{kind=link}

- Market prices in at least two rate cuts from Fed

- ECB, BoE expected to follow suit despite divergent economic conditions

- SNB and BoC could ease further; RBNZ possibly close to a summer rate cut

- BoJ and RBA could surprise with rate hikes during 2024

We are halfway into 2024 and the countdown for this year’s key event, the US presidential election, has already started. With geopolitics taking a backseat lately, despite both the Ukrainian-Russian and Israeli-Hamas conflicts remaining unresolved, political risk is expected to affect market sentiment, as seen lately in the euro area.

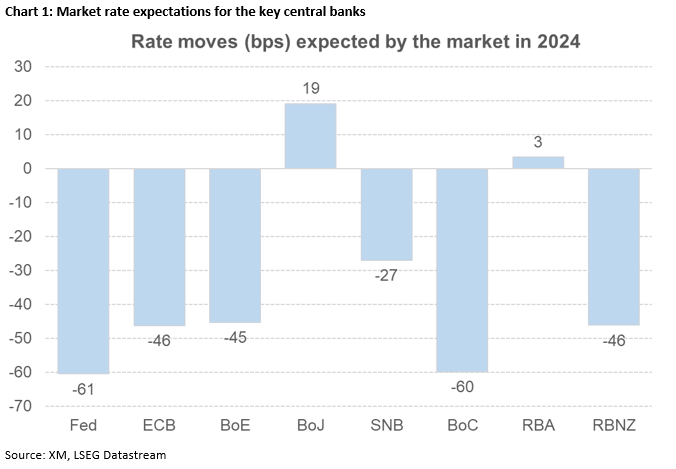

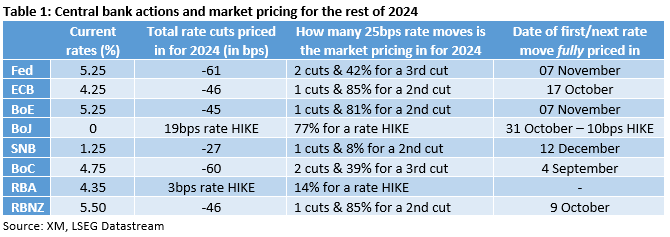

Amidst these developments, the key central banks are trying to implement their strategy. The ECB, the Swiss National Bank and the Bank of Canada have already started to ease their monetary policy stance while the Bank of Japan has managed to hike once so far in 2024. The remaining central banks, and predominantly the Fed, remain on the sidelines. Ahead of the next round of central bank meetings, what is the market pricing in for the rest of 2024?

The Fed to follow in the ECB’s footsteps?

The recent US labour market data and the June CPI report have probably firmly opened the door to the much-discussed rate cuts by the Fed. The market is currently pricing in 61bps of rate easing in 2024, which translates to two 25bps rate cuts and a 41% chance for a third similarly sized move. Considering the November presidential election and the June 2024 dot plot penciling in one rate cut, the market might be getting too optimistic, especially if the data improves over the summer.

Turning to the ECB, when a central bank announces its first rate cut, the path is assumed to be fixed towards further accommodation. As made evident by recent ECB members’ comments, this is not the case now. Having said that, the market is currently expecting 46bps of easing in 2024, which means one full 25bps rate move and around 90% possibility of a second rate cut. Interestingly, political developments in France could tip the balance in favour of more rate cuts down the line.

The market expects both the BoE and the RBZN to start cutting soon

The market expects almost two rate cuts by both the Bank of the England and the Reserve Bank of New Zealand in 2024. The recent aggressive drop in UK headline inflation could have opened the door to a rate cut by the BoE, but the political developments forced it to go into a brief hibernation. With the general election out of the picture, another weak CPI report on July 17 could materially increase the chance of a rate cut at the August 1 meeting, which includes the quarterly monetary policy report.

Similarly, the RBNZ’S dovish shift at its most recent meeting surprised the market since just 40 days ago the RBNZ was considering the rate hike option. The market has quickly adapted to the new status quo by pricing in a total easing of 46bps by year-end, with a considerable probability of a summer rate cut if the imminent quarterly CPI surprises on the downside.

BoC and SNB cut rates, market expects more

Responding to easing inflation, both the BoC and the SNB eased their monetary policy stance over the past few months. In the case of the former, the Canadian economy has not been firing into all cylinders with unemployment rising to the highest level since February 2022. Ignoring the recent upside surprise in monthly inflation, the market continues to fully price in two rate cuts in 2024, with a sizeable possibility of a third one towards the end of the year.

Turning to the SNB and the two rate cuts already announced were partly unexpected but probably justified due to the low inflation rate and the continued strengthening of the franc. The SNB stands ready to ease further, with the market currently fully pricing in another 25bps rate cut at the December meeting.

BoJ to hike again, RBA thinking about it

The BoJ remains on the lonely path of tightening its monetary policy stance. The April rate hike was welcomed by the market, but BoJ’s recent inactivity has raised a few eyebrows, weakening the yen. Japanese authorities could be hoping that a sustained worsening of US data and the mild hawkishness of the BoJ could help the yen recover. The market is looking for 19bps of rate hikes by the BoJ in 2024 with the next 10bps rate hike expected at the September meeting. Firstly though, the market awaits the full details of the bond buying programme tapering.

The Reserve Bank of Australia is the only other central bank thinking about rate hikes. Stickier inflation and a tight labour market are keeping Governor Bullock et al on their toes with the minutes from the June meeting confirming the RBA’s intention to hike rates if needed. The market is tentatively pricing in 3bps of tightening in 2024 but RBA’s rates outlook will probably be gravely affected by the July 31 CPI print for the second quarter of 2024.