. We keep a close eye at the long end of core bond curves to see whether yesterday’s move was a one-off repositioning or whether more is at hand.){kind=link}

Markets

The sell-off at the long end of the US Treasury curve was the odd one out yesterday. The US Note future slid from start to finish with tenors from 7- to 30-yr adding around 8 bps. From a technical point of view, this lifts the 10-yr yield away from the recent lows/support zone near 4.20%. The front end of the curve (2-yr) is still stuck near 4.70%. Yesterday’s move stood out given that it occurred in what was mostly a risk-off session with European stock markets throwing away opening losses, the dollar marching to new short-term highs and French assets underperforming. The move also occurred in the run-up to tomorrow’s May PCE deflators which should be a benign outcome after May CPI releases. On top, it coincides with the traditional build-up towards the end-of-quarter which often sees beneficial flows towards bonds. Our best guess for yesterday’s underperformance of US Treasuries has to do with tonight’s presidential debate between Biden and Trump. None of them seems to have reigning in ailing public finances as a top priority. On the contrary, fiscal policy could remain expansionary. Former NY Fed governor Dudley highlighted the matter again yesterday in an opinion piece. Markets tend to forget that the CBO last week upgraded the fiscal 2024 budget deficit forecast from $1.5tn to $1.9tn. To know that longer-term studies by that same Congressional Budget Office already point at budget deficits of more than 5% of GDP for the next 30 years. In this respect, Dudley warns that the more the government borrows, the greater the change it’ll end up in a vicious cycle in which government debt and interest rates drive one another inexorably upward. “It’s impossible to know when investors will decide that such risks are too much to bear, as the bond vigilantes famously did in the 1990s. When it happens, it tends to be sudden and brutal”.

News flow is thin this morning apart from more verbal intervention warnings by Japanese top officials as USD/JPY holds above 160. EUR/USD trades south of 1.07 and is likely to stay there ahead of and after the first round of French parliamentary elections (Sunday). We keep a close eye at the long end of core bond curves to see whether yesterday’s move was a one-off repositioning or whether more is at hand. Apart from the above-mentioned presidential debate, the eco calendar contains EC confidence data, US weekly jobless claims and durable goods orders. We don’t expect these figures to be of any importance. The US Treasury concludes its end-of-month refinancing operation with a $44bn 7-yr Note sale and there are policy meetings in Sweden, Turkey and the Czech Republic.

News & Views

In its yearly regular stress test of US largest banks, the Fed concluded that “while large banks would endure greater losses than last year’s test, they are well positioned to weather a severe recession and stay above minimum capital requirements”. The greater loss compared to last year comes from substantial increases in banks’ credit card balances with higher delinquency rates, riskier corporate credit portfolios and higher expenses and lower fee income in recent years. The hypothetical scenario includes a severe global recession with a 40% decline in commercial real estate prices, a substantial increase in office vacancies, and a 36% decline in house prices. The unemployment rate rises nearly 6-1/2 percentage points to a peak of 10%, and economic output declines commensurately. The Board also conducted an exploratory analysis, including two funding stresses to all banks tested and two trading book stresses to only the largest and most complex banks. The two funding stresses include a rapid repricing of deposits, combined with a more severe and less severe recession. The trading book stresses included the failure of five large hedge funds under different market conditions.

Japanese retail sales beat consensus in May, rising by 1.7% M/M and 3% Y/Y, compared to 0.8% M/M and 2% Y/Y in April. Even as some of the gains might be due to price increases, the data are supportive for the BOJ’s aim to support domestic consumption via higher wages. The data also suggest that Japanese consumption might support Q2 economic growth after a contraction the first quarter. (Q1 GDP contracted 0.5% with consumption even declining 0.7% Q/Q).

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative (France) dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

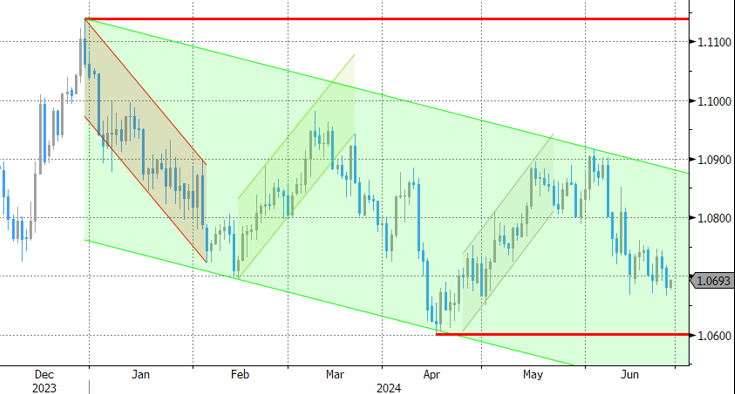

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. At the same time, the euro remains vulnerable to political event risk going into the French elections. EUR/GBP 0.84 is becoming solid support.