{kind=link}

Summary

- As was widely expected, the FOMC left the fed funds target range unchanged at 5.25-5.50% at the conclusion of its March meeting.

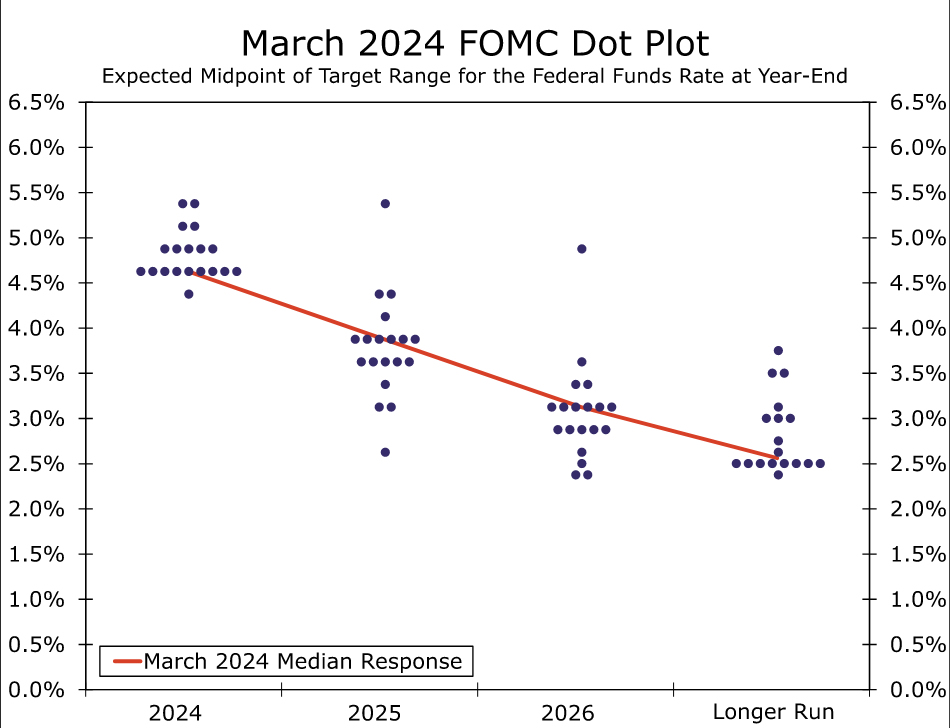

- The Summary of Economic Projections showed that the vast majority of the Committee continues to believe some easing of policy will be appropriate this year. The median projection for the federal funds rate at year-end was unchanged from December’s projection at 4.625%. However, the distribution of expectations shifted higher for 2024 and the median dot for 2025 and 2026 moved up 25 bps, implying an incrementally more hawkish outlook.

- Notably, the median “longer-run” dot also moved higher. While the increase was small (6 bps), we suspect the longer-run dot will drift higher very slowly to reflect a neutral rate that may have moved somewhat higher relative to the pre-pandemic period.

- The slightly higher fed funds rate outlook comes amid more upbeat projections for economic growth and stickier inflation this year. That said, the Committee’s estimates for unemployment and inflation were barely changed for 2025-2026.

- The statement was virtually unchanged, with only a minor tweak to the paragraph on recent economic conditions. The Committee continues to seek “greater confidence that inflation is moving sustainably toward 2%” before reducing the fed funds rate.

- Overall, the updated Summary of Economic Projections suggests that the FOMC believes that inflation is on a path back to its 2% target, but it is likely to be achieved slightly later than previously expected. We continue to look for the FOMC to start reducing the fed funds rate at its June 12 meeting. However, the risks to our outlook are skewed toward the FOMC beginning to ease a little later in the summer or potentially proceeding at a slower pace that leads to less than the 100 bps of easing we project through the end of this year.

- While risks to the FOMC beginning to cut the fed funds rate skew toward later in the year, balance sheet normalization looks likely to occur somewhat earlier. In light of Powell’s comments at today’s press conference, we think an announcement to slow the pace of quantitative tightening is coming at the May 1 meeting, although we would not be surprised if it slipped to the following meeting on June 12.

FOMC Signals Cuts Coming, Just Not Yet

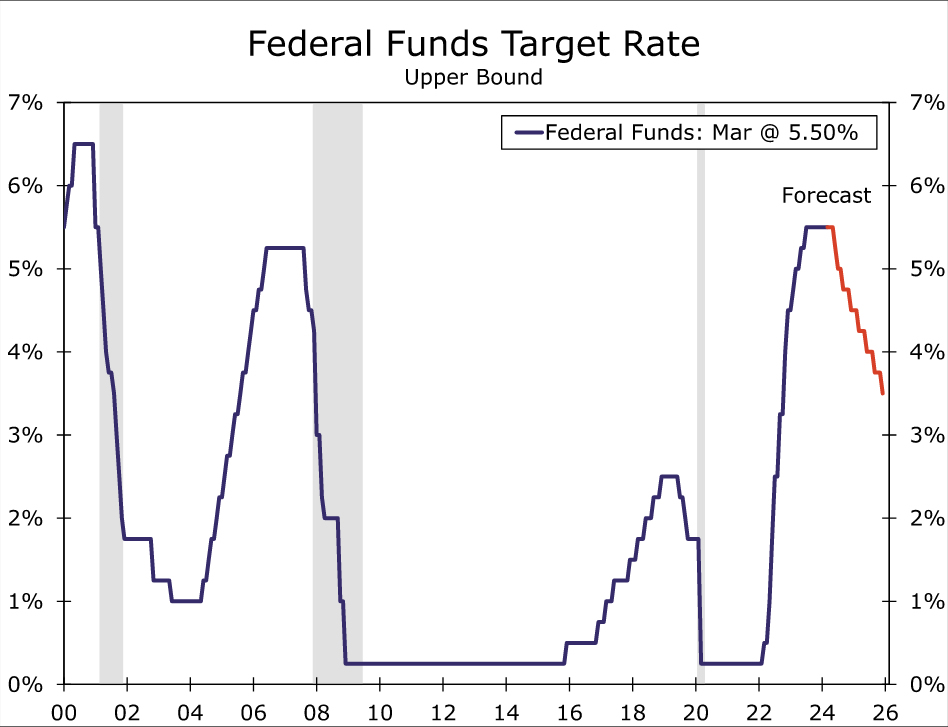

As widely expected, the FOMC left the target range for the federal funds rate unchanged at 5.25-5.50% at the conclusion of its March meeting. The last rate hike occurred in July 2023, and the Committee has left its policy rate unchanged in the eight months since.

The Summary of Economic Projections (SEP) signaled that all but two of the Committee members expect to start cutting rates this year, with the median participant projecting 75 bps of easing by year-end 2024 (chart). The 2024 median dot was unchanged from the December SEP, although the distribution drifted higher in a sign that policymakers remain on guard against sticky inflation. In that vein, the median dots for 2025 and 2026 rose by 25 bps in each year, consistent with 75 bps of easing in 2025 and another 75 bps of cuts in 2026.

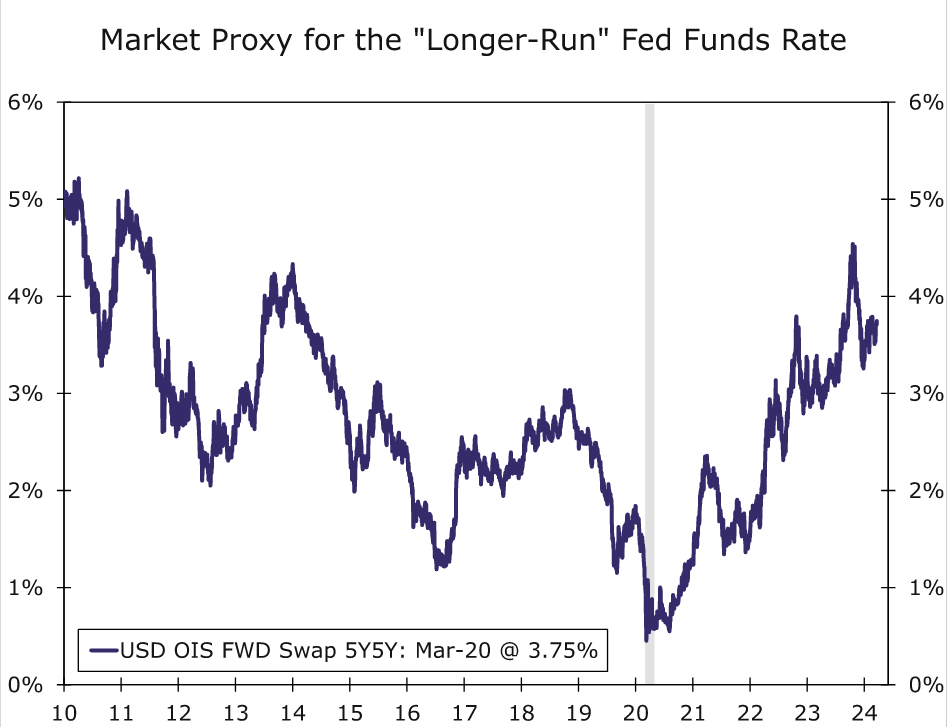

The median “longer-run” dot also moved higher. The longer-run dot represents each participant’s view of the level of the federal funds rate that would be most consistent with achieving the Federal Reserve’s dual mandate of maximum employment and price stability over the long-run. The increase in the longer-run dot was small, just 6 bps, but it marks the first time the median has been above 2.5% since March 2019. We suspect the longer-run dot will drift higher very slowly to reflect a neutral rate that may have moved somewhat higher relative to the pre-pandemic period. Markets appear to be ahead of the Committee and are priced for short-term interest rates to be between three and four percent over the longer-run (chart).

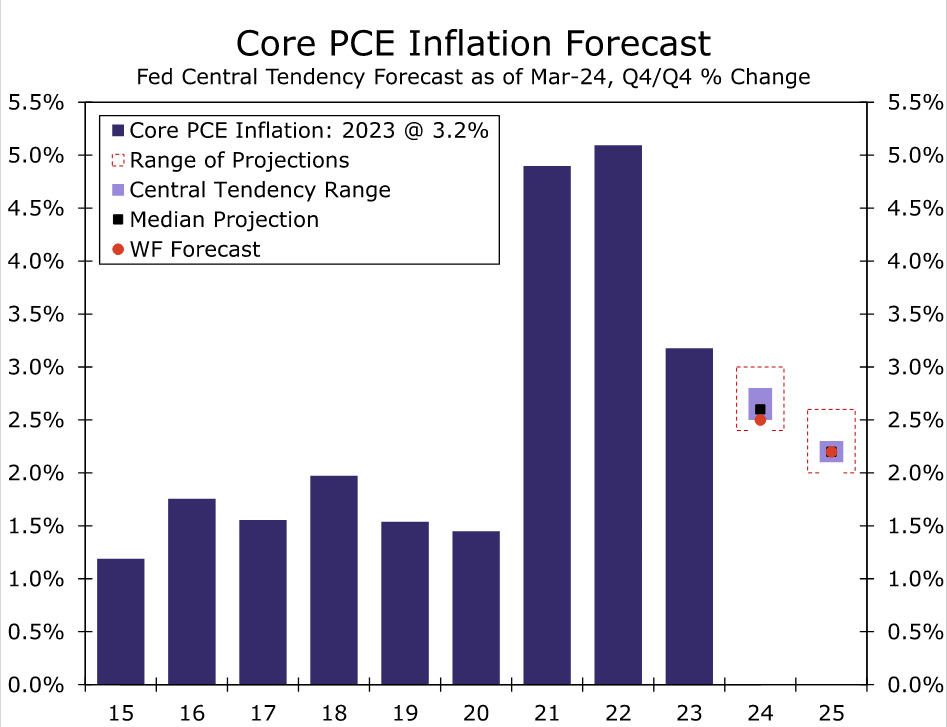

Elsewhere, the Committee’s projections for the economy reflected continued resilience in both output and price growth. The median projection for real GDP growth in 2024 is 2.1%—up from 1.4% in the December SEP. Growth projections in 2025 and 2026 were also revised up by two tenths and one tenth of a percentage point, respectively. The Committee’s inflation projections also rose modestly, most notably an increase in the median projection for 2024 core PCE inflation from 2.4% to 2.6% (chart). That said, the median forecasts for core inflation in 2025 and 2026 were left unchanged in a sign that the Committee remains confident that inflation progress will continue, just at a slightly slower pace than previously believed.

The post-meeting statement contained virtually no changes to what was released following the January 31 meeting. Job gains were still characterized as “strong,” although the phrase that hiring has “moderated since early last year” was stricken with payrolls averaging 265K the past three months. The remainder of the statement contained no changes. Economic activity continues to expand at a “solid” pace, and inflation “remains elevated.” Notably, the FOMC continues to seek “greater confidence that inflation is moving sustainably toward 2%” before reducing the fed funds rate.

Source: U.S. Department of Commerce, Federal Reserve Board and Wells Fargo Economics

Source: Federal Reserve Board and Wells Fargo Economics

Overall, the updated Summary of Economic Projections suggests that the FOMC believes that inflation is on a path back to its 2% target, but it is likely to be achieved slightly later than previously expected. We currently expect the Committee to first ease policy at its June 12 meeting, at which time officials will have seen three more months of inflation and employment data, and ultimately reduce the fed funds rate by a total of 100 bps this year (chart). However, with the Committee more upbeat on prospects for economic activity and a bit more worried about inflation, the risks to our outlook are skewed toward the FOMC beginning to ease a little later in the summer (at its July 31 meeting), or potentially proceeding at a slower pace (e.g., every other meeting).

The Committee also reaffirmed its ongoing pace of balance sheet runoff, commonly referred to as quantitative tightening (QT), but Chair Powell’s comments in the post-meeting press conference suggested that changes are coming. Powell stated that it is the Committee’s view that it would be appropriate to slow the pace of asset runoff “fairly soon.” Note that a slower pace of QT would still involve shrinking the Fed’s balance sheet, just at a slower pace than what has occurred since QT ramped up in mid-2022. Coming into the meeting, our forecast assumed that the FOMC would announce a plan to slow the pace of QT at its June meeting. In light of Powell’s comments today, an announcement at the May meeting seems slightly more likely than a June announcement, although we would not be surprised if it slipped to the June meeting. Either way, we expect the runoff caps for Treasury securities to be reduced to $30 billion while mortgage-backed securities caps are dropped to $20 billion, with this slower pace of runoff continuing until roughly year-end 2024.