{kind=link}

- The RBNZ left the OCR at 5.5% as expected.

- The RBNZ took a more dovish view – easing looks to be coming earlier than they previously thought.

- The short-term inflation outlook seems more comfortable for the RBNZ.

- But it’s the weaker growth momentum that seems especially top of mind.

- The RBNZ’s monetary policy strategy is shifting towards preparing for a reduction in restrictiveness. The RBNZ is “keeping it tight” but looks forward to easing earlier.

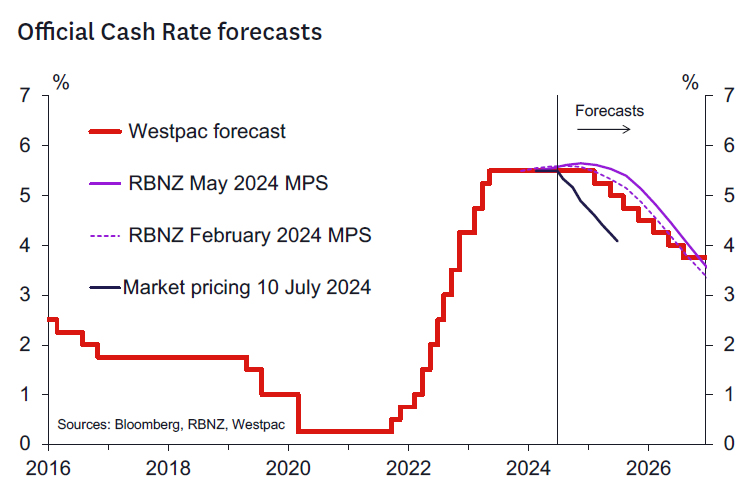

- We see this as consistent with our forecast of an initial easing in February 2025 with some chance of a November easing.

The RBNZ left the OCR unchanged at 5.5% as expected but took a more dovish tone on the outlook.

As we discussed in our Monetary Policy Review preview note, a key area of interest was the RBNZ’s updated assessment of the forward growth situation given recent weaker economic indicators that have seen markets price in a significant chance of interest rate cuts in 2024.

The RBNZ’s commentary indeed reflected concerns that the forward growth profile looks weaker than before. In particular, the record of the meeting noted that:

“…recent higher frequency indicators suggest that nearterm growth in business activity has weakened. A range of business and consumer surveys, and higher frequency spending and credit data, all point to declining activity.”

This contrasts with the May Statement, in which the RBNZ forecast low but positive GDP growth over each quarter of this year. This suggests that the RBNZ will revise down its GDP growth forecasts in the August Statement, and with that project a more negative output gap and so weaker domestic inflation pressures. The record also noted that:

“….recent survey measures of hiring intentions and job vacancies indicate flat employment levels.”

Fiscal policy.

Regarding fiscal policy, the record of meeting suggests less concern about Budget 2024 than we had expected, especially considering the comments made in the May Statement. The RBNZ noted that lower government spending has already been contributing to weaker demand and it expects that this will continue over the period. It was noted that the positive impact of impending tax cuts on private spending is yet to occur. However, at this stage the RBNZ regards the magnitude of that impact “more uncertain”. We think that part of that uncertainty likely stems from uncertainty regarding the near-term direction of the economy, with current levels of consumer pessimism likely to dampen some consumers’ willingness to spend these cuts.

Inflation.

The RBNZ also sounds more confident about the outlook for inflation, noting that it is expected to return within the target range “…in the second half of the year.” Previously, the RBNZ noted that this was expected to occur “…by the end of 2024.”

The RBNZ’s rhetoric around medium term inflation risks has been dialled back. The RBNZ notes that:

“Domestic inflation measures remain more persistent, but growing excess capacity in the domestic economy provides greater certainty that they will sustainably decline.”

They also seem to have taken some comfort from recent business surveys which have shown an easing in both cost pressures and the number of businesses who have been raising their prices.

Monetary policy strategy.

We didn’t think the RBNZ would have any significant change in message to communicate and wouldn’t be keen to endorse recent dovish market pricing suggesting meaningful chances of OCR cuts by the end of 2024. This was wrong.

While the RBNZ’s commentary was very short, the tone of the commentary suggests a change in strategy is coming. The title of the statement “Inflation approaching target range” and the final sentences:

“The Committee agreed that monetary policy will need to remain restrictive. The extent of this restraint will be tempered over time consistent with the expected decline in inflation pressures.”

are revealing in that the RBNZ is moving towards dialling back restriction as inflation falls closer to target. This tells us that the May Statement interest rate track is now stale and that current projections are consistent with an earlier start to easing. To some extent this follows the prevailing trend among developed market central banks to start dialling back restriction once the inflation target range nears. It also reflects the weaker economic data of late and it may also reflect the sense that once inflation is inside the target range the RBNZ can and perhaps will be more relaxed.

This is comforting given the RBNZ’s previous forecast start to the easing cycle was 6 months beyond most domestic forecasters (including our own February 2025 call). The question is the implied extent of the shift in strategy. Our sense is that the “feasible set” for initial RBNZ easing lies in the November 2024 to February 2025 range now.

The extent of the shift in view will come at the August Statement and with the benefit of the Q2 CPI and labour market reports due in coming weeks. Should the CPI report in particular print noticeably below the RBNZ’s 0.6% published forecast (we suspect their internal forecast is lower than this now) then this could open up a shift to a November easing forecast – although we still think this is a stretch.

Key will be their confidence on the medium-term inflation outlook as opposed to the proximity of the 1-3% target range “The extent of this restraint will be tempered over time consistent with the expected decline in inflation pressures” (our emphasis added).

The RBNZ is setting markets up to price an earlier easing start dependent on the inflation data to come. They are clearly not yet there – or easing would have started – but they no longer are discussing tightening. The RBNZ also are discussing the beginning of a measured rate cut cycle – presumably in line with the evolution of inflation outcomes. We don’t think this is the beginning of the GFC style swift and severe OCR reduction campaign (unless the economy and inflation take a step down commensurate to the much weaker scenario seen in over 2008/09).

Our OCR view.

We retain our call for first cut to the OCR to 5.25% in February 2025. It’s comforting to see the RBNZ move back towards us but it’s not clear they have vaulted us at this point. The RBNZ may have moved back to where they were in February this year where our views were closely aligned. We will be watching the inflation data most carefully to see if it is able to provide the confidence that an earlier move down in the OCR is more likely. The non-tradable inflation components will be top of mind in that regard.

Data to watch.

Key data to watch between now and the August Statement include:

- The June quarter CPI (17 July) where the level of core inflation will be especially key (headline CPI forecasts: RBNZ May 0.6% q/q, WBC 0.6% q/q, non-tradables CPI forecasts: RBNZ February 0.8% q/q, WBC 0.8% q/q).

- The June quarter labour market reports (7 August) where further signs of labour market loosening will be sought (unemployment rate forecasts: RBNZ May 4.6%, WBC 4.6%, private sector LCI wages forecasts: RBNZ May 0.9% q/q, WBC 0.8% q/q).

Market reaction.

Markets have reacted significantly to today’s significant change in tone from the RBNZ. At the time of writing, markets are pricing around a 60% chance of a 25bp easing at the August MPS meeting and have more than fully priced a 25bp easing by the time of the October OCR review.