{kind=link}

- Surprisingly, the RBNZ’s July OCR Review was markedly less hawkish than the May Statement.

- The RBNZ’s growth forecasts seem to have been significantly downgraded from their May view.

- The RBNZ crucially seems more confident that annual inflation will be below 3% quite soon, giving them more latitude to reduce policy restriction.

- The recent QSBO survey likely crystalised the downside risks to the growth and inflation outlooks that were evident in other high frequency indicators.

- The RBNZ’s abrupt change in messaging at the July Review suggests a non-trivial risk of policy easing before long.

- Our central expectation remains that the RBNZ will begin easing policy in February next year. But an earlier move is very feasible and will be data dependent.

- We set out here what we think the RBNZ would likely need to see in the upcoming data to begin easing sooner than February.

What caused the marked change in the RBNZ’s tone in the July OCR Review?

Like most commentators and financial market participants, we were very surprised by the marked change in tone in this week’s July OCR Review. The economy has looked to be steadily weakening relative to the RBNZ’s May Statement view. Hence, we expected the RBNZ would soon begin to moderate the very hawkish tone conveyed in the May Statement. But we didn’t expect as large a shift so soon given in May the RBNZ seemed particularly hawkish and had pushed out the timing of the first policy easing until August 2025. We thought it more likely the RBNZ’s view would begin to evolve in the August Statement and converge towards our own longstanding view that easing could begin early in 2025.

But the July OCR Review message was much less hawkish than that. We discussed the main features of the July OCR Review in our review. In summary, the commentary in the press statement and record of meeting pointed to a more optimistic outlook for inflation this year and a less optimistic outlook for activity, with the latter now said to be “declining” based on high-frequency indicators. And most jarring of all was the final paragraph of the press statement: “The Committee agreed that monetary policy will need to remain restrictive. The extent of this restraint will be tempered over time consistent with the expected decline in inflation pressures” (our emphasis in italics). This latter discussing of future policy easing was not expected at this review and was surprising as the RBNZ likely understood markets would amplify the point and push even harder for a much earlier move in the OCR.

So, what has led to such an abrupt change in the RBNZ’s tone? We think that the RBNZ has been sufficiently shaken by the flow of data and business commentary since the May meeting to move totally away from their previous tightening bias.

The path for activity has been reassessed.

We suspect the latest QSBO business survey was key as it echoed earlier indications from the ANZ Business Outlook survey and from the BusinessNZ PMIs. Collectively these surveys suggest that GDP likely contracted in the June quarter, in contrast with the RBNZ’s forecast of modest growth, with little indication of a pick-up in the second half of the year.

The QSBO also pointed to a further easing of pressures in the labour market and associated indicators of productive capacity. This confirmed the reading from our own Employment Confidence Survey and an emerging downtrend in filled jobs, as measured by the Monthly Employment Indicator and the even more timely weekly filled jobs data (taken from tax data).

Inflation looks more likely to be below 3% in 2024.

Importantly, the QSBO also confirmed the significant step lower in firms’ pricing intentions that had been reported in the May and June editions of the ANZ Business Outlook survey. These now suggest inflation will soon return to the inflation target range. This data, combined with the latest monthly CPI indicators, has likely been the key driver of the RBNZ’s increased confidence that headline inflation will return to within the target range “in the second half of this year” (in May the RBNZ forecast inflation below 3% “by the end of 2024”).

The return of inflation to the 1-3% target range would be an important milestone for the RBNZ. The RBNZ’s relatively hawkish stance since late 2023 has been entirely driven by concerns that inflation would take too long to adjust lower. It seems that the RBNZ’s optimism has significantly increased which is giving them room to shift strategy towards considering easing.

Why did the RBNZ make this change in July, and not wait until August?

The abrupt shift in tone at the July Review raises significant questions about the RBNZ’s current view of the OCR profile and the likely timing of the first policy easing. It’s almost certain that the RBNZ’s OCR profile is much flatter and shows earlier easing than before. The key question is how large their adjustment is relative to the 60% chance of a further 25 bp hike in interest rates and an initial easing at the August 2025 Statement that was previously forecast.

We suspect their adjustment is relatively large as otherwise we doubt that the RBNZ would have felt the need to make such a significant change to its policy stance this week, especially with important inflation and labour market data looming.

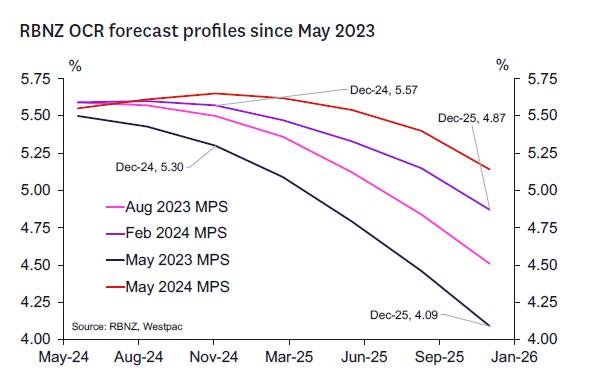

Referring to the RBNZ’s past forecasts of the OCR through 2024 and 2025 could help provide a benchmark for how large the reassessment might be. With the May Statement view being stale, some potential options to consider are the RBNZ’s forecasts back in February 2024 (when they expressed a relatively dovish view compared to market expectations) and May 2023 (when the RBNZ thought the tightening cycle was over and the next move in the OCR would likely be lower). The chart below summarizes the RBNZ’s past OCR forecasts.

These benchmarks might provide a range within the RBNZ could be sitting now while awaiting the key CPI and labour market data ahead. A move back to their February view (removing the May hawkish sojourn) would imply easing around February 2025 (Westpac’s current forecast). Total easing through 2025 would add up to around 50- 75 points.

A move back to May 2023 could provide a relatively dovish alternative. The overall inflation forecasts are not much different (perhaps a tad higher) than what we face today (although the markedly higher non-tradables profile would suggest caution in extrapolating the expected fall in inflation too far ahead). That scenario showed a chance of an easing in October 2024 and a likely easing in November 2024.

The decision to change course in the July Review likely means that the RBNZ now sees some possibility that incoming data could make a compelling case for policy easing before the end of this year. That would be consistent with the RBNZ lying somewhere within the range of where it has been in May 2023 and February 2024.

The RBNZ is almost certainly giving some weight to the possibility that near-term growth outlook could be considerably weaker than forecast in May, with significant downside consequences for the medium-term inflation outlook. Hence the RBNZ probably felt it needed to begin moving away from its very hawkish May view sooner rather than later. This would allow for a less jarring change of tone in the August or October policy reviews should downside risks continue to build.

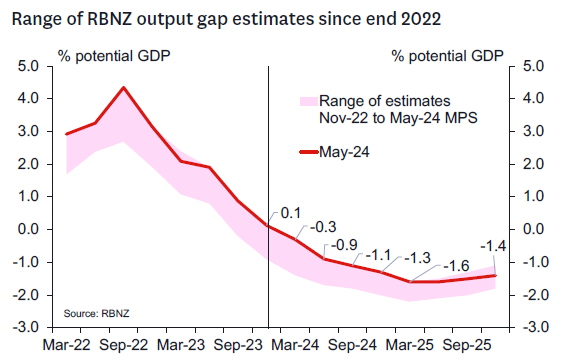

Its likely the RBNZ’s forward estimates of the output gap will be revised lower from the relatively high-water mark reached in May. The May 2023 output gap profile marked the low tide mark in the chart below and could be consistent with a mark down in GDP of 0.5-1.0% range through the balance of 2024 (and perhaps a 0.25-0.5% increase in forecasts of the unemployment rate).

But we doubt that the changes in the risks in the activity outlook alone would have justified such a dovish tilt. The RBNZ’s growth forecasts had already been marked down a lot in May and were not especially optimistic. Rather it’s the additional confidence they seem to have on the inflation outlook – and particularly the near-term inflation profile – that seems particularly prominent. The weaker growth expectations help increase confidence that medium term inflation will move towards 2% – which likely remains a core goal of the RBNZ. But its that confidence that inflation will nudge below 3% relatively soon that will be giving them the confidence to move earlier. And it probably explains why the RBNZ’s language focuses on “tempering” restriction as opposed to pumping the accelerator to boost growth. This latter point is likely important in understanding the pace and extent of the easing profile once started.

What scenarios could see the RBNZ tempering restriction in the next 6 months?

Here we discuss some more specific data hurdles we think need to be crossed to begin reducing restriction, recognizing that there are also other key indicators (both domestic and abroad) that will impinge on the assessment of the domestic policy outlook:

- For easing to begin in August, we would likely need to have seen the following:

- A significant broad-based downside surprise in the Q2 CPI on 17 July (WBC forecast 0.6% qoq/3.5% yoy). The surprise would need to be sufficient to give confidence that future quarterly CPI outcomes will soon sit close to historic norms. This implies a need to see significant downside surprise in the non-tradables component of the CPI (WBC forecast 0.8% qoq/5.3% yoy) that is itself broad-based and consistent with excess capacity flowing through to lower core inflation pressures; and

- A significant upside surprise (perhaps close to 5%) in the unemployment rate in the Q2 labour market data on 7 August (WBC forecast 4.6%), and clear signs that wage inflation is dissipating more quickly than expected (WBC forecast 3.5% annual total private sector LCI); and

- Further evidence that Q2/Q3 GDP growth is significantly weaker than current forecasts (WBC -0.2 qoq perhaps with some downside risks).

- A first easing to occur at the October meeting, would likely require:

- The RBNZ to have foreshadowed some probability of an October easing at the August Statement and a much larger probability of a November easing; and

- A moderate downside surprise in the Q2 CPI on 17 July, including the non-tradables component. This should be sufficient to suggest some additional and ongoing progress in reduced core inflation pressures; and

- A significant upside surprise in the unemployment rate in the Q2 labour market data on 7 August, and clear signs that wage inflation is dissipating more quickly than had been expected; and

- Confirmation of a marked decline in activity in the Q2 GDP report on 20 September (WBC forecast -0.2 qoq – perhaps with downside risks); and

- More evidence of weak activity, expanding spare capacity and easing inflation indicators in the Q3 QSBO on 1 October; and

- Signs that tax cuts in late July aren’t significantly increasing economic momentum or reducing excess capacity unduly.

- For a first easing to occur at the November meeting, we would likely need to have seen the following:

- Sufficient broad-based weakness in the Q2 and Q3 CPIs (17 July and 17 October), including in the non-tradables component of the CPI that suggest that inflation is clearly on track to move close to the midpoint of the target in 2025 (WBC Q3 forecasts 1.1% qoq total/1.4% qoq non-tradables); and

- A moderate upside surprise in the unemployment rate in the Q2 and Q3 labour market data on 7 August and 6 November respectively (WBC Q3 forecast 4.9%), and signs that wage inflation is dissipating more quickly than had been expected; and

- Confirmation of a decline in activity in the Q2 GDP report on 20 September; and More evidence of weak activity, expanding spare capacity and easing inflation indicators in the Q3 QSBO on 1 October; and

- Signs that tax cuts in late July were not leading to a greater lift in household spending than the RBNZ had expected.

- For the first easing to occur at the February 2025 meeting, we would expect to see something like our current Economic Overview outlook to evolve with a focus on the inflation outlook in particular.