{kind=link}

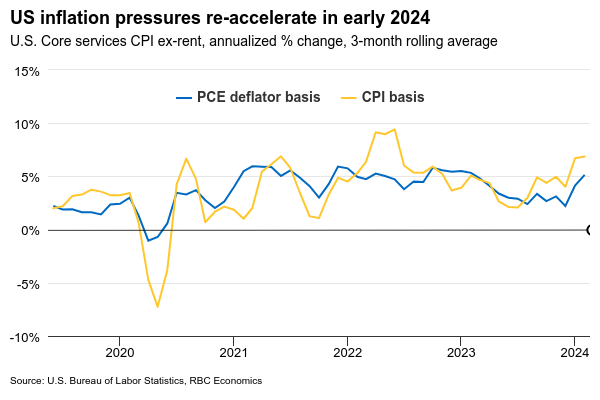

The U.S. Federal Reserve is widely expected to stand pat on the fed funds range for a fifth consecutive meeting on Wednesday. But any shift in the monetary policy statement language will be closely watched after two straight months of upside surprises on inflation.

Markets continue to expect the first interest rate cut in June in line with our expectations. But we now anticipate the Fed will be moving at a slower pace and cut rates by 75 basis points (instead of the 125 bps previously expected) this year to 4.5-4.75%, given the above-target price increases and strong growth in output and employment. Its accompanying Summary of Economic Projections will be reviewed for any changes in the expected number of rate cuts this year, and potential revisions to GDP growth, unemployment rate and inflation forecasts.

Recent comments from Fed officials have suggested they’re still committed to moving rates lower this year despite the setback in inflation. That, however, is contingent upon inflation readings easing in the months ahead. There are still three more consumer price index releases before the Fed’s June meeting. Headline inflation should follow market rent measures lower by then.

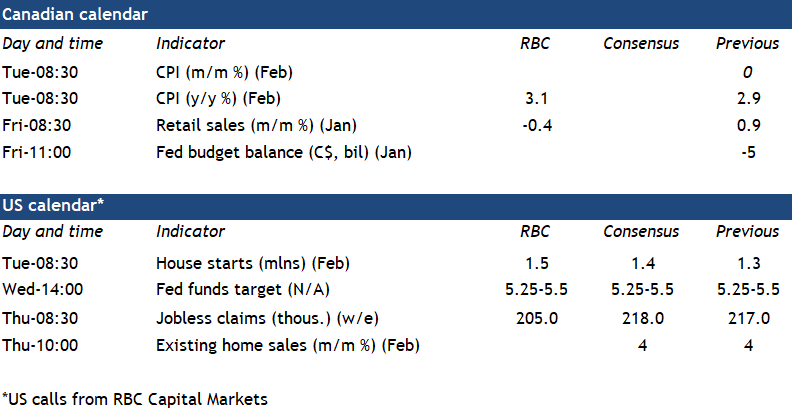

Similarly, Canada’s February CPI print on Tuesday will be watched by the Bank of Canada for more signs of improvement in price pressures. Both headline and core (ex-food and energy) inflation are expected to come in at 3.1% year-over-year with headline up from 2.9% in January on higher energy inflation. Gasoline prices rose by nearly 4% in February from a month ago. Still, a very soft economic backdrop means that price pressures in Canada are more likely to keep easing and narrowing, allowing for a first rate cut from the BoC to also come in June.

Week ahead data watch

Retail sales in Canada are expected to edge lower in January by 0.4% (nominal), consistent with Statistics Canada’s preliminary call. Gasoline prices were lower in January, but the volume is also expected to have dropped by 0.3% due to lower auto sales.