{kind=link}

- It will be another central-bank-heavy week with the RBA, SNB and BoE

- None are expected to cut but there’s room for surprises

- Retail sales will be the highlight in the United States

- Plenty of other data also on the way, including flash PMIs and UK CPI

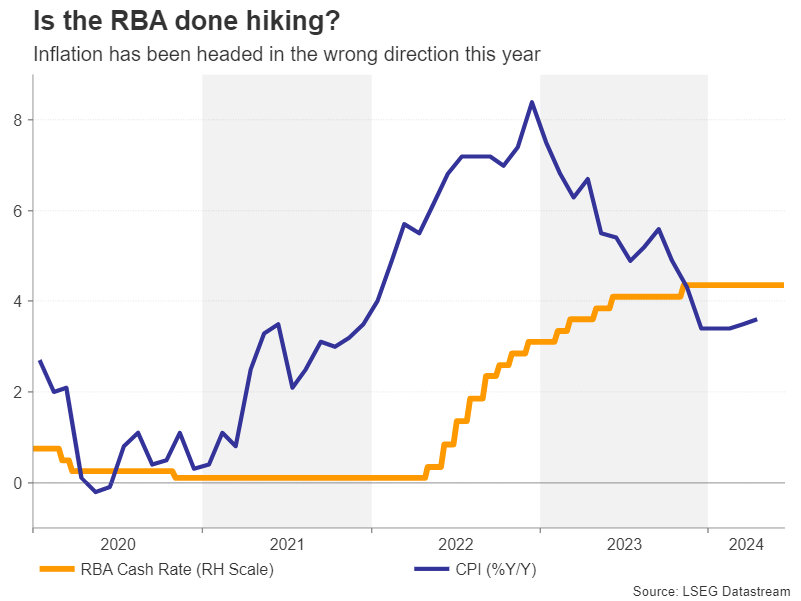

RBA is in a pickle

The Reserve Bank of Australia will keep the central bank theme going on Tuesday when it meets for its June policy decision. Like their global peers, RBA policymakers had been hoping that their job was going to get a lot easier this year. But a muddy economic picture and sticky inflation have complicated the policy path.

Inflation has been gradually edging higher all year, with the monthly CPI reading ticking up to 3.6% y/y in April, reversing some of the sharp drop seen in 2023. Meanwhile, the labour market appears to be tightening again. However, doubts about the strength of the broader economy have deterred policymakers from hiking rates. GDP grew by just 0.1% in the first three months of the year.

A rate hike was considered at the May meeting, but ultimately, policymakers judged the risks to the inflation forecasts to be balanced. The June statement will likely strike a similar tone, with the cash rate expected to remain on hold.

However, although investors have in recent weeks priced out any probability of a rate increase, the inflation trend in Australia remains more worrisome than in other countries and it may be too soon to rule out a hike. Nonetheless, any policy shift is unlikely before the August meeting when new economic projections will be available. The timing of how long it will take for inflation to fall back within the RBA’s 2-3% target band will be crucial to future rate decisions.

In the meantime, any reactions in the Australian dollar might be short-lived amid the lingering fog over the interest rate outlook both domestically and in the United States.

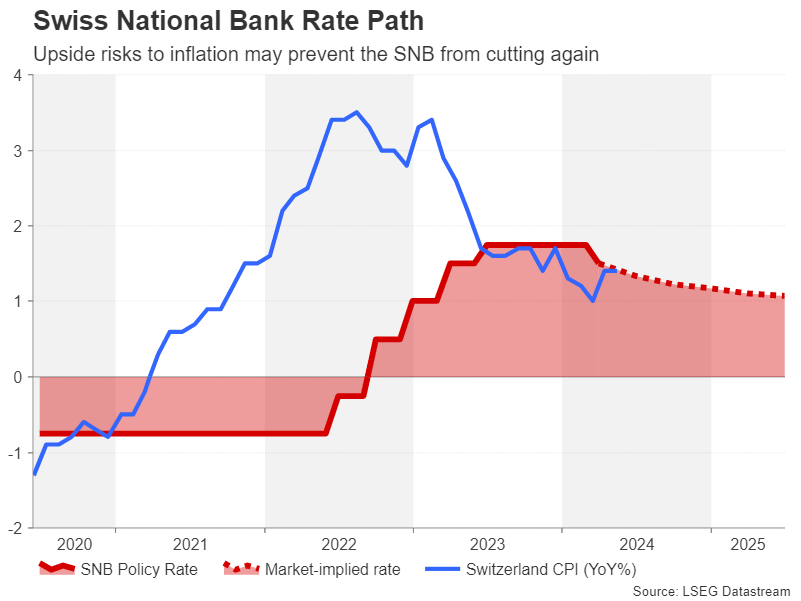

Will the SNB cut again?

The Swiss National Bank took many investors by surprise when it cut rates back in March, becoming the first major central bank to do so in this cycle. Markets see around a two-thirds probability of a follow-up 25-basis-point cut on Thursday when the SNB convenes for its quarterly gathering.

However, the recent data does not point to any urgency to ease policy so soon after the last move. GDP grew more than expected in Q1 and inflation quickened to 1.4% in April, staying unchanged in May.

The SNB has an inflation target of 0-2.0% and when adding the weaker Swiss franc into the equation, policymakers can certainly afford to wait before cutting again. Outgoing president, Thomas Jordan, even warned as much in recent remarks, citing the exchange rate as the likely source of inflation risks being skewed to the upside.

Should the SNB keep rates unchanged at 1.50% and cast doubt on the prospect of a September cut, the franc could extend its latest rebound attempt against the US dollar.

Should the SNB keep rates unchanged at 1.50% and cast doubt on the prospect of a September cut, the franc could extend its latest rebound attempt against the US dollar.

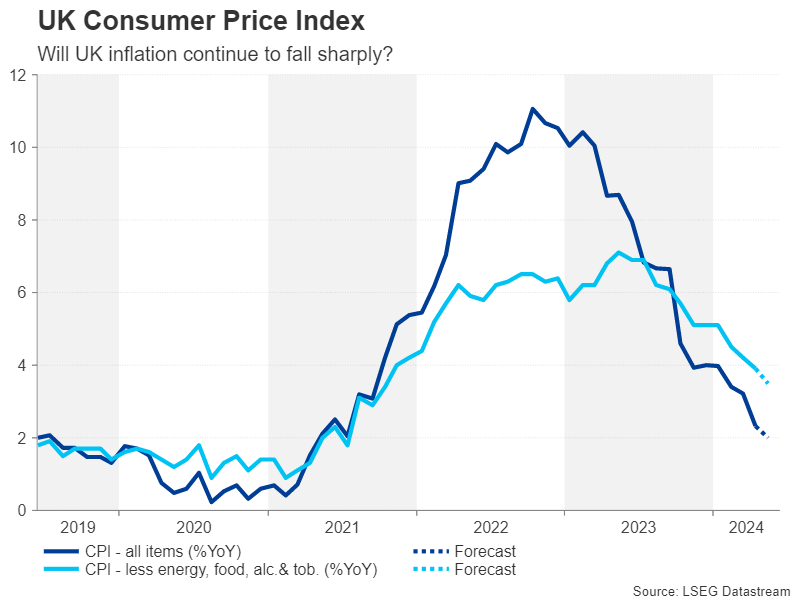

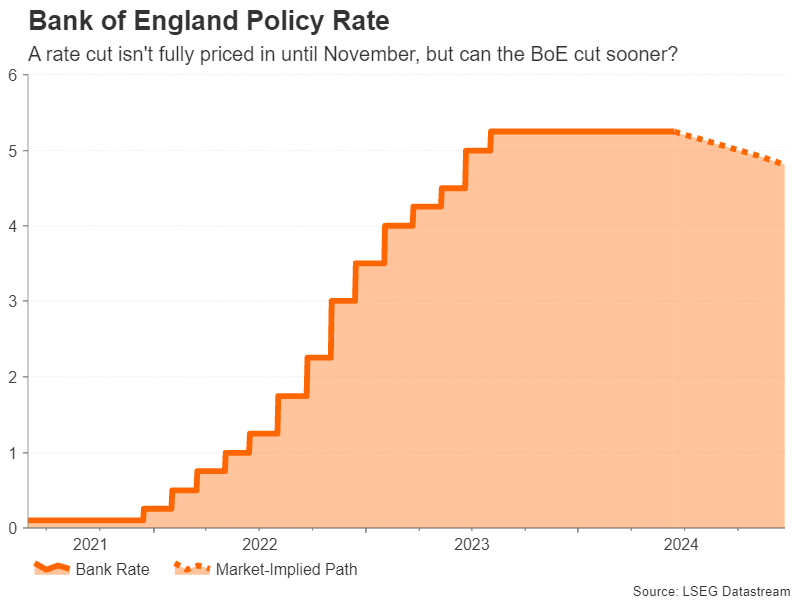

BoE: avoiding a political storm

The Bank of England will deliver the final policy decision of the week hours after the SNB, and it looks set to be a non-event. The ongoing general election campaign in the UK means that the Bank will not say or do anything that could sway voters towards any political persuasion.

This might actually come as a relief for policymakers who need more time to assess the inflation picture. Although UK CPI plunged to 2.3% y/y in April, wage growth has remained sticky at 6.0% y/y, while services inflation has not subsided much from its peak. Yet, the jobs market is clearly softening, with the unemployment rate rising for the fourth straight month in March.

In August, not only will there likely be a new government in Downing Street with a new economic agenda, but the Bank will also have access to updated forecasts. Hence, policymakers might not even tweak their statement in June, turning the spotlight to the incoming data.

The CPI numbers for May are due on Wednesday, to be followed on Friday by retail sales figures for the same month, as well as the flash PMI estimates for June.

Investors have currently assigned odds of about 40% for a cut in August, while a 25-bps reduction isn’t fully priced in until November. But markets may be underestimating the BoE’s eagerness to begin the easing cycle and should headline CPI drop below 2% in May, hopes of a summer rate cut will get a boost.

For sterling, however, soft data and dovish soundbites post the July 4 election may only have a limited impact if expectations for a September cut by the Fed also grow. Moreover, if investors view an early BoE cut as simply bringing forward the timing of one and not a shift to a more aggressive easing path, the pound’s broader outlook might not change much.

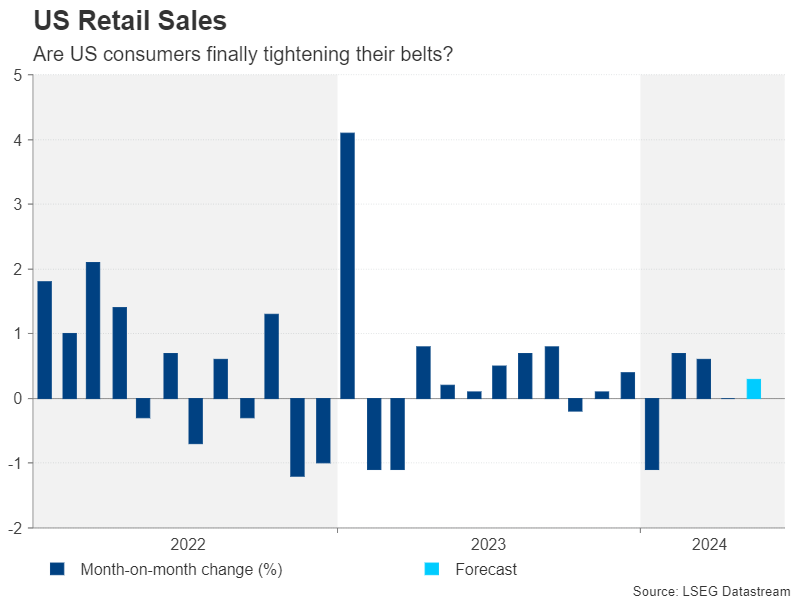

US retail sales in focus after wild week

It’s been a confusing week for Fed watchers as a soft CPI report was followed by a hawkish Fed meeting. For the dollar, its rollercoaster ride started a few days earlier from the hot jobs report. But perhaps the most telling in all this is where Treasury yields ended after all the excitement died down – at two-and-a-half-month lows.

In a nutshell, market expectations have been back and forth between one and two rate reductions for some time now and so the new dot plot signalling just one cut in 2024 wasn’t much of a gamechanger. Crucially, Fed Chair Powell left the door open to a September cut if there’s further progress on lowering inflation before then. In addition, Fed officials pencilled in more cuts for 2025 than in the March dot plot.

But the pendulum could still swing either way and Tuesday’s retail sales numbers could therefore spoil the current optimism if they show that consumer spending accelerated in May. Forecasts are for a reading of 0.3% m/m versus 0.0% in April.

Other data out of the US next week are mostly second-tier releases. They include the New York Fed and Philly Fed manufacturing gauges on Monday and Thursday, respectively, industrial production on Tuesday, building permits and housing starts on Thursday, and the S&P Global PMIs and existing home sales on Friday.

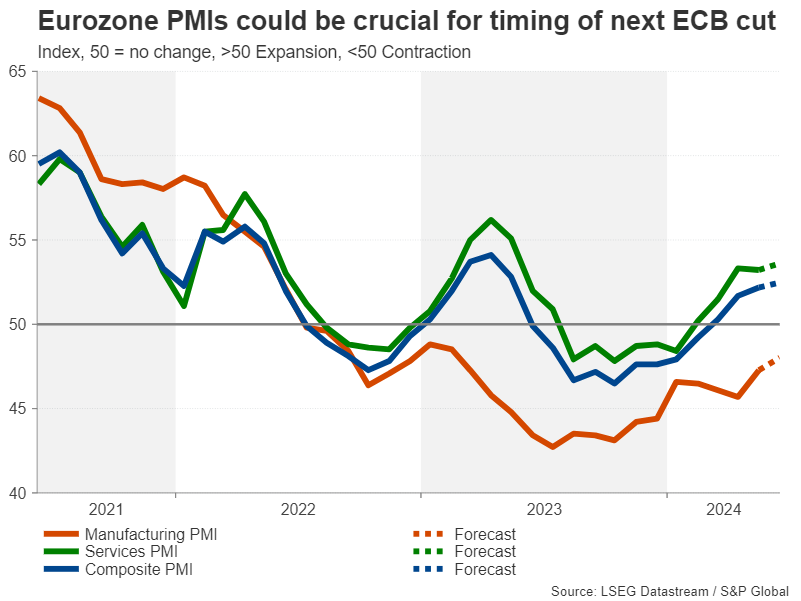

Euro hoping for a calmer week

Another currency experiencing some volatility over the past few days has been the euro. After the gains of the far right in the European Parliament election last weekend and French President Macron’s shock announcement of a snap election, a dollar selloff briefly came to the aid of the sliding euro. In the coming week, the euro’s best bet for some support will be Friday’s flash PMI figures.

An upbeat set of surveys for June could bolster the single currency as a strengthening economic recovery would dash expectations of another rate cut by the ECB in the near term. Investors will also be watching quarterly wage data on Monday, the final CPI estimates for May on Tuesday, as well as Germany’s ZEW economic sentiment index due the same day.

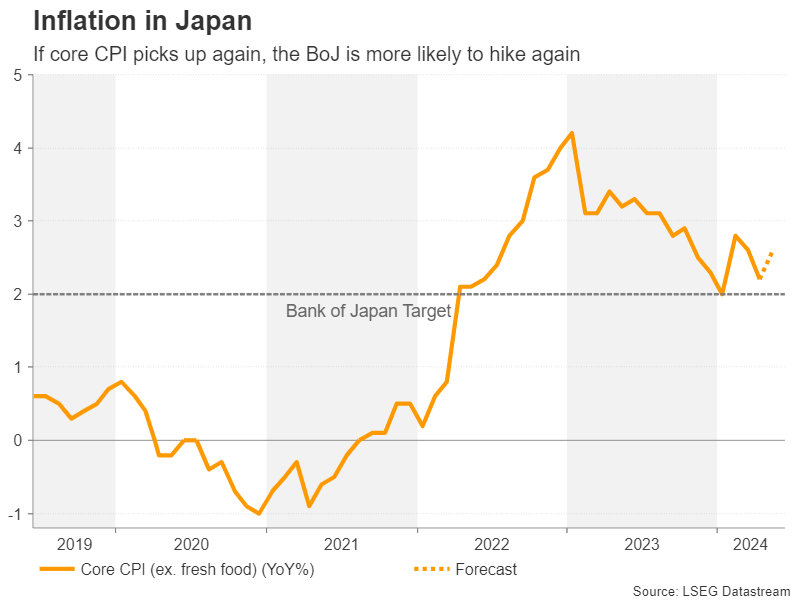

Japanese CPI and New Zealand GDP eyed too

In Japan, May inflation numbers out on Friday will be the focal point for the yen. Tuesday’s trade figures and the flash PMIs might also attract some attention.

The Bank of Japan decided this week to delay any decision on tapering its bond purchases until the July meeting. The cautious stance pulled the yen lower, but there might be some good news for the beleaguered currency from the CPI report. The core figure is expected to rise back up to 2.6% y/y in May from 2.2%, potentially adding to the case for the BoJ to further wind down its stimulus policies.

Elsewhere, the first quarter GDP print will be the highlight for the New Zealand dollar on Thursday, while at the start of the week, China’s monthly data dump that includes industrial output and retail sales figures will set the market mood on Monday.