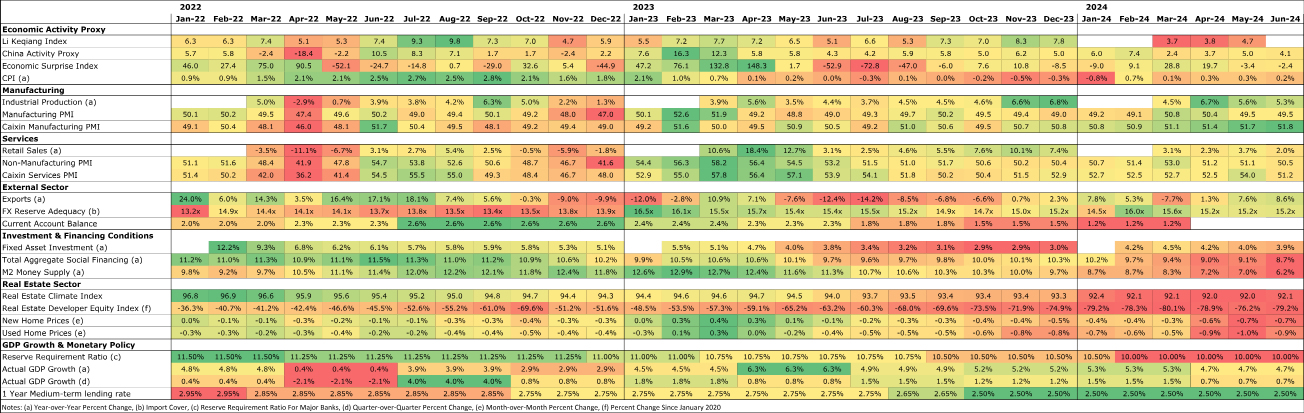

Following relatively steady activity over the course of the first few months of this year, China’s economy has since demonstrated a renewed downturn. Most sentiment and activity indicators have tailed-off during the last few months, ultimately culminating in a recent GDP print that was nothing short of underwhelming. In Q2-2024, China’s economy grew 4.7% year-on-year—well below our forecast as well as consensus expectations—and a notable slowdown relative to Q1. At first glance, weak domestic consumption seems to be the primary driver of China’s softening economic momentum. Retail sales were especially weak in June, but missed expectations for most of the second quarter. Persistent subdued inflation/disinflation pressures, a real estate sector that remains in correction, as well as household preferences to save, all contribute to a local backdrop that is not conducive to spending. China’s recent economic slowdown may be driven by soft consumption, although pockets of weakness exist outside of consumption (Figure 1). China’s manufacturing sector remains in contraction territory, while capital formation and conditions for inbound investment also appear to be sluggish and restraining overall economic growth. Exports have been supported recently; however, we continue to believe China is gradually becoming a less integral part of the global supply chain. Over time, China being replaced as the manufacturer to the world can challenge China’s export-led economic model over the medium-to-longer term. Incorporating recent GDP data into our forecast profile for China’s economy leads us to downwardly revise our 2024 annual growth forecast. To that point, we now forecast China’s economy to grow 4.8% this year, down from 5.1% before the latest data releases. Given the sheer size and importance of China to the global economy, all else equal, this downward revision will also have negative implications for our global GDP forecast.

PBoC Unrelenting on Monetary Easing & FX Defense

With Chinese growth shifting back to an uninspiring direction, we continue to believe the People’s Bank of China (PBoC) will regularly ease monetary policy over the course of our forecast horizon. In that sense, we maintain our view that PBoC policymakers will lower the “major bank” Reserve Requirement Ratio (RRR) again in Q3-2024. As of now, the RRR for major domestic banks is 10.00%. In our view, the combination of sluggish economic growth and subdued price pressures offers enough rationale for Chinese authorities to deliver another 50 bps reduction in the RRR in the coming months. Longer-term, we believe China’s growth and inflation dynamics will remain subdued. Under that assumption, we believe additional RRR cuts are likely to be delivered over the course of next year as well. To that point, given our less-than-robust outlook for Chinese activity and price growth, we reiterate our forecast for 100 bps of RRR cuts over the course of 2025, taking the major banks RRR to 8.50% by the end of next year. Worth noting, is that we believe PBoC policymakers will seek to ease monetary policy irrespective of other policy decisions from major central banks. While we believe institutions such as the Federal Reserve will lower interest rates this year and in 2025, the “higher for longer” theme has not completely dissipated. Many emerging markets central banks, at least historically, have taken monetary policy cues from the Fed and adjusted policy rates taking into account FOMC decisions. However, regardless of whether the Fed keeps interest rates unchanged for an extended period of time or delivers cuts along the contours of our forecast, we believe PBoC policymakers will operate with a degree of autonomy and primarily respond to the evolution of domestic activity and price pressures, rather than the direction of interest rates in the United States.

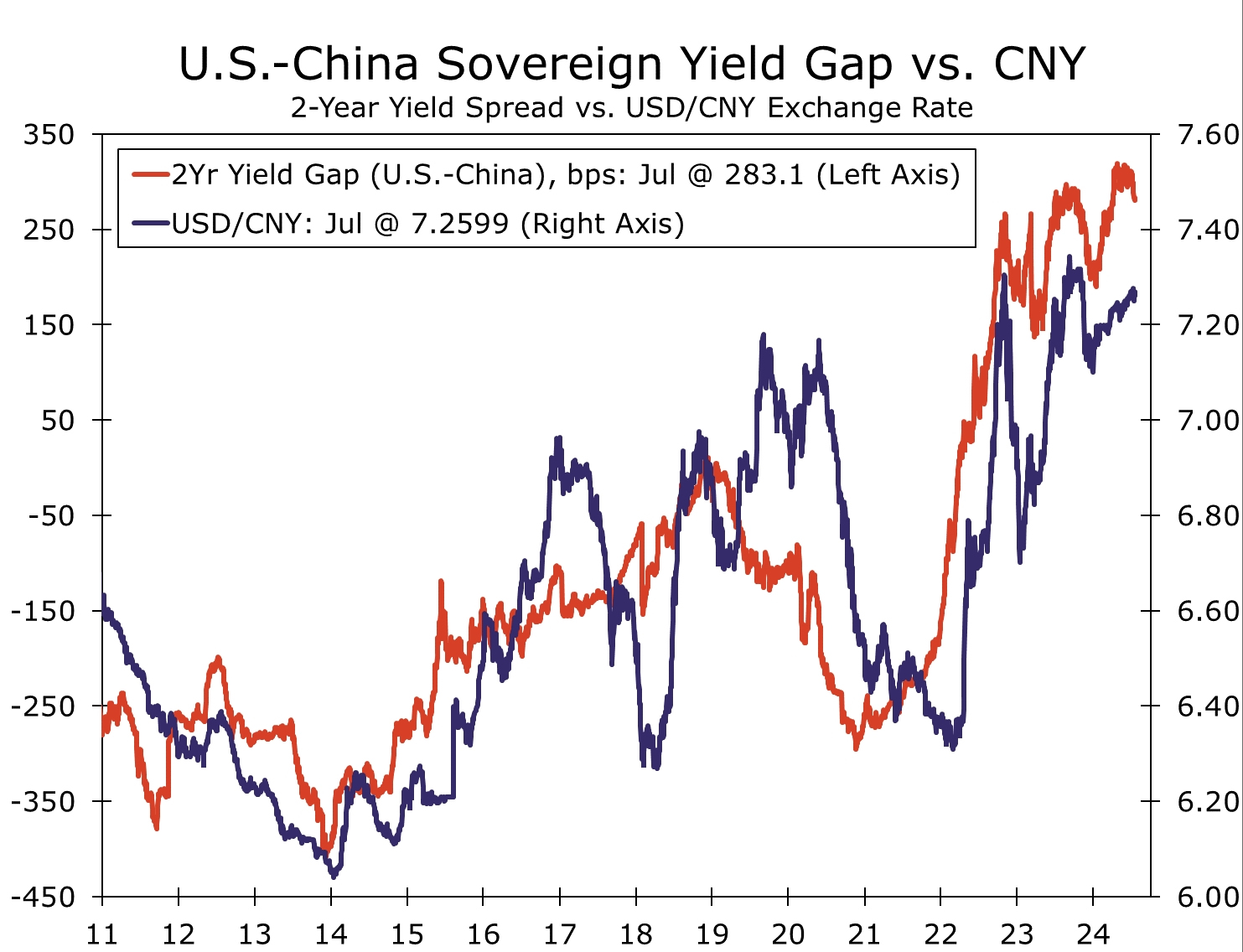

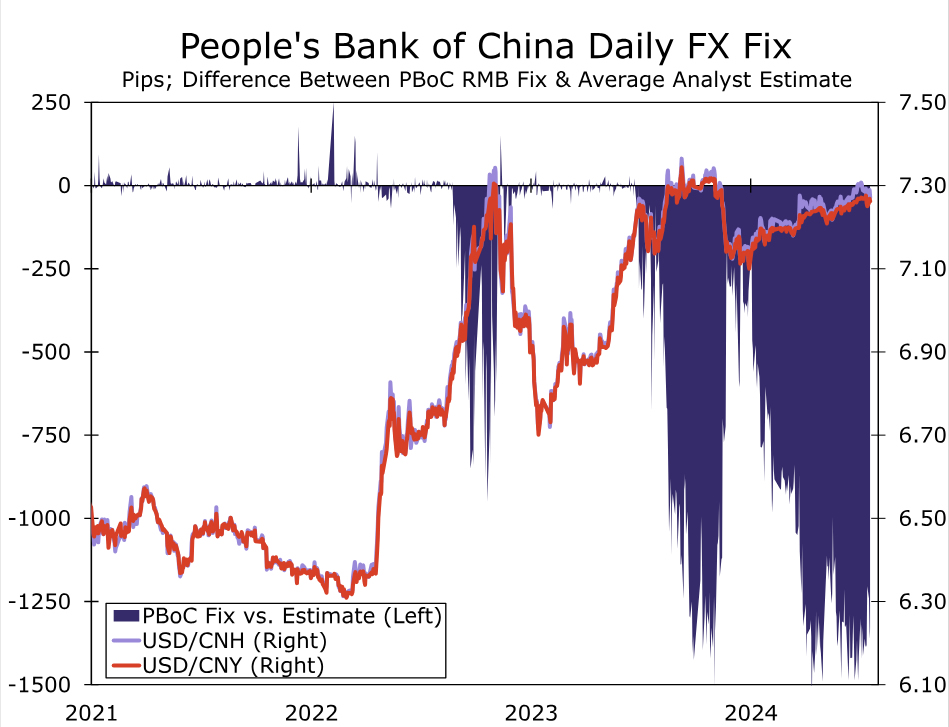

In fairness, PBoC policymakers have determined monetary policy settings notwithstanding the Fed for years. As the Fed pursued tighter monetary policy to contain inflation in early 2022, PBoC policymakers were lowering interest rates in an effort to support economic activity and generate inflation. Diverging paths for Fed-PBoC monetary policy have been the primary source of a weaker Chinese currency over the last few years. Widening interest rate differentials between the Fed and PBoC drove the USD/CNY exchange rate to a peak of ~CNY7.35, from ~CNY6.30 when the Fed started its latest rate hike cycle (Figure 2). While interest rate differentials suggest the renminbi could be even weaker, PBoC policymakers have utilized their FX toolkit effectively to mount an impressive defense of the Chinese currency. Central bankers continue to use the overnight renminbi fix as primary means to defend the value of the renminbi, opting to set a stronger fix relative to market expectations, a signal we interpret as policymakers having limited appetite for a weaker yuan at the current juncture (Figure 3). In our view, policymakers will continue to use FX policy tools at their disposal to limit renminbi volatility and further protect against any significant currency depreciation for the time being. We believe the overnight fix will continue to act as the first line of defense, although authorities have also turned to verbal intervention as a way to deter FX speculators from allocating capital toward a weaker renminbi. Verbal intervention along with the daily fix should be enough to keep the renminbi steady for the time being, and while more of a tertiary option, the PBoC also has a war chest of FX reserves it could draw on to prevent FX weakness if need be.

Longer-term, we are more constructive on the Chinese currency. While we are not necessarily optimistic on the outlook for China’s economy, we do believe the same interest rate differentials that have weighed on the renminbi could act as a source of longer-term strength for the currency. As mentioned, we believe the Federal Reserve will deliver rate cuts starting in September and continue easing through the end of 2025. Even as the PBoC delivers easier monetary policy, Fed rate cuts can at least keep current interest rate differentials steady rather than widening. In fact, our core view for the long-term path of the U.S. dollar is that Fed rate cuts apply depreciation pressures broadly to the U.S. dollar. Even more, we believe accommodative Fed policy could drive easier global financial conditions, which can reduce demand for safe haven currencies such as the U.S. dollar and boost foreign currencies, including the renminbi. Dollar depreciation, in our view, can push the renminbi back below CNH7.20 by the end of 2025. We do, however, acknowledge that risks to our long-term, as well as shorter-term, renminbi forecasts are tilted toward less Chinese currency strength. Those risks stem from the U.S. election and the rising possibility of the implementation of a more adverse policy mix toward China. Regardless of the outcome of the election, trade policy toward China could turn more hostile; however, in a second Trump administration, trade policy could turn severely more antagonistic. Former President Trump has floated the possibility of a 60%, or even 100%, tariff on all Chinese exports to the United States. Not only would tariffs apply another source of pressure on China’s economy, but would likely also damage sentiment toward local Chinese financial markets and the renminbi. Should tariffs indeed be raised and China’s economy indeed be damaged through reduced exports and weak sentiment, PBoC policymakers could accommodate renminbi depreciation to offset economic pressures. For the time being, this scenario represents a downside risk. We are not incorporating any U.S.-political induced renminbi depreciation into our base case FX forecasts, nor our outlook for the Chinese economy.

As Expected, The Third Plenum Underwhelms

Also of note and worth highlighting is that China hosted its every-five-year Third Plenum this week. At select times in the past, Chinese authorities have used the Third Plenum to alter the strategic direction of China’s economy, specifically attempting to integrate China more into the global economy and opening up to Western nations. However, while Third Plenum meetings capture market attention and have been used as an agent for change in the past, Third Plenums more often fail to live up to expectations or serve as a platform for major change to the longer-term vision of China’s economy. In our view, the 2024 Third Plenum, up to this point, seemingly follows this trend. While more robust details are likely still forthcoming, we interpret the initial communique as the Third Plenum failing to deliver anything especially meaningful that would suggest changes to the longer-term direction for the Chinese economy. The communique refers to China’s, and President Xi’s, ambition for “high quality growth” rather than the overall growth rate of China’s economy. As far as “high quality growth”, Chinese authorities seem to still be focused on manufacturing capabilities and production in high-tech sectors. We view the focus on manufacturing—as opposed to an attempt to reposition China as a domestic demand driven economy—as also rather underwhelming. As mentioned, China’s geopolitical ambitions are already resulting in fewer export destinations for locally produced goods. Maintaining an export driven economic model, in our view, is likely to keep downward pressure on China’s growth rate and also possibly even act as a roadblock to achieving “high quality” growth.

While the Third Plenum is not typically a forum for fiscal stimulus discussions nor decisions, the dire state of China’s property sector was not forcefully addressed in the first communique. Since the Global Financial Crisis in 2008-2009, China has often relied on infrastructure spending and property development to fuel economic growth. In recent years, the property sector has been in significant decline and has raised the likelihood of a China “hard landing” financial crisis scenario unfolding. Perhaps a more strategic plan or fiscal stimulus for China’s property sector will be announced in the coming days, but with China’s fiscal deficit and debt burden in troubling shape, as well as a desire for export-driven growth, we have our doubts a meaningful policy response will be delivered to address China’s real estate sector issues. The initial statement touched on, but offered little detail, into China’s geopolitical ambitions, specifically related to Taiwan. Third Plenum meetings are designed to outline the medium-term economic plan, but with focus on geopolitics ramping up over the years, foreign relations could grab a bit more focus relative to prior meetings. When, or if, more details on discussions are released, we will be paying attention to any references to geopolitics, military capabilities and/or Taiwan. We have noted in prior publications that 2024-2027 is a timeframe where geopolitical event risks are elevated. A more hostile approach to Taiwan or reunification attempt is unlikely by 2027, but perhaps details from recent economic discussions can offer insight into Xi’s and the broader CCP’s geopolitical thinking.