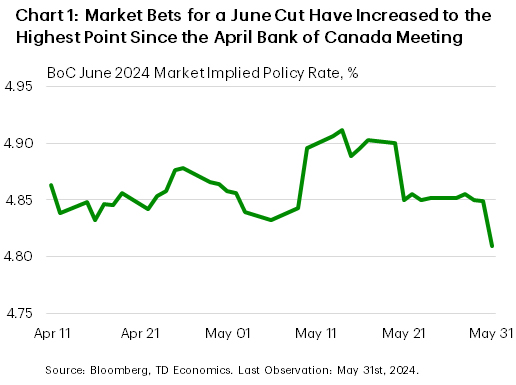

interest rate decision next week. Interest rate relief is on the horizon, but the pressing question remains whether the BoC will cut in June or July. For the past several weeks bets were skewed towards June. With first quarter GDP growth missing to the downside compared to consensus and the BoC’s estimates, the scales tipped further in June’s direction, with markets pricing in nearly an 80% chance of a move. This is the most conviction markets have had since the BoC’s April 10th meeting (Chart 1), but we’d argue that an interest rate reduction next week is not a slam dunk.){kind=link}

U.S. Highlights

- Revisions to economic growth in the first quarter featured a mark down to consumer spending.

- That theme continued in April, where a contraction in real personal consumption expenditures came as a confirmation that restrictive rates are working.

- Inflation also took another step in the right direction. But sticky services inflation still has room to fall before the Fed can feel confident that inflation has been tamed.

Canadian Highlights

- Canadian economic growth missed to the downside in the first quarter. A strong increase in domestic demand was offset by inventory drawdowns.

- As the dust settles, markets have increased their bets for a June rate cut to their highest level since the last monetary policy meeting.

- We acknowledge the risks around a cut next week, but ultimately believe the Bank of Canada will wait until July to pull the trigger.

U.S. – A Slight Downshift

Bond yields are climbing down from this week’s highs as a pair of high-profile data releases suggest the some of the steam is being let out of the U.S. economy. While there isn’t anything released this week that is going to meaningfully move the needle on the timing of the Fed’s decision, it was encouraging to see that the current restrictive policy stance is cooling the economy. That said, there is still enough strength underlying the economy to keep the Fed’s policy rate right where it is until later this year.

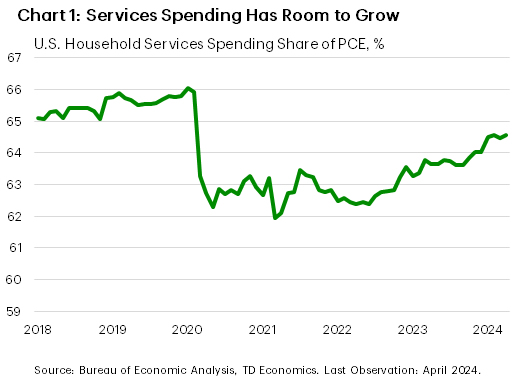

First up was the refresh of the first quarter’s GDP data. Top-line economic growth was shaved down a smidge, to a below trend 1.3% quarter-on-quarter (q/q, annualized) change. Consumer spending too was marked down, from 2.5% to a more trend-like 2.0%. That said, faced with persistently strong price growth and high interest rates, the ability of households to keep buying stuff and spending money on experiences has defied expectations. Specifically, the shift back to services spending has kept demand up on the primarily domestic portion of the economy facing a tight labor market. Moreover, there is room for this trend to run if households continue to adjust their expenditures back towards a pre-pandemic mix, where household services consumption accounted for just shy of 66% of personal consumer expenditures (compared to 64.6% as of April, Chart 1).

So, it came as a welcome surprise that April’s Personal Consumption and Expenditures (PCE) survey showed real PCE pull back 0.1% month-on-month (m/m). More good news came as the core PCE deflator edged down to 0.2% m/m, leaving the annual pace of price growth to 2.8%. That said, the three- and six-month core PCE inflation rates are still 3.5% and 3.2% (annualized), respectively, as the past few months of strong price growth continue to be felt.

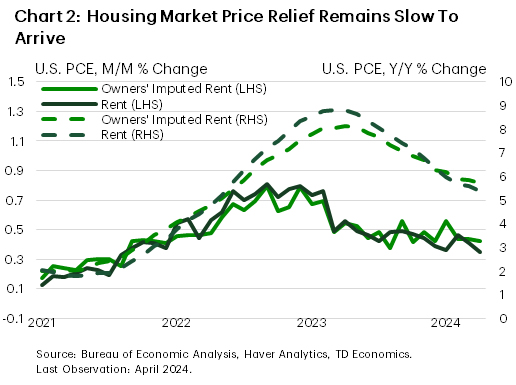

Importantly, while the deceleration in core price growth was welcome, special attention has to be paid to rents and housing costs that have been propping up core price growth. Together the two categories make up roughly 15% of PCE and will be critical to taming inflation. On this front, there was only marginal relief in April. Rent inflation came in at a “soft” 0.4% m/m (the print was 0.35% m/m unrounded). This is in line with the average reading from the prior five months (Chart 2). On the homeownership side too, implied rents came in at the same 0.4% m/m, roughly unchanged from the last few months. Sustained over a year, the 0.4% monthly pace would translate to 4.9% annual growth. The annual rates on the two shelter components are now cruising along at 5.7% and 5.4% for the imputed and actual rent measures, respectively.

For the Fed, April’s data were a step in the right direction, but there is still more work to be done before rate cuts become imminent. So now, all eyes are focused on data coming next week, and specifically the May payrolls report. After April’s real spending and payrolls data surprised to the downside, the focus will be for any signs that the month was not a one-off and weaker momentum continued into May.

Canada – Bank of Canada in Focus

Anticipation is high for the Bank of Canada’s (BoC) interest rate decision next week. Interest rate relief is on the horizon, but the pressing question remains whether the BoC will cut in June or July. For the past several weeks bets were skewed towards June. With first quarter GDP growth missing to the downside compared to consensus and the BoC’s estimates, the scales tipped further in June’s direction, with markets pricing in nearly an 80% chance of a move. This is the most conviction markets have had since the BoC’s April 10th meeting (Chart 1), but we’d argue that an interest rate reduction next week is not a slam dunk.

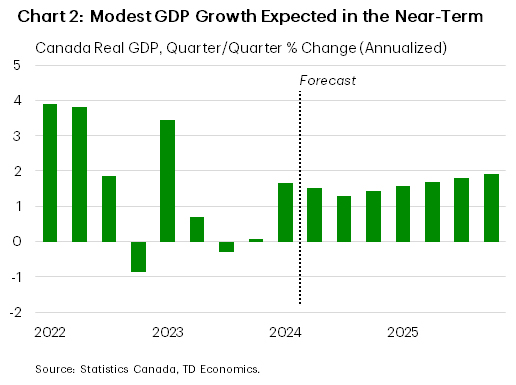

High interest rates are doing their part to cool economic activity, evidenced by the fact that economic expansion effectively flatlined for most of 2023. The Q1 GDP miss also comes on top of a downward revision to the fourth quarter, which now shows no growth. However, the details under the hood were more constructive of decent, albeit temporary, economic strength. For one, final domestic demand, a good barometer for internal economic health, grew at the fastest pace in eight quarters. Business investment and government spending contributions were also encouraging. This quarter, like many in the past two years, was heavily swayed by inventory drawdowns, which subtracted nearly 1.5 percentage points (ppts) from Canada’s GDP in Q1. We expect growth will hum along at a below-trend pace for the next several quarters (Chart 1) as the economy continues to grapple with higher interest rates.

The Bank of Canada should continue to focus their policy decisions on meeting their inflation mandate. In this sense, rate cuts have been justified for some time, especially as headline inflation has printed under 3.0% for four consecutive readings. Further, the average three month annualized change in the BoC’s preferred core measures have been sub-2% for the last two months.

Despite inflation dynamics suggesting the economy is ready for a cut, we still believe the BoC will pull the trigger in July. Firstly, Governor Macklem has only acknowledged progress, but hasn’t explicitly signaled any intention to make a move. Further, in the recent summary of deliberations, some council members stressed that the risk was lower that higher rates would slow activity more than necessary. In an effort to increase transparency and forward guidance, the Bank can use next week to tee up a July rate cut, while allowing themselves to see two more inflation prints to confirm that durable 2% price growth is in sight.

We also recently wrote about monetary policy divergence with the Federal Reserve and how much room the BoC can run on their own before risking a destabilization in the Canadian dollar. In short, this won’t be the first time that policy divergence has happened between the two central banks. Meanwhile, Governor Macklem continues to stress that the Bank will act independently. Stay tuned for Bank’s decision next week!