after posting the smallest monthly gain in three years in May (0.16%). While a bounce back in core services ex-housing is likely to propel the pickup, favorable seasonal factors and broadly easing price pressures should mitigate the extent of June's rebound.){kind=link}

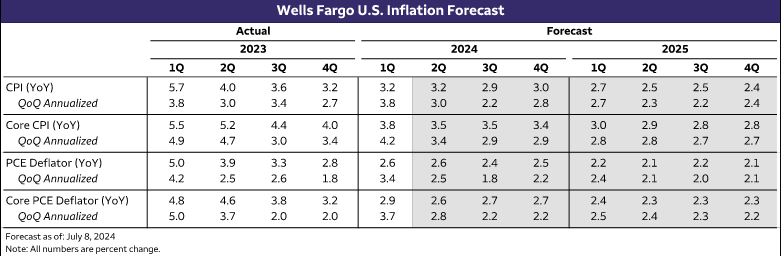

Summary

Consumer price inflation likely firmed in June relative to May but remained on a downward trajectory through the month-to-month noise. We estimate headline CPI rose 0.1% in June, with a decline in gasoline prices helping keep the overall increase in prices tame. The core index also looks to have rebounded slightly. We expect core CPI to register a “high” 0.2% gain (0.24% before rounding) after posting the smallest monthly gain in three years in May (0.16%). While a bounce back in core services ex-housing is likely to propel the pickup, favorable seasonal factors and broadly easing price pressures should mitigate the extent of June’s rebound.

Overall, we expect June’s CPI report be consistent with inflation slowing on trend. A 0.24% increase in June would be a noticeable step down from the 0.35% average monthly pace registered in the first quarter. If realized, the three-month annualized rate of core CPI would slow to 2.8% from 4.5% in March and 3.3% in December. While additional improvement on the inflation front is likely to remain slow-going when compared to the rapid reduction registered over 2022 and 2023, we continue to expect inflation to grind lower in the months ahead as input cost pressures ease and more tepid consumer demand makes it harder to raise prices.

Less Favorable than May, but Clear Improvement from Q1

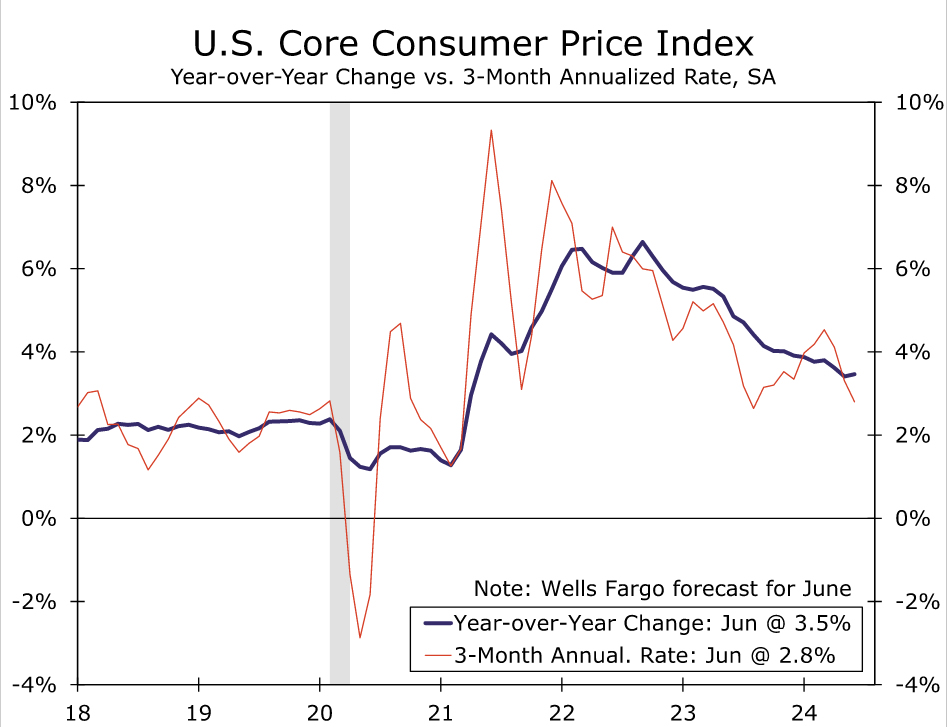

Last month’s CPI report delivered the first clear piece of good news on inflation this year. The Consumer Price Index held steady in May, marking the first month prices did not increase since the summer of 2022. Excluding food and energy, prices advanced 0.16%, which was the smallest rise in nearly three years and a tenth below consensus expectations. The CPI’s tamer readings were echoed by the PCE deflator, the Fed’s preferred inflation gauge. The core PCE index rose 0.08% over the month, half the pace of the FOMC’s 2% target when measured on an annualized basis.

May’s soft inflation data leave some wiggle room for the next few inflation prints to come in a little stronger yet still give the FOMC the “greater confidence” it seeks that inflation is on its way back to 2% on a sustainable basis. That bit of extra space could come in handy following June’s inflation data to keep a September rate cut on the table. We look for the core CPI to come in slightly higher on an unrounded basis (0.24%), although that would still mark a step down from the 0.35% average registered in the first four months of the year. The resumption of the downward trend in core inflation should be made evident by the three-month annualized rate slowing to 2.8% from 4.5% in March and 3.3% in December, even as the year-over-year rate moves a touch higher (Figure 1).

Headline CPI should also indicate that while price growth strengthened a little in June, the trend is slowly becoming more benign. We estimate the headline index rose 0.1%, which would push the year-over-year rate back down to 3.1%. Gasoline should lead to another sizable decline in energy goods prices (3.6% on a seasonally adjusted bases by our estimate). However, with oil and gasoline prices drifting up in the early days of July, the dampening effect will likely be short-lived. Meantime, after declining in each of the past two months, energy services costs are likely to rise following May’s jump in natural gas prices.

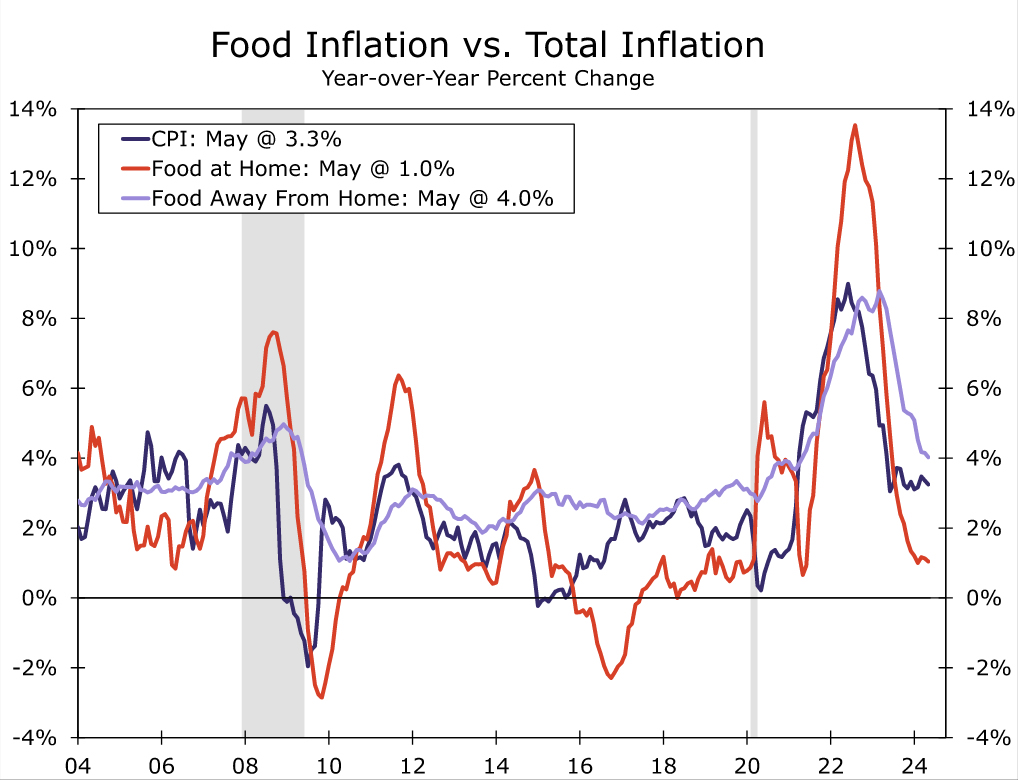

Consumers at least look to have gotten a bit more breathing room at the grocery store. We estimate prices for food at home were flat to down slightly last month amid growing promotional activity and a few major retailers recently announcing price cuts that are likely to pressure competitors’ pricing. That should leave prices up just 1.0% on a year-ago basis compared to the recent zenith of 13.5% hit in the summer of 2022 (Figure 2). Price growth for food away from home should also moderate as labor costs and inflation-adjusted sales have weakened in recent months.

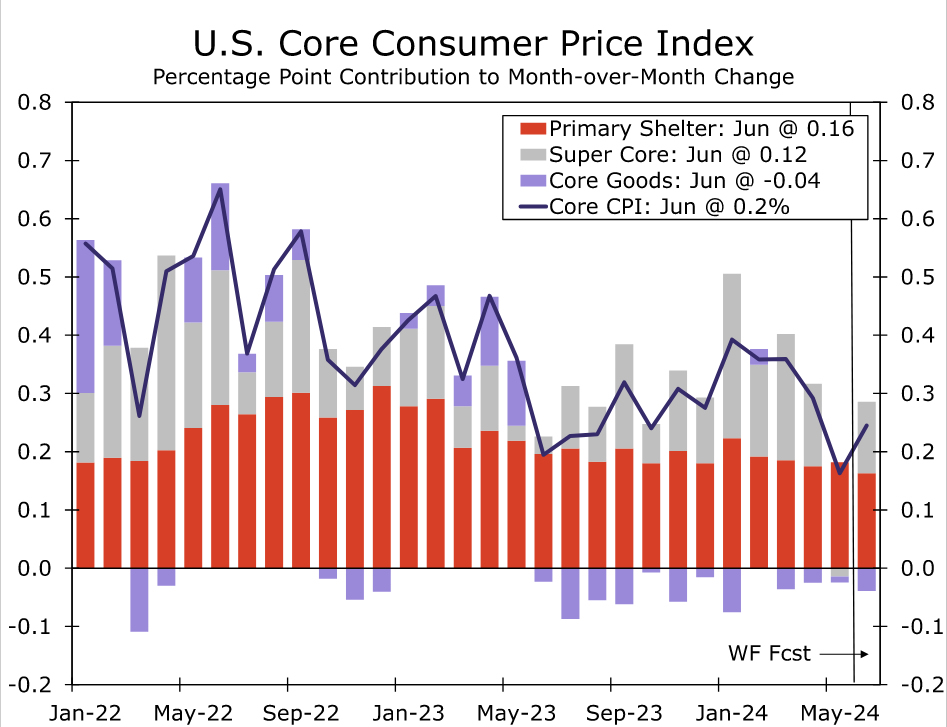

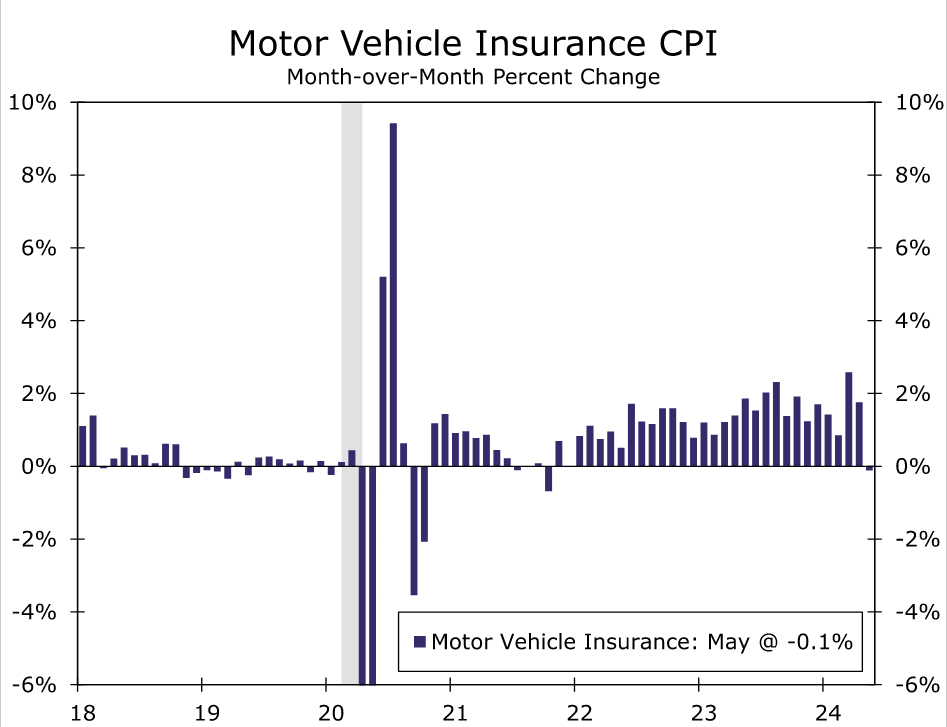

The sources of May’s downside surprise to core CPI leave us expecting a little payback in June’s gain. That said, we expect the degree of the bounce-back to be mitigated by broad easing in price pressures and favorable seasonal factors. Specifically, we look for June’s firmer core reading of 0.24% to be driven by services less housing (Figure 3), with the CPI “super core” up 0.4% after holding steady in May. Fueling the pickup is likely to be a rebound in motor vehicle insurance after an outright decline last month. While improved profitability at auto insurers points to motor vehicle insurance inflation downshifting from the breakneck pace of the past year, last month’s abrupt drop likely overstates the pace of moderation (Figure 4). More stable fuel prices also suggest prices in the volatile public transportation category (largely airfares) being little changed in June after falling 3.1% in May. Recreation and personal services prices also look ripe for a pickup after declining in May.

Yet beyond the “super core,” the downward trend in primary shelter remains in place, which we expect will lead to a further moderation in the monthly rate of primary rent of residences and owners’ equivalent rent gains in June. At the same time, we look for core goods to decline more sharply in June (-0.2% after being unchanged in May). Vehicle prices remain under pressure from improved inventory and elevated financing costs, while the jump in prescription drugs and tobacco products that buoyed other core goods in May is unlikely to be repeated in June.

A return to more normal calendar year pricing patterns may also help keep core inflation from springing back sharply in June. Over the past five years, June has trailed only January and February in average monthly price increases on a non-seasonally adjusted basis, leading the June seasonal factor to “expect” a relatively large increase. However, prior to COVID, core prices in June typically rose less than the calendar year average. If businesses are no longer raising prices as significantly mid-year as the pricing tumult of the pandemic fades, the weakening trend in inflation could be amplified by the June seasonal factor.

Downward Pressure on Inflation Still in Place

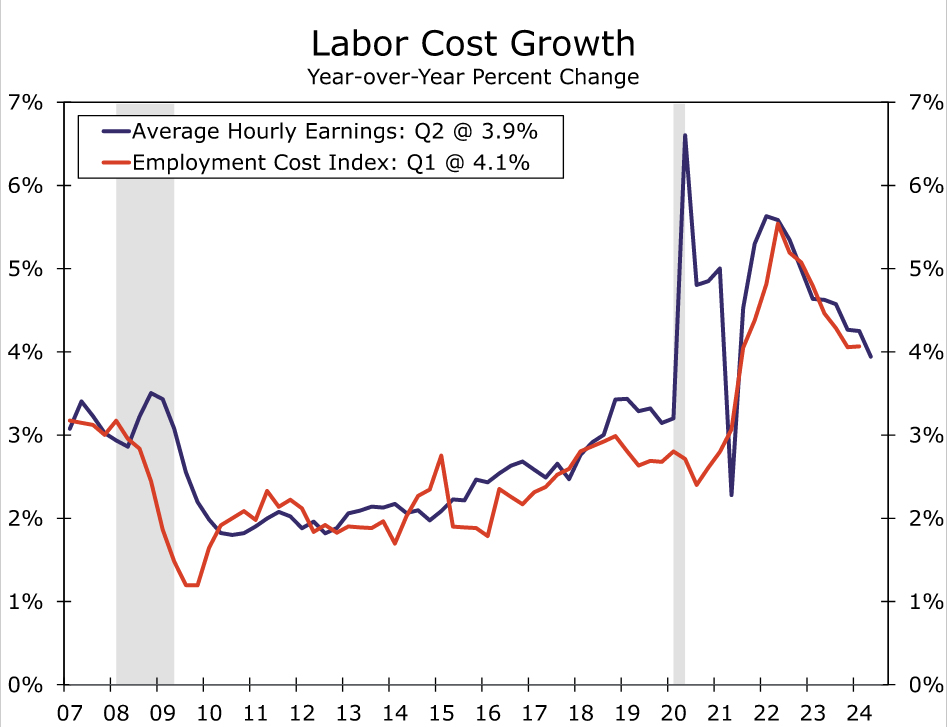

We continue to expect inflation to grind lower as we move through the second half of the year and into 2025 as overall price pressures are abating. While further improvement in supply chains is likely to be more modest ahead, more tepid consumer demand is likely to keep a lid on goods prices. Increasingly cost-conscious consumers are also likely to limit the extent of price increases across the service sector, while slower growth in input costs, including labor, is reducing the need to do so (Figures 5 & 6).

Additional improvement, however, is likely to remain slow-going when compared to the rapid reduction in inflation that occurred over 2022 and 2023. Headline CPI on a year-over-year basis is unlikely to break significantly below the bottom end of the past twelve months’ 3.0-3.7% range as energy prices are more stable, although the core CPI should continue to ebb as the slowdown in market rents feeds further into shelter prices and non-food and energy goods prices fall further. The core PCE deflator is likely to show less improvement on a year-over-year basis given its smaller weight for shelter and tough base comparisons after the sharp slowdown in prices in the second half of last year. However, when measured on an annualized basis, it should be clearer to the Fed that inflation is more closely nearing its mark (Figure 7).