.){kind=link}

The spring wage decision will reflect cyclical factors rather than a structural shift leaving little reason for the BoJ to consider contractionary action.

The Bank of Japan and financial markets are eagerly awaiting the Shunto wage decision for Japan’s largest trade confederation RENGO, which is due in. In our view, the result will likely be more of a reflection of near-term cyclicality than structural strength in the economy. It is therefore unlikely to justify a material policy shift by the Bank of Japan (BoJ).

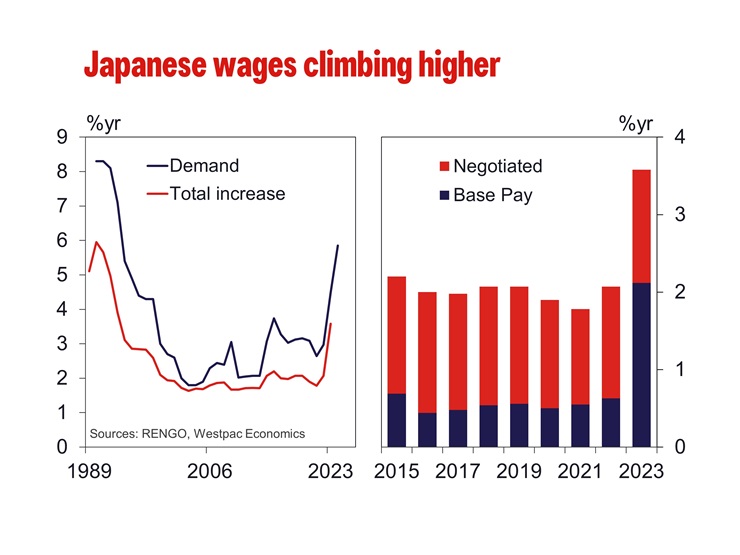

Japan’s recent strong wage growth reflects the lagged effect of cyclical momentum in the economy. RENGO wages rose 3.6% in 2023 after averaging 2% between 2014 and 2022. Base pay, which goes to all employees, rose 2% trumping the average 0.6% rise since 2015. In justifying their decision, RENGO drew attention to higher cost of living. Inflation rose 4% through 2022, well above the 0.5%yr average between 2010 and 2019. Inflation subsequently eased to 2.6%yr during 2023, following the global disinflationary pulse, and is expected to ease further hence.

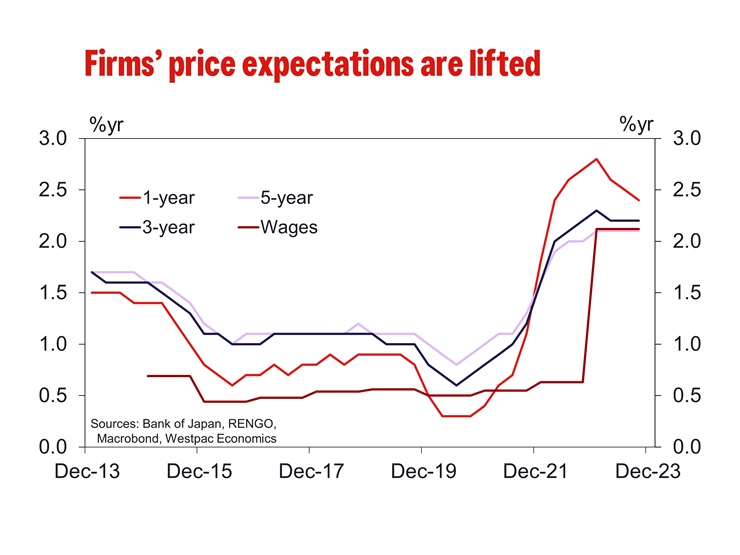

As of 2023 Q4, the inflation outlook for 1, 3 and 5 years came to 2.4%, 2.2% and 2.1% respectively. While still above the circa 1% average for all three time periods 2014 to 2019, it is also materially below where inflation has been. Still-elevated current inflation expectations may support wage growth in the near-term, but this effect looks set to dissipate as actual inflation prints come in weaker.

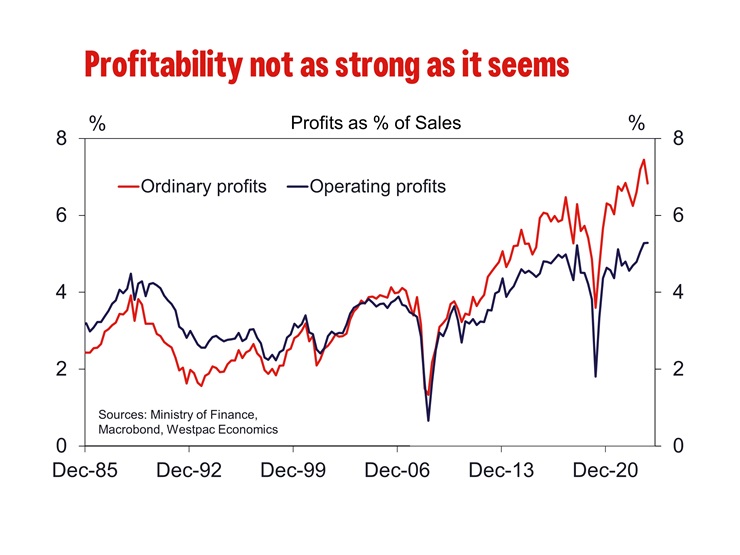

Rising profitability has also been used to argue for stronger wage growth in 2024 with a focus on strength in ordinary profits. However, operating profits are only slightly above the pre-COVID peak and below the 10-year pre-COVID trend. Operating profit as a share of sales are also relatively unimpressive, hovering around pre-COVID rates. The disparity between operating profits, which do not include investment-related income, and ordinary profits implies profitability is being flattered by financial investment returns not firms’ underlying profitability. It is only the latter that would given businesses confidence to increase wages at or above the rate of inflation.

Rather than being a support for wage growth, beyond 2024, we expect structural factors to act at a headwind for sustained wages growth. In Japan, wage increases depend on seniority, so job mobility is low and companies typically find it unnecessary to raise wages to retain staff. This also disincentivises employees from reskilling or making career changes into higher growth areas. In 2016, then Govenor Kuroda outlined low job mobility as a key challenge for the labour market and the country’s growth potential.

Further, participation has recently been rising thanks to a growing cohort of part-time workers, primarily women and those aged 65 and above. Wage growth is slower for part time workers, and the loss of tax and social benefits for secondary income earners dissaude many from labour market and the country’s growth potential.

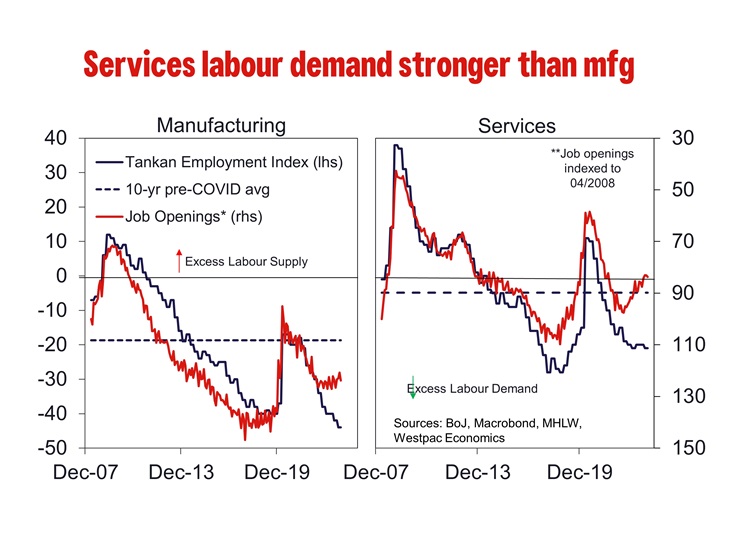

While some large companies such as Suntory and Nomura have publicly committed to raising salaries by 7-16%, many others will hold back believing the labour they will require will remain available. According to the Tankan survey, firms are reporting labour shortages as less severe than pre-COVID in manufacturing; while shortages in services persist to what was seen in the early 1990s. The number of new job openings in the services sector are also settling below the pre-COVID peak while new openings in manufacturing continue to decline. Part of this reflects a structural decline in manufacturing jobs, with south-east Asia providing attractive alternative locations for facilities and automation also limiting labour demand. Given manufacturing employs around 15% of the labour force, weaker demand will act as a drag on aggregate wages. This points to a softening labour market overall but also diverging outcomes for services and manufacturing.

Small businesses have been particularly unenthusiastic about raising wages. As an example, a survey completed by Johnan Shinkin Bank and the Tokyo Shimbun daily reported 72.8% of small and medium-sized businesses in the Tokyo metropolitan area said they ” have no plans to raise wages this year”. Smaller employers tend to make up the bulk of employers and so can have a significant effect on aggregate outcomes. Their reluctance is arguably principally due to an inability to pass on higher costs to consumers, particularly when households are price sensitive as they are now, but also as they are much less able to scale up and therefore benefit from efficiency and large markets.

One segment of the labour market that is showing increasing wages is younger Japanese workers. They are more likely to have in demand skills, particularly for high-skill work, and are also more likely to job hop being early in their careers. As such, wage gains are thought to be skewed towards younger workers. BoJ research also shows that wages for high skill workers are increasing. However given Japan’s ageing population and weak immigration program, young people make up a small fraction of the labour force, so wage gains in this cohort is unlikely to drive aggregate wage gains or consumption.

Looking beyond 2024, both cyclical and structural factors are likely to limit wage gains and thereby keep a lid on domestic inflation pressures. While the second estimate for GDP has revised away recession, the economy remains weak and at risk of global developments. All this points to an absence of demand-side inflation pressures necessary to justify a tightening cycle of scale. While the BoJ can likely justify the end of negative rates in coming months, moving the policy materially above zero is unwarranted and potentially a decision that would put at risk all the work undertaken in recent years to aim to achieve the inflation target on a sustainable basis. All considered, the shunto wage outcome is unlikely to be the opportunity markets are hoping for a generational change in monetary policy.