and indicating only one rate cut this year as the FOMC’s preferred interest rate scenario only limited the big decline in US yields post a softer than expected US may CPI release.){kind=link}

Markets

Yesterday’s ‘hawkish’ Fed dots raising governors’ 2024/25 inflation projections, a higher reference for the neutral rate (2.75% ) and indicating only one rate cut this year as the FOMC’s preferred interest rate scenario only limited the big decline in US yields post a softer than expected US may CPI release. US 2-y and 10-y yields were saved by the bell not to drop below key support zones respectively at 4.70% (mid-May low) and 4.26% (50% retracement rise December/April & recent correction low). Still, markets clearly saw a more than 50% chance of the Fed again backtracking on its guidance and deploy two rate cuts starting in September rather December. Given Fed guidance yesterday, it would be reasonable to expect money markets to continue switching between a first Fed rate cut in September rather than December or vice-versa and above mentioned yields’ levels to provide solid support. Today’s US jobless claims and PPI data for sure are second tier compared to yesterday’s CPI. Even so, as they pointed in the same direction yesterday’s lows/key supports are again at risk. US jobless claims jumped from 229k to 242k, the highest level in nine months. US (headline) PPI even declined 0.2% M/M to slow the Y/Y-measure to 2.2% from 2.3%. Core PPI didn’t rise in May (0.0%). US yields currently decline between 3 bps (30-y) and 5 bps (5-y). Markets further embrace a September Fed rate cut (75%). Going into this evening’s sale of $ 22bln of 30-y US notes, yesterday’s and today’s moves again made treasuries far more expensive compared to Tuesday’s successful 10-y sale. Interesting the see investors’ interest at current pricing. German Bunds again substantially underperform Treasuries showing changes of less than 1 bp across the curve. ECB’s Vasle and Muller joined comments from colleagues recently that it’s too early communicate on the timing of further steps, among others as wage growth remains and upside risk to inflation. For EMU yields, especially for longer maturities, the upward tendency still holds even after recent correction. Higher EMU yields/underperformance also suggests a gradual tentative rise in EMU risk premia. In this respect, intra-EMU spreads (VS Germany) continued this week’s uptrend (France, Italy, Greece +4 bps, Spain, Portugal, Belgium, Ireland + 3 bps). Lower yields gains again don’t help (European) equities. The Eurostoxx50 again cedes 1.1%. US indices are holding near recent record levels (S&P 500 + 0.25% , Nasdaq + 0.70%).

On FX markets, the dollar, despite a diminishing interest rate differential, still marginally outperforms the likes of the euro or the yen. DXY gains modestly (104.8 from 104.7). EUR/USD struggles to hold to 1.08 big figure. USD/JPY, admittedly in low volatility trading, surpasses the 157 barrier as market await tomorrow’s BOJ decision. Markets see a chance of the BOJ reducing its bond buying. A further rate cut is expected later this summer.

News & Views

Germany’s finance ministry is considering a supplementary budget for this year, Bloomberg reported after Bild newspaper aired the news earlier today. The revision to the 2024 finance plan, which is still being discussed, would allow the government to borrow an additional €11bn on top of the net new €40bn expected before (down from €70bn). Germany’s constitutional debt brake limits deficit spending to just 0.35% of GDP. This structural component is complemented with a cyclical element, however, to smoothen out business cycles. As the economy grew more modestly than expected during the previous budget preparations, some leeway opened up for the government.

MSCI late yesterday denied debt sold by the European Union entrance to its government bond indices. The news came unexpected and is a setback for investors, who anticipated that MSCI inclusion would drastically improve liquidity and overall demand for the bonds. The current supranational status means that triple A rated EU bonds still trade with a discount compared to equally- (and in some cases even lower-)rated peers. A survey of investors conducted by the EU last year revealed that inclusion in such indices was “the single-most important remaining step in order for EU-bonds to trade and price similarly to European government bonds.” MSCI said it will re-evaluate the eligibility criteria in 2025Q2.

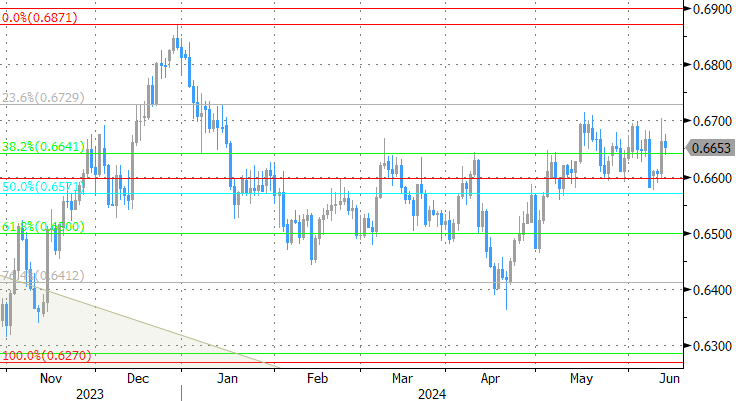

Graphs

EMU 10-y swap stays in gradual uptrend even as ECB started cutting rates. EMU risk premium in play?

US 2-y yield revisits yesterday’s lows as high jobless claims and soft US PPI challenge yesterday’s Fed guidance.

USD/JPY: dollar holding up well despite loss of interest rate support. Yen awaits BOJ decision.

AUD/USD tries upside test. Strong labour market data suggest RBA to stick to higher for longer narrative.