of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.){kind=link}

U.S. Highlights

- In a widely expected move, the Federal Reserve held the policy rate steady in the target range of 5.25%-5.5%.

- FOMC participants now expect fewer rate cuts this year, with the median projection showing just one cut by year-end (previously three).

- Consumer Price Index (CPI) inflation came in weaker than expected in May, with the core measure recording its softest monthly gain since August 2021.

Canadian Highlights

- A quiet week for Canadian economic data had fixed income markets taking their cue from the U.S. The Federal Reserve left interest rates unchanged, but an encouraging inflation report led markets to take yields lower.

- The national balance sheet data for the first quarter had some encouraging news. Canadians’ net worth improved, in part due to greater thrift among households.

- Household leverage and the debt service ratio have moved down a bit. Half of mortgages are still set to renew at higher rates over the next couple of years, and we will be watching how that burden evolves given the implications for consumer spending.

U.S. – The Data Will Light the Way

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

In a widely expected move, the Federal Reserve kept its policy rate unchanged holding the target range at 5.25%-5.5% for the seventh consecutive meeting. Accompanying the announcement, the FOMC also released a revised Summary of Economic Projects (SEP). In terms of the macroeconomic forecasts, there were few changes made relative to March. Expectations for growth this year and next remained unchanged at 2.1% and 2.0%, respectively, while the unemployment rate saw a modest upward revision of 0.1 percentage points in 2025 (to 4.2%) and 2026 (to 4.1%). The inflation forecast was nudged higher, with core PCE now expected to hold steady at 2.8% (previously 2.6%) through year-end, before slipping to 2.3% (previously 2.2%) by the end of the next year.

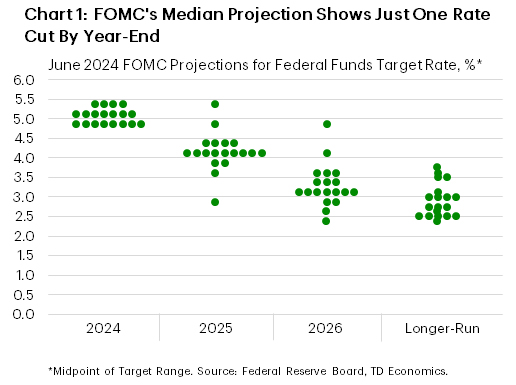

The most notable change in the SEP came from the Committee’s view on the future expectations of the policy rate. On the surface, the updated median Fed funds rate projection appears considerably more hawkish – now showing just one cut for this year as opposed to the three penciled in back in March. But a closer look at the dispersion of forecasts shows that FOMC members are nearly split between one (seven participants) and two (eight participants) cuts by year-end (Chart 1). Four members expect to keep the policy rate unchanged until next year.

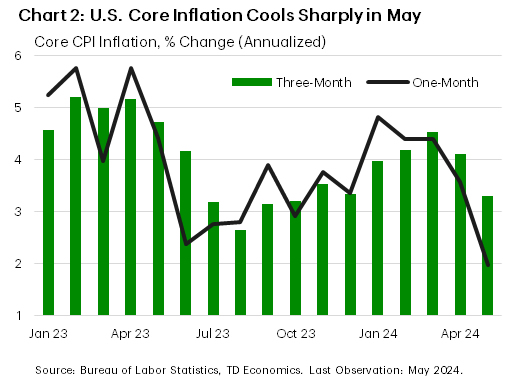

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).

During the press conference, Chair Powell acknowledged the last two softer-than-expected readings on inflation. However, he also reiterated that inflation “remains far too high” and that the FOMC needs to “greater confidence” before easing monetary policy. Whether that can be achieved over the next few months remains to be seen. As Powell noted in the press conference, “the data will light the way”.

Canada – The Upside of Higher Interest Rates

It was a quiet week for Canadian economic data, with fixed income markets cuing off signals from the U.S. Federal Reserve and a soft U.S. inflation print. One week after the Bank of Canada’s interest rate cut, bond yields are down a bit further. Canadian equity markets have had a rough week, in contrast to a stronger outturn south of the border.

The most interesting release was the first quarter national balance sheet accounts, which measures the assets and liabilities of Canadian households, businesses, and governments. All told, the story is good news. Household net worth made solid gains in the first quarter of 2024, largely thanks to healthy growth in financial assets. Net worth has now surpassed its earlier peak in the first quarter of 2022, before the housing market dipped under the weight of higher interest rates.

These gains in financial assets are not all just increases in valuations. Canadians, on net, have rediscovered saving. That is likely due to a combination of increased precautionary savings and higher risk-free interest rates providing a stronger incentive to lock money away for a rainy day. Precautionary savings likely stems from a couple of sources: 1) worries about a potential recession over the past couple of years, and 2) households facing mortgage renewals at higher rates perhaps putting some money away to pay down principal. Whatever the reason, the household savings rate ticked up to 6.9% in the first quarter of 2024, more than double the rate in the five years prior to the pandemic.

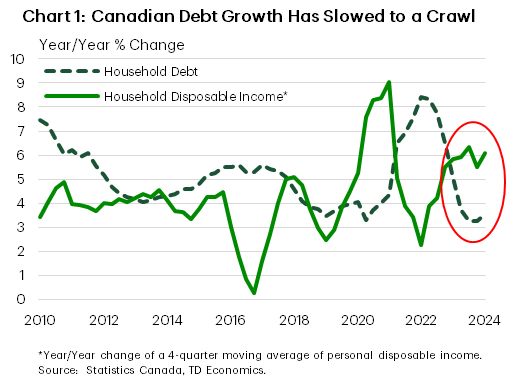

The other side of the coin in increased savings activity is less debt-financed consumption. Since the Bank of Canada (BoC) started raising interest rates in 2022, households have dramatically pared back borrowing. Canadians added debt at a very soft pace in the first quarter, and around a 3 ½% clip over the past year. This is modest on a historical basis, and now well below growth in income (Chart 1). This means that household leverage, as measured by the debt-to-income ratio, has been trending modestly downward from its peak at the end of 2021.

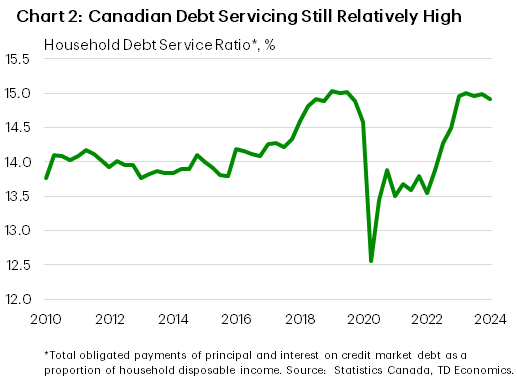

This has also helped the debt service ratio, which measures the share of total household income in Canada that goes towards servicing debt, has plateaued and come down very slightly (Chart 2). This is a better outcome than we had expected when the BoC first started raising interest rates. However, we are not out of the woods entirely yet. Many borrowers who took out mortgages at rock bottom interest rates in 2020 and 2021 will face renewals at much higher borrowing costs (see rate forecasts) over the next couple of years. According to the BoC’s Financial Stability Report released in May, about half of outstanding mortgages have yet to see payment increases due to higher rates. This is likely to keep the debt servicing burden elevated and weigh on consumer spending over the next couple of years. Thankfully Canadians have also seen their incomes grow, which should also help to cushion the strain of higher debt payments.