{kind=link}

Markets

As US and UK markets were closed yesterday, directional guidance for trading on European markets solely had to come from domestic sources. German IFO Business climate printed softer than hoped for after last week’s strong PMIs. The overall index stabilized (89.3) as better expectations were neutralized by an, albeit modest, setback in the current assessment. The immediate impact on EMU bond markets was negligible, but yields finally fell prey to the forces of gravity and this move was reinforced by comments from ECB’s Villeroy and Lane. As the ECB is in a data-dependent and meeting-by-meeting approach, the Bank of France governor wants to keep all options open. A June rate cut is a done deal except in case of a big shock. After that, Villeroy didn’t commit to any specific path for follow-up easing, but contrary to some of his more hawkish colleagues he doesn’t exclude a next step in July. If expectations for inflation returning to 2% next year are confirmed, there is room for the ECB to already reduce restrictive policy this year. Villeroy also labelled current market expectations on the ECB’s terminal rate (2.50%/2.75% area) as not unreasonable. In a separate interview, Chief economist Lane agreed, that within restrictiveness, there is room to lower rates. German yields declined between 4.7 bps (2-y) and 2.2 bps (30-y). Even after the comments markets still are about 50-50% split on two or three 25 bps ECB rate cuts by the end of the year. In low volume trading, European equities remained well bid (EuroStoxx 50 + 0.47%). The euro briefly reversed initial losses to close the day even marginally stronger at 1.0859. Sterling outperformed with EUR/GBP testing the 0.85 barrier.

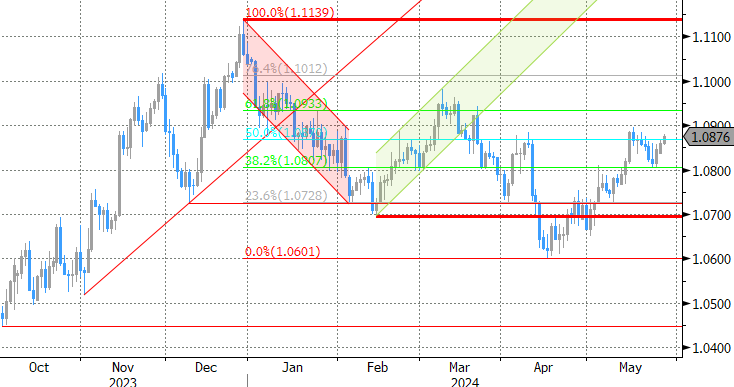

This morning, Asian equities are trading mixed, mostly with no big changes. US yields decline marginally and the dollar stays in the defensive (DXY 104.44; EUR/USD 1.0875). Later today, the calendar in the EMU and the US is modestly interesting with markets still focused on key inflation data later this week (EMU May flash CPI and US April PCE deflators on Friday). In EMU, the ECB 1-year inflation expectation is expected to ease for 3.0% to 2.9% (3-y expected unchanged at 2.5%). After yesterday’s comments from ECB’s Villeroy and Lane, a soft surprise might cause markets to again move in the direction of 3 rather than 2 ECB rate cuts this year, supporting some further decline especially at the short end of EMU yield curves. In the US, house prices and consumer confidence (Conference Board) will be released. The overall index is expected to continue the gradual downtrend (96 from 97) since the start of the year. Such an outcome, might help cap last week’s rebound in US yields, keep equities well bid and weigh on the dollar. In a day-to-day perspective, the US currency might return to ST support levels (DXY 104.08 and EUR/USD 1.0895). Softer UK price data (cf infra), this morning are keeping EUR/GBP north of 0.85.

News & Views

US yields decline marginally and the As US and U British retail shop price rises eased to 0.6% y/y in May, the slowest pace since end 2021, the British Retail Consortium reported this morning. That’s slower than the 0.8% the month before and defies expectations for a pickup to 1%. The decline was broad-based with food prices rising 3.2% compared to 3.4% in April. Non-food was even increasingly deflationary for a second month straight (-0.8%, from -0.6%). The BRC chief executive noted that “Retailers cut furniture prices in an attempt to revive subdued consumer demand for big-ticket items, and football fans have been able to grab some bargains on TVs and other audio-visual equipment.” The price data come after the UK last week released April CPI numbers that topped estimates across the board. UK money markets have all but fully priced out a June rate cut by the Bank of England as a result.

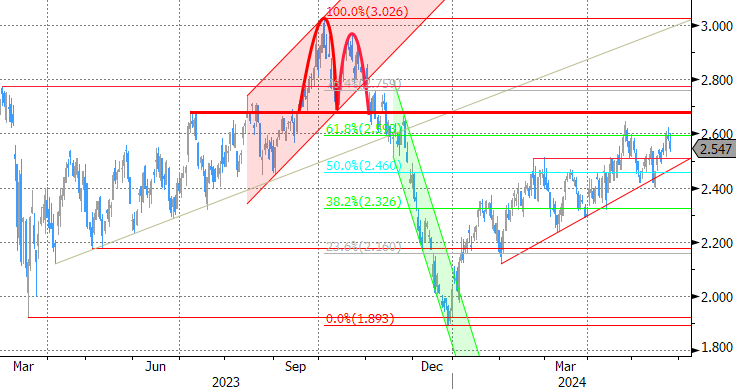

Australian retail sales in April rose a meagre 0.1% m/m, erasing only part of the 0.4% decline the month before. The head of Australia’s statistics bureau noted that the timing of easter and school holidays across the country induced some volatility in turnover in March and April. But this doesn’t change the fact that “Since the start of 2024, trend retail turnover has been flat as cautious consumers reduce their discretionary spending.” Turnover in most non-food industries rose with the exception of clothing, footwear and personal accessory retailing. Food-related spending was mixed with food retailing (-0.5%) normalizing after an early Easter-boosted March while there was a small rise in cafes, restaurants and takeaway. The Australian dollar strengthens this morning despite the poor reading against an overall weak USD. AUD/USD trades around 0.666.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target.. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell indicated that further tightening was unlikely. Soft US early month data triggering a correction off YTD peak levels. However, the Fed minutes still showed internal debate whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already proved strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view but slower than expected April disinflation and a surprise general election on July 4 complicated matters. A June cut in line with the ECB looks improbable. Sterling extends a recent bull rally. A test of EUR/GBP’s 2024 YtD low (0.8489) is possible. We expect this important support level to hold.