.){kind=link}

Markets

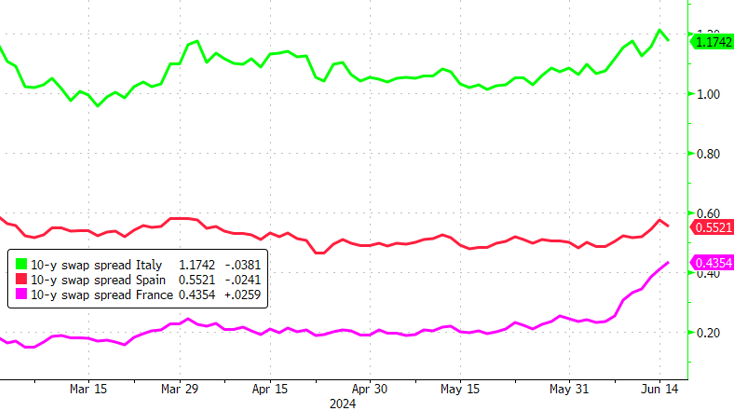

A sense of calm returned to European markets for now. Le Pen from the poll-leading Rassemblement National sought to reassure investors on the budgetary front if her party were to win the elections. It may have helped to stop the rout in European/French assets in a daily perspective after a disastrous week. Equities in the region stabilize and in some cases eke out a small gain (EuroStoxx50 +0.5%). Global core bond yields add a few basis points as safe haven bids ease for the time being. US rates rise between 4 (2-yr) and 7.8 (30-yr) bps. The move offer the likes of the 10-yr yield some wiggling room north of the lower bound of the short-term downward trend channel. German bunds tentatively underperform, adding 5.3 to 6.3 bps across the curve with the 10-yr yield trying to undo Friday’s break below the 2.4% support level (38.2% retracement on the 2024 rally, mid-May correction low). 10-yr spreads vs swaps creep a few bps higher in the case of Germany but decline for the likes of Italy, Spain and Portugal. France’s is up but is biased due to a benchmark change. It’s worth noting that several ECB members are not (yet, at least) concerned with the European repricing. Both chief economist Lane and de Guindos said it happened orderly and with sufficient liquidity, suggesting the Transmission Protection Instrument won’t be deployed any time soon. The former also touched on monetary policy but did not want to speculate on rate cuts even though he labeled every meeting as a live one. Either way, the current phase is about remaining restrictive. The euro struggled in Asian dealings but for now manages to hold north of EUR/USD 1.07. It does eke out a nice gain against sterling in the wake of the pound’s failed test of the EUR/GBP 0.84 support zone. The pair is currently changing hands in the 0.846 region. In a final sign of markets starting the week with a less grim mood, EUR/CHF recovers some of the lost ground (0.956, up from 0.952 at Friday’s close).

News & Views

Both the Swiss Federal State department for Economic Affairs (SECO) and the KoF Economic Institute updated forecasts for the Swiss economy. SECO slightly upwardly revised economic growth for this year to 1.2% (from 1.1% in March), leaving growth still at a below-average pace. SECO sees a difficult environment for investments this year. Exports will offer some degree of support, but growth should mainly be driven by private consumption, buoyed by a further rise in employment and a fairly stable rate of inflation. The latter is expected to average 1.4% this year (vs 1.5% in March). For next year SECO expects growth (1.7%) to return closer the historical average also supported by better exports and investments. Inflation is expected to cool further to 1.1%. Growth expectations from the KoF Institute are close to SECO (2024 1.2%, 2025, 1.8%). The Institute is slightly more optimistic on disinflation (1.3% this year and 1.0% next year). In this context, KoF expects the SNB to cut rates by other 25 bps this week with an additional step to 1.25% in March next year. This week’s SNB decision might be affected/complicated by recent swings the Swiss franc. End May, Governor Jordan warned that a weaker franc at that time could be a risk for the inflation outlook. However, after Jordan’s comment and due to the European risk-off last week, the franc again trades about 4.0% stronger against the euro compared to end May, raising the chance of a SNB rate cut Thursday.

Polish core inflation decelerated further in May, the national bank reported. CPI excluding food and energy prices slowed to 0.1% M/M and 3.8% Y/Y (from 0.7% M/M and 4.1% ) in April. A similar trend was also visible for the series excluding administered prices (0.1% M/M and 2.4% Y/Y from 1.2% M/M and 2.3%) and the series excluding most volatile prices (0.3% M/M and 3.1%). The data confirmed the trend in the release of headline May inflation published by the Statistical office end last month (0.1% M/M and 2.5% Y/Y). Despite current softening in the inflation dynamics, most NBP members including Governor Glapinski see no room to cut rates this year as they see inflation rising back above 5.0% in H2 2024 due to a phasing out of price caps by the government and as high real wage growth might support demand and prices. The zloty rebounded from EUR/PLN 4.38 to 4.357 today, but this was mainly driven by a softening in E(M)U related risk sentiment that weighed on the currency last week.

Graphs

German 10-yr yield seeks to recover lost support at 2.4% as calm returns at the start of the week

Peripheral swapspreads decline a few bps in a sign of market stress easing slightly

EUR/PLN: Polish zloty catches a breather after European risk off pushed the currency (and other regional peers) lower

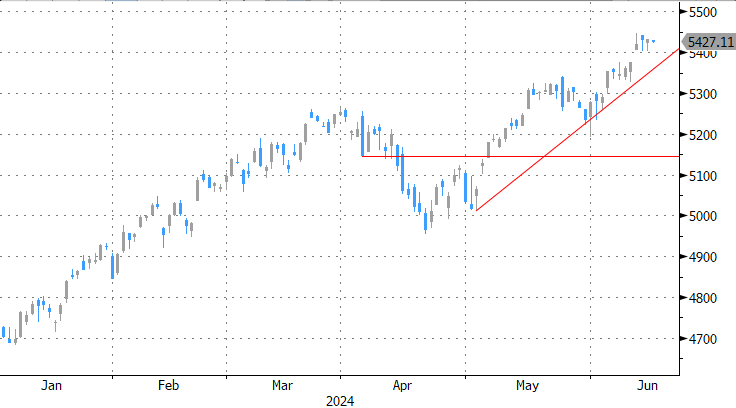

S&P500 – unfazed by European risk-off last week – opens near record highs as markets look for direction