{kind=link}

- OPEC+ oil producers might extend current supply cuts on Sunday June 2

- Deeper cuts could be acceptable by major members but probably not for long

- Plans for capacity increases might cause some divisions within the group

- Geopolitical tensions, China outlook, and Fed rate cut path to move oil prices too

An agreement seems to be on the table already

OPEC oil producers and their allies including Russia postponed their 188th gathering for a day to Sunday June 2 and switched from an originally scheduled in-person meeting in Vienna to a virtual conference following the death of the Iranian president Ebrahim Raisi and as the Saudi King, the father of energy minister Abdulaziz bin Salman, who is also the cartel’s chairman, is in poor health.

The last-minute shift to an online meeting flagged that an agreement for members to extend their current production cuts in the second half of the year is already guaranteed. Perhaps this is the easiest and fastest solution for the time being. Distributing a potential output increase or decrease among members could lead to political disagreements within the group, given that some of them are directly or indirectly involved in the Middle East turmoil and the war in Ukraine. Note that 79.5% of global oil reserves are located in OPEC states and particularly in the Middle East.

Compliance is challenging

For instance, Iraq, which is the second largest OPEC producer and the world’s fifth largest owner of reserves, has been seeking to increase its supply by 7 million bpd since the pandemic, producing over its quota limits at the start of this year with a pledge to compensate for it in the second half of the year.

However, Iraq is known for its low degree of compliance, raising questions about whether it will indeed meet its obligations. Yet, this is a common phenomenon among OPEC members who rely heavily on oil production to ensure economic funding and avoid indebtedness. Kazakhstan has been overproducing as well during the first quarter, while Gabon seems to have no plans to compensate, with the compliance rate within the OPEC+ group easing to 96.5% in April from 97.9% in March.

Recall that Angola decided to leave the group after a 16-year membership, joining Ecuador and Qatar over a dispute on output quotas. Therefore, it will be intriguing to observe if additional oil producers jeopardize the group’s unity. Specifically, Iran, whose exports are at a six-year high, flagged a 4 million bpd boost amid economic challenges recently without providing a timeframe and the UAE also announced an output capacity increase shortly before June’s meeting. Nigeria has been expressing its dissatisfaction over restrictions on quotas too, but is still endorsing its collaboration with the organisation.

Would steeper production cuts be acceptable?

The existing plan involves a total 5.86 million bpd supply reduction (5.6% of global demand), composed by the initial 3.66 million bpd cut announced in steps since late 2022 and the additional 2.2 million bpd cut (from 1.3 million previously) led by selected members such as Saudi Arabia and Russia.

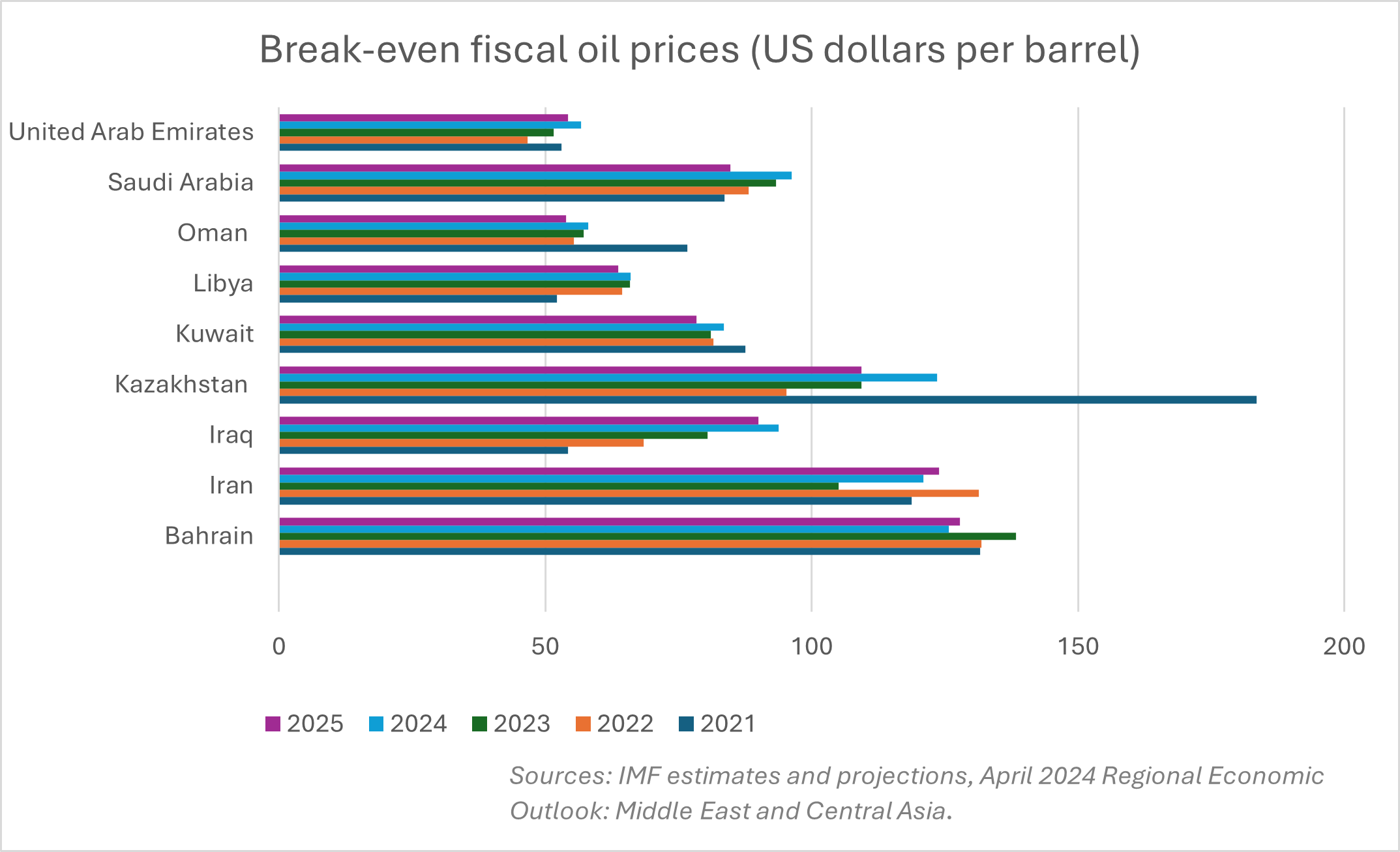

A tighter supply could boost oil prices, benefitting the key OPEC players Saudi Arabia and Russia, which have a high break-even price between $90 and $100/bpd according to the International Monetary Fund (IMF), as the former aims to fund its ambitious economic plans and the latter deals with war expenses for the second consecutive year.

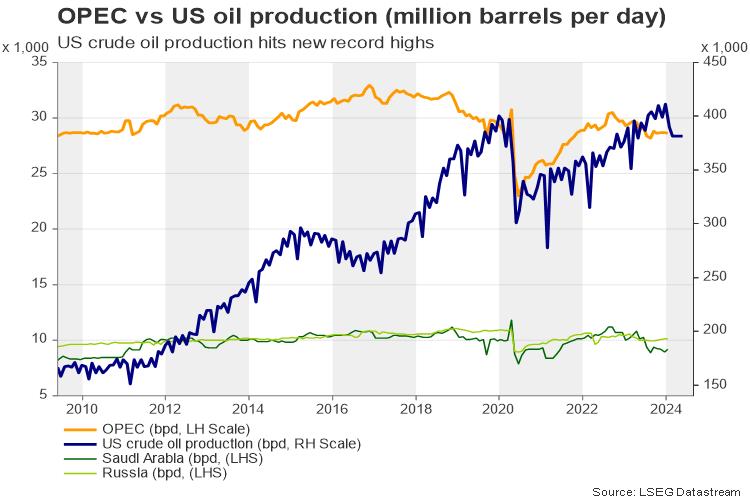

Perhaps other important OPEC producers such as Iran and Iraq might not complain either and could even accept a new round of cuts as their breakeven price is even higher, though the expansion in their supply capacity suggests that persisting production cuts might not be in their interest as US supply is expected to hit a record high in 2025. Canada, Brazil and Norway could also lead production increases in the months ahead.

Would OPEC+ members welcome a reversal in cuts?

Alternatively, softer production cuts could send oil prices lower, benefiting only a minor group of exporters, including Libya and the UAE. The latter faces an estimated break-even price of around $56.7 in 2024 and aims to increase its capacity further by 2027. Yet, capacity assessments will not be delivered before the meeting and an increase in production could be a tough task this week. Perhaps, such a decision could be easier next year. OPEC estimates a demand slowdown to 1.8 million bpd in 2025 from 2.2 million bpd in 2024. The IEA foresees a steeper decline to 1.1 million bpd estimated by the IEA. Hence, production might be more balanced next year and after the US election.

For now, OPEC’s supply cut policy combined with the ongoing geopolitical risks in Ukraine and Israel keeps adding a floor under crude oil prices. The summer travel season ahead and a more optimistic outlook about China’s recovery could boost demand for fuel, while more clarity on when the Fed will start cutting rates could be a positive catalyst for oil investments too.

WTI crude oil

Technically, WTI oil futures will need to close above the broken support trendline at $81.37 to extend their upturn towards the 23.6% Fibonacci retracement of the previous uptrend at $82.40. Even higher, the focus might fall on the constraining zone of $83.90-$84.35, where the ascending line from the pandemic low and the tentative resistance line from the 2022 top are located. A successful penetration of this border could cause an acceleration towards April’s ceiling of $86.80.

In the event the OPEC+ group signals a softer supply cut approach in 2025, WTI crude could drift lower. The flattening 200-day simple moving average is nearby and attached to the 38.2% Fibonacci mark of $79.65. Therefore, any steps lower and below the 50-day SMA at $78.92 could see a continuation towards the 50% Fibonacci of $77.42. An extension below May’s base of $76.00 would worsen the outlook.