emulated the Federal Reserve by exploring rate cuts, ultimately deciding to maintain interest rates at 5.25%, their highest level in 16 years, with a 6-3 majority vote. Two policymakers voted for a rate hike but surprisingly, one policymaker raised his hand for a quarter-percentage point rate cut for the first time since the pandemic. On top of this, the central bank removed the sentence that referred to further tightening, adding to speculation that the rate hike cycle was now in the past and a new chapter of rate cuts would open in the coming months.){kind=link}

- Bank of England to retain the same policy stance

- Q2 data could be more valuable for next decision making

What happened last time

In its February policy meeting, the Bank of England (BoE) emulated the Federal Reserve by exploring rate cuts, ultimately deciding to maintain interest rates at 5.25%, their highest level in 16 years, with a 6-3 majority vote. Two policymakers voted for a rate hike but surprisingly, one policymaker raised his hand for a quarter-percentage point rate cut for the first time since the pandemic. On top of this, the central bank removed the sentence that referred to further tightening, adding to speculation that the rate hike cycle was now in the past and a new chapter of rate cuts would open in the coming months.

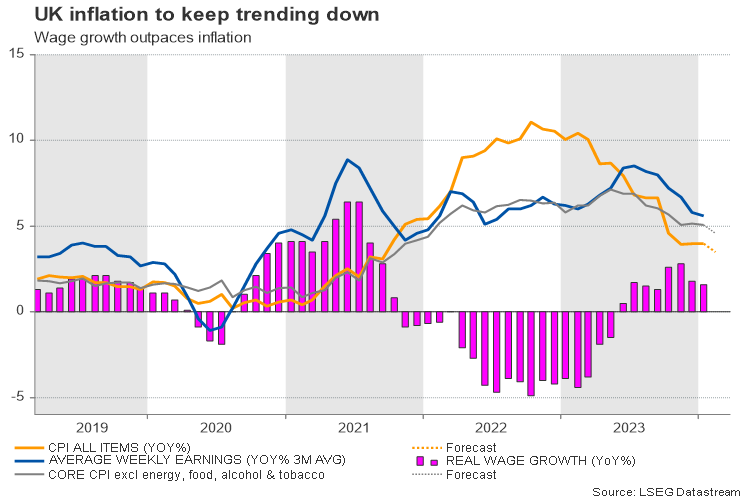

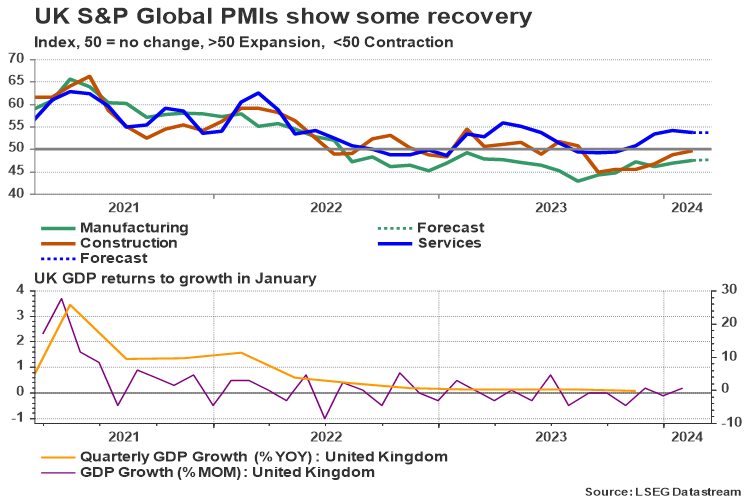

However, the central bank provided no clues about the timing of rate cuts, reiterating in the policy statement that more evidence is needed to confirm inflation is moving sustainably towards its 2.0% target. This narrative might be repeated once again when the central bank reviews its policy on Thursday. UK inflation stabilized at 4.0% y/y in January but given the recent upside surprises in the eurozone and the US CPI data, a meaningful pullback to 3.5% as analysts expect, is questionable. Besides, with the economy moving out of a mild technical recession in January on the back of growing consumption and construction, policymakers might avoid any premature rate cut signals.

Inflation expectations

Inflation expectations

The BoE economic forecasts predict a temporary slide in inflation to the 2.0% target in Q2 of this year, followed by a subsequent increase before gradually falling below that level in three years. Chancellor Jeremy Hunt did not reignite new inflation concerns nor did he spark concerns about high debt when he introduced his spring budget earlier this month. Hence, the central bank might feel more confident sticking to its current policy, especially as the continuous slowdown in wage growth keeps denting fears of a wage-price spiral.

Interestingly, BoE governor Andrew Bailey admitted that interest rates might go down before inflation reaches the central bank’s goal. Perhaps he wanted to emphasize that sustained progress on services’ costs, wage growth and labor shortages might be enough information to proceed with rate cuts. In the meantime, though, there is no guarantee that the economy will meet these conditions soon given that wage growth is still well above the inflation rate and higher than 4% observed in the US and eurozone. Upcoming wage increases in April will be closely watched for that reason, while potential spikes in raw material costs and energy prices cannot be ruled out either, given the persisting geopolitical risks in Ukraine and the Middle East.

Will the central bank call for a June rate cut?

Therefore, the rate statement might give little reason for investors to bring forward their rate cut projections from August to June. Also, if one more hawk migrates to the group of unchanged rates, shifting the voting structure to 7-2 as analysts project, that would be another indication that rate cuts are coming instead of a preference for an earlier rate reduction.

Futures markets are currently reflecting a less than 50% probability of a quarter-percentage rate cut in June and around 70% chance for a similar move in August. Perhaps investors could adjust their rate projections if inflation readings fall short of analysts’ estimates, but that would still be in line with the BoE’s forecast for a significant inflation slowdown this year. Moreover, an unexpected pullback in the flash business PMI figures due on Thursday could justify the central bank’s muted GDP growth forecast for Q1, whilst stronger-than-expected readings might question the need for a rate cut.

Thus, unless the BoE tweaks its language to support a dovish change in June, the pound could strengthen as markets would delay the possibility of rate cuts. Perhaps the second quarter data could be more vital for decision making and hence a bigger source of volatility.

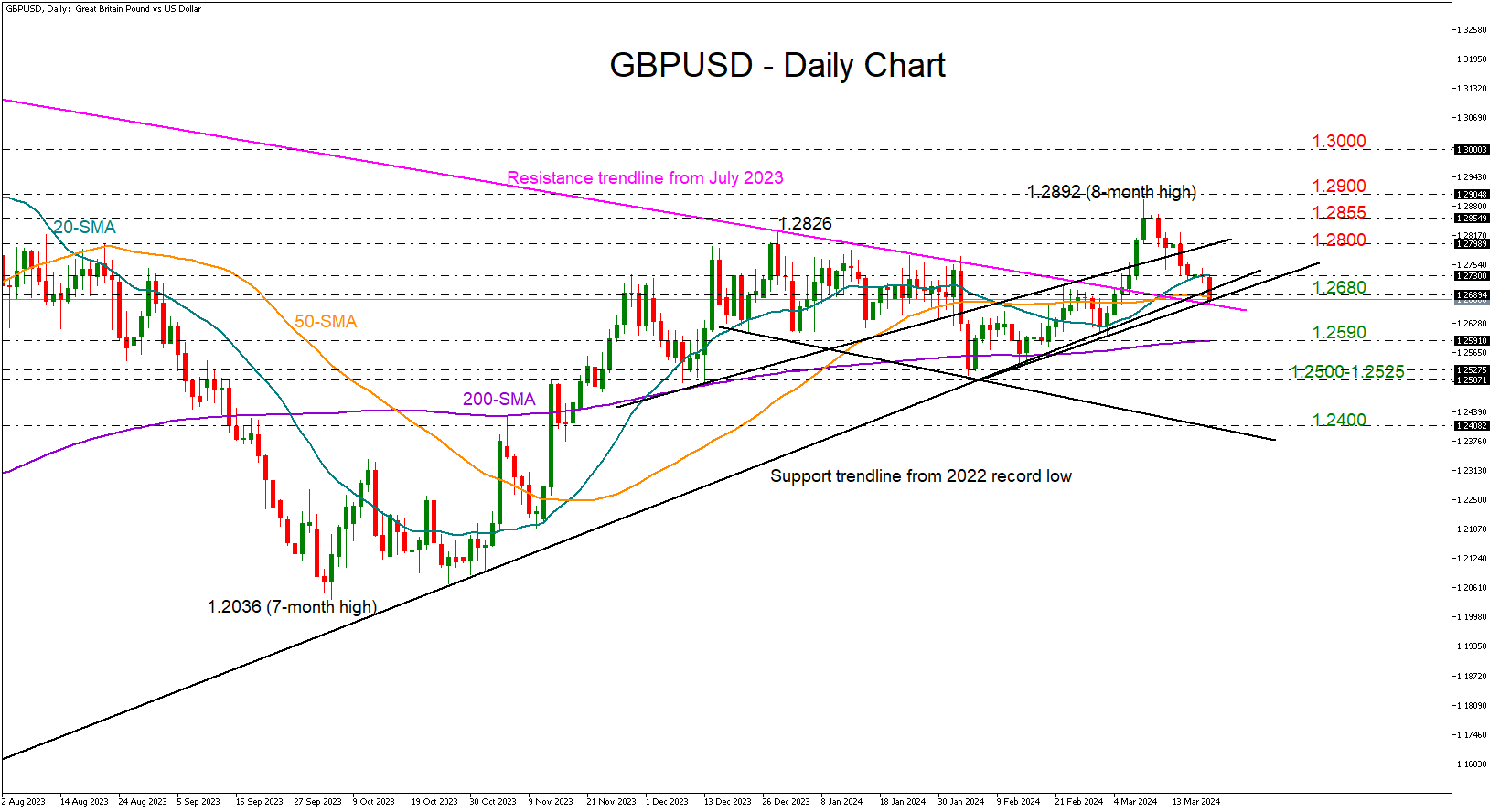

GBP/USD levels to watch

At present, GBPUSD is seeking support around the 1.2680 region following its pullback from an eight-month high of 1.2892. A close below that floor would downgrade the short-term outlook back to neutral, consequently causing a slump towards its 200-day simple moving average (SMA) at 1.2590.

On the upside, the bulls will have to crawl back above the 20-day SMA at 1.2730 in order to reach the 1.2800 round level. A move higher and above the 1.2855-1.2900 wall could see an advance towards the 1.3000 psychological level.