{kind=link}

- Fed meets on Wednesday with focus on new dot plot

- Will the Bank of Japan finally end negative rates on Tuesday?

- BoE and RBA to stick with patience, SNB might be in more of a rush to cut

- Flash PMIs plus inflation data in the UK, Japan and Canada will also be crucial

Fed decision: hoping for the best

The upcoming week will undoubtedly be one of the busiest, not to mention the most important, of the year for investors with five major central bank decisions on the way, along with a plethora of economic data. The highlight, however, looks set to be the Federal Reserve’s decision on Wednesday, as expectations of looser monetary policy in the world’s largest economy have been fuelling the incredible stock market rally of late.

Rate cut bets have swung sharply this year amid some mixed signals on the strength of the Fed’s two mandates: employment and price stability. If the overall picture could be summed up, it is that both the labour market and inflation are cooling down, but only gradually. The latest nonfarm payrolls report and CPI figures only underscored this trend.

For the Fed, although it has so far avoided the trap of pre-committing to a rate cut, the easing tendency is evident. Chair Powell told lawmakers last week that they’re “not far” from being confident that inflation is moving sustainably towards 2%. Powell’s readiness to cut is likely the reason why markets react more to soft data than upbeat ones.

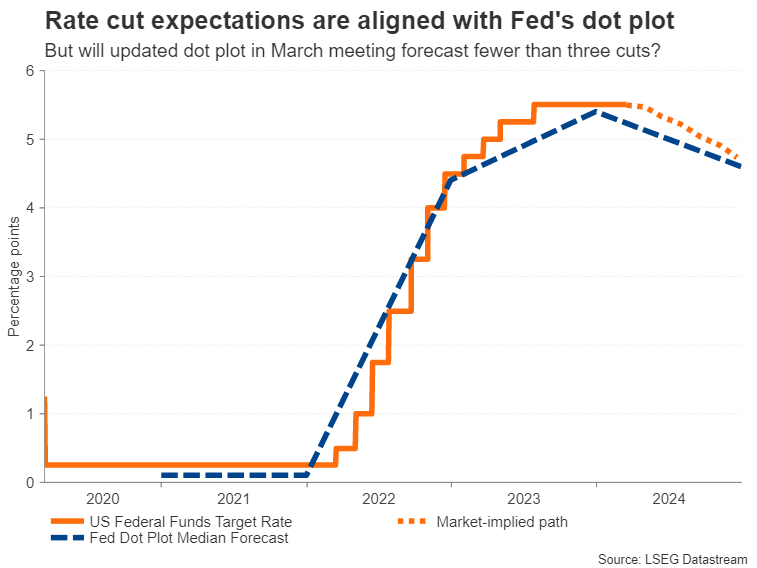

However, the Fed’s projected rate cuts are based on the expectation that inflation remains in a downward trajectory despite the slowdown in the disinflation process. That trend has now started to look questionable as the latest CPI and PPI releases suggest that inflation may be flatlining before reaching the Fed’s 2% goal. This turns the spotlight on the updated FOMC dot plot, which will be the focal point of the March meeting.

There’s a possibility the median projection for 2024 will be revised from three 25-basis-point rate cuts to just two. But even if the median projection is left unrevised, if more participants see the Fed funds rate either at 4.75% or higher, that would also reflect a hawkish tilt. Yet, Powell might still attempt to strike a balanced tone in his press briefing in the event that FOMC members predict only two rate cuts, and this could limit any selloffs in stocks and other risk assets.

For the US dollar, however, the upside risks are greater than the downside risks heading into the meeting following its somewhat muted response to the recent hot price data. Traders will additionally be keeping an eye on some housing stats (building permits and housing starts on Tuesday, and existing home sales on Friday), the Philly Fed manufacturing gauge on Thursday as well as S&P Global’s flash PMI readings for March.

BoJ: time to hike?

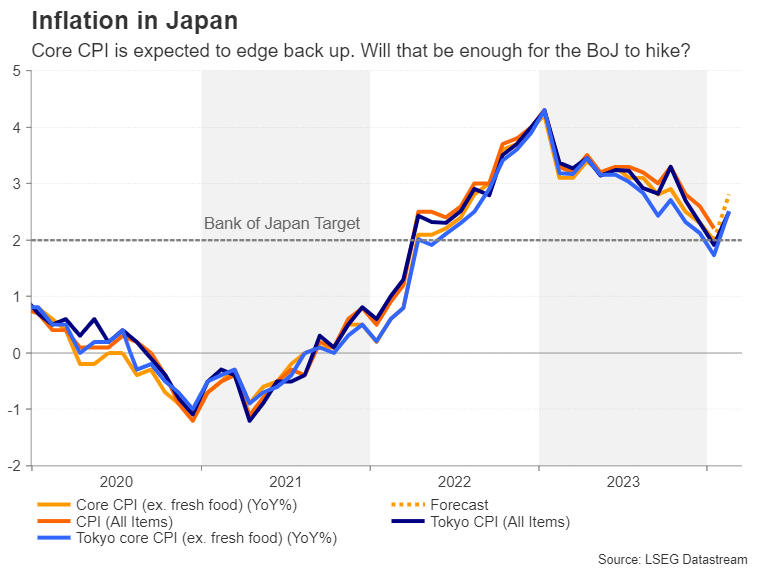

The long-suffering yen enjoyed a much-needed lift in March amid renewed speculation that the Bank of Japan is close to ending its negative rates policy. Early indications from the spring wage negotiations point to much bigger pay deals this year than in 2023. Governor Ueda couldn’t have made it clearer that any exit from negative rates is conditional on a sustained acceleration in wage growth.

Some board members already see this criteria being met so may vote for a rate increase at Tuesday’s policy decision. However, having been patient this long, it’s unlikely that Ueda will support such a move before there’s a more complete picture about the outcome of the 2024 wage negotiations, and so April remains a more realistic timeframe for a big policy shift.

Traders seem to concur as they’ve priced in a 40% probability for a 10-bps hike in March and a 70% probability for April.

Another reason why the BoJ may prefer to wait is that the consumer price index for February is released days later on Friday. Although the annual CPI rate in Tokyo spiked higher in February, suggesting a similar move in the nationwide figures, the Bank may not want to jump the gun.

For the yen, however, the March meeting could still spur some significant gains even if no rate hike is announced. Policymakers will likely make significant tweaks to the language to possibly hint that they are close to achieving 2% inflation sustainably. They may even announce some changes to their asset purchases by ending the program for buying exchange-traded funds.

Hence, the yen could attract buyers until the April meeting. What happens after that, though, will depend on whether the BoJ will also abandon its yield curve control policy and whether a rate hike will be a one-off.

Aside from the CPI numbers, machinery orders will be watched in Japan on Monday, as well as the flash PMIs on Thursday.

UK CPI data might overshadow BoE meeting

The pound is the only major currency that is currently able to stand tall against the US dollar in terms of year-to-date performance. Much of that is to do with the expectation that the Bank of England will not be able to cut rates before August, whereas the Fed and the European Central Bank will likely cut in June. More to the point, the latest market pricing puts UK interest rates the highest in the G7 by year end, amid stickier inflation and wage pressures than in other economies.

Unsurprisingly, Bank of England officials have been less dovish than their global counterparts when it comes to rate cut talk, although they have hinted that policy might need to become less restrictive later in the year. Fortunately for the Monetary Policy Committee, there’s a raft of incoming UK data next week that should help members make up their minds.

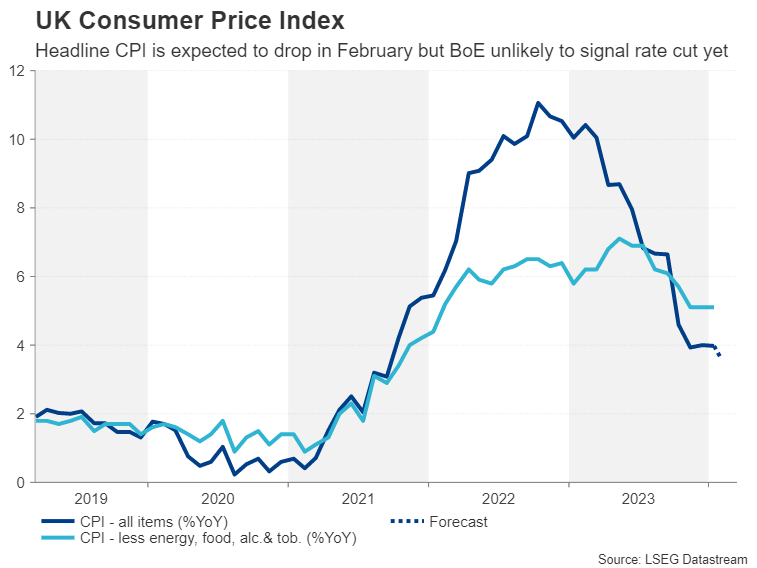

The CPI report for February is due on Wednesday, the flash PMIs will follow on Thursday, and retail sales will wrap up the week on Friday. The inflation numbers will come just in time before the MPC votes later on Wednesday.

Both headline and core CPI were unchanged in January so policymakers will be hoping to see inflation head back down again in February. Another disappointment in CPI staying sticky, combined with a not-so-gloomy PMI survey would probably prompt the BoE to maintain its comparatively hawkish stance, boosting the pound.

However, any downside surprises in the CPI figures, especially on the back of the somewhat weaker-than-expected employment report could trigger a bit of correction in cable following its near 2% rally at the start of March.

As for Thursday’s decision, there is no press briefing nor new forecasts at the March meeting, so investors will be looking for subtle changes to the statement.

SNB might lay groundwork for a cut

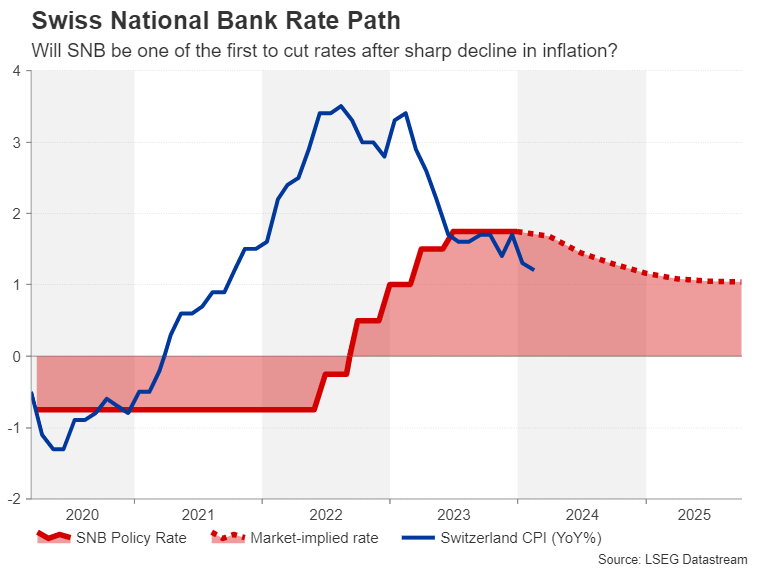

The Swiss National Bank also meets on Thursday, and it too is not expected to announce any changes in borrowing costs. The Alpine nation boasts an inflation rate of just 1.2% so out of all the central banks, the SNB has the most reason to begin slashing rates imminently.

A 25-basis-point rate cut is more than fully priced in for June and this might explain why the Swiss franc is close to overtaking the yen as the worst performing currency this year. If policymakers signal that a rate cut is likely at the June meeting, the franc could extend its losses.

RBA: from a hawkish hold to a dovish hold

Kicking things off, however, is the Reserve Bank of Australia, which meets on Tuesday. The RBA has been on hold after last hiking rates back in November. Policymakers considered hiking again at both of their subsequent meetings but decided against it. At the March meeting, the decision will likely be less contentious as there’s been some further progress in bringing down inflation since the last gathering, particularly in the underlying measures.

But would that be enough for the RBA to drop its tightening bias? There’s been a notable hawkish shift in RBA policy under Governor Michelle Bullock, but in her last comments when she testified in Parliament in February, she sounded slightly more optimistic about inflation coming down. A more neutral tone on Tuesday is therefore probable and this may weigh on the local dollar.

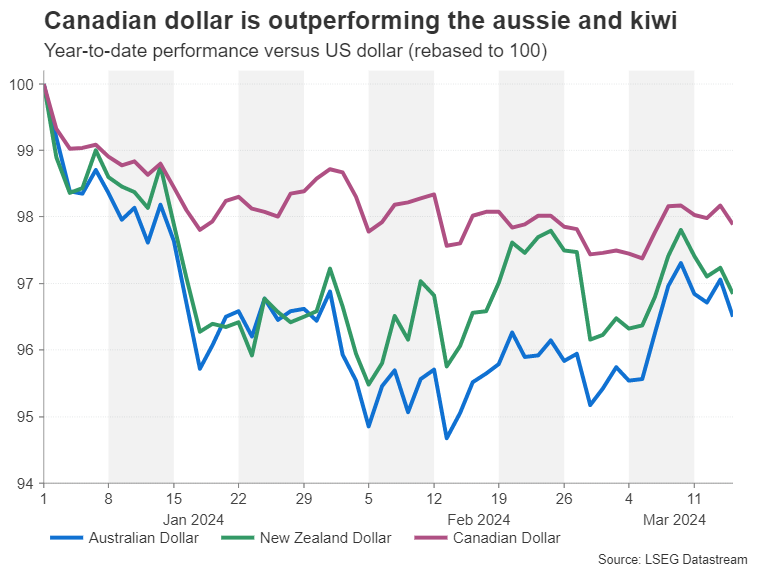

Plenty of drivers for the commodity dollars

The aussie has shed more than 3.5% so far in 2024 despite investors expecting fewer cuts by the RBA this year than other major central banks. Worries about Australia’s biggest trading partner – China – are partly to blame for this underperformance.

Aussie traders will be monitoring industrial output and retail sales numbers due in China on Monday for fresh clues on the speed of the Chinese recovery, while domestic employment figures on Thursday will also be vital.

Staying in the region, New Zealand will publish quarterly GDP estimates on Thursday, which may boost the kiwi if they show the economy returned to growth in the final quarter of 2023.

The Canadian dollar has fared somewhat better than the other commodity linked currencies, as like in the US, inflation in Canada is taking longer than anticipated to reach the 2% target. Investors have pushed out the timing of when they expect the Bank of Canada to start cutting rates, with a move not seen before the July meeting, followed by just one more cut after that.

However, headline CPI did fall back below 3.0% in January and a further decline in February might lead to rate cut bets being ratcheted up. The latest CPI release is on Tuesday, with retail sales for January coming up on Friday.

Euro eyes PMI bounce for further gains

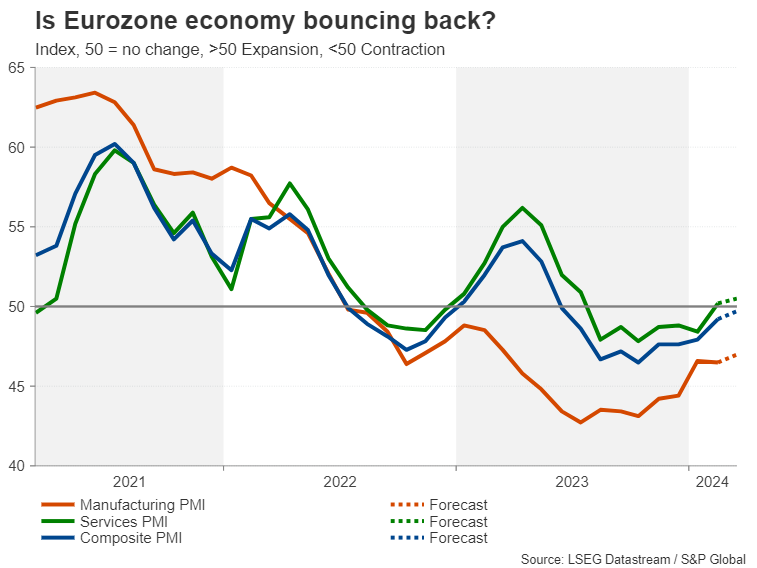

Finally, the euro will not miss out on some attention as Thursday’s flash PMI estimates for the Eurozone could sway ECB rate cut bets. A battle is raging between the hawks and doves as to not only how soon the central bank should switch to an easing cycle, but by how much rates should be cut.

With inflationary pressures fading fast and an economy stuck in the doldrums, the ECB could yet be more aggressive than the Fed in slashing rates. However, whilst the inflation picture remains encouraging, there are signs that economic growth has started to regain some momentum. The services PMI climbed above the 50 neutral mark in February for the first time since July and is expected to improve further in March. The manufacturing sector remains in contractionary territory but there are green shoots there too.

After flirting with the $1.09 level during the past week, the euro could rise further if the PMIs impress. Ahead of the PMI survey, the final CPI readings are due on Monday, while German business gauges, the ZEW and Ifo indices on Tuesday and Friday, respectively, will shed some more light on the bloc’s largest but currently the weakest economy.