{kind=link}

Markets

Outright risk-off from the start of trading today. French President Macron’s parliamentary election bet culminated in the current risk climate. The French president’s approval rating hit an air pocket and his Renaissance party is burnt. Nobody, stretching from left to right on the political aisle wants to join forces with the stigmatized French president going into the elections. It only raises the odds of a strong showing for the extremes. French FM Le Maire warned that a victory by the new left-wing alliance would lead to the country’s EU exit as its programme would cause an economic collapse. Risk aversion was already visible in weaker stock markets, an ailing euro and rising sovereign credit spreads. Today, basis swap risk added another layer with markets scrambling for USD liquidity. That’s a common phenomenon in global financial crises, but likely a first time just because of the European election risk. In any case, it pushed EUR/USD below the 1.07 barrier for the first time since early May. The race to the YTD low at 1.0601 remains on. EUR/GBP touched 0.84 before rebounding to 0.8430 in the current environment and with next week’s Bank of England meeting looming as (GBP) event risk. European stock markets lose another 1%-2% with the French CAC 40 underperforming (-2.36%). That makes a cumulative 6% for the week. The 10-yr French/swapspread breached 40 bps (41 currently) for the first time since H2 2012. German Bunds are back as preferred safe haven asset with German yields dropping over 10 bps across the curve, massively outperforming US Treasuries. US yields shed 1.4 bps (2-yr) to 3.2 bps (30-yr). Today’s eco calendar was empty with University of Michigan consumer confidence due later today. ECB President Lagarde is scheduled to speak after European close but already sparred with the press. For the moment she stuck with the tune that the disinflationary path will be bumpy in H2 meaning that policy rates aren’t on a pre-set path mower.

News & Views

The Bank of England/Ipsos quarterly inflation attitudes survey showed expected inflation over the coming year at 2.8% down from 3% in May. Current inflation was seen at 5.5% from 6% (headline inflation in fact was 2.3% in April, core 3.9%). The median answer for inflation in the longer term was unchanged at 3.1%. With respect to the future path on interest rates, 34% expected higher rates over the next 12 months. 42% (from 41%) expect rates to go down. Regarding the impact of interest rates on their personal situation, 24% of respondents assessed it would be better if interest rates were to ‘go up’, up from 23%. 31% of respondents said it would be better if interest rates were to ‘go down’. Asked to assess the way the Bank of England is ‘doing its job to set interest rates to control inflation’, the net satisfaction balance, was -4%, up from -5% in February 2024. Inflation expectations are important input when the BoE meets next Thursday. On Wednesday, the May UK CPI data also are still scheduled for release.

The Swedish disinflation process slowed in May. CPIF inflation (with a fixed interest rate, preferred measure of the Riksbank) increased 0.2% M/M and 2.3% Y/Y (unchanged from April), but a further decline of -0.1%M/M to 2.1% was expected. Core CPIF (excluding energy) even reaccelerated to 0.8 % M/M and 3% Y/Y (0.4% M/M and 2.9% Y/Y expected). Transportation services (6%), accommodation services (+11.2%), package holidays (19.7%) and food (0.5%) recorded price rises. At the same time, overall inflation was dampened by a sharp decline in electricity (-13.3%) and fuel prices (-2.9%). In its March monetary policy report, the Riksbank expected CPIF inflation to return to 2% by the middle of this year and to hold near that level. The Riksbank meets next on June 27, with a new monetary policy report (including new forecasts) at its disposal. As there are indications that at least part of the jump in services inflation in May might have been due to one-offs, it probably won’t profoundly change the RB’s inflation assessment. The RB might thus maintain guidance on two additional rate cuts later this year. After a protracted EUR/SEK decline since early May, the rise of the krone this week slowed. There was no sustained reaction to the May CPI data (EUR/SEK 11.27). EUR/SEK 11.15 and especially the 11.00 area are important support levels.

Graphs

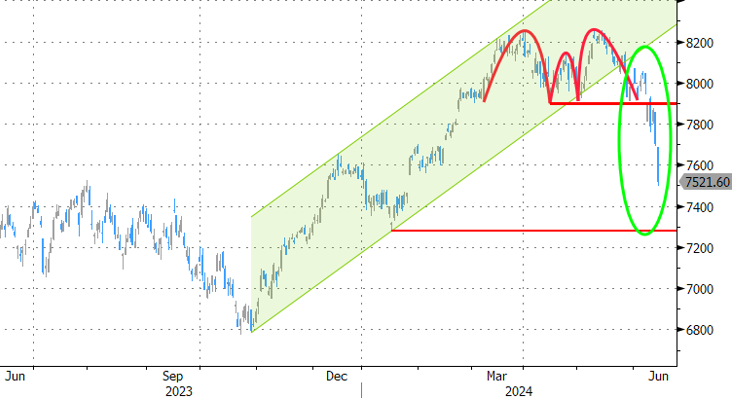

Cac40: French/EU political risk exhibit A

10yr OAT/swapspread: French/EU political risk exhibit B

EUR/USD: French/EU political risk exhibit C

EUR/USD basisswap (Estr v sofr, 3y): French/EU political risk exhibit D