{kind=link}

Summary

- We do not expect the FOMC to change the federal funds rate or alter its current pace of balance sheet runoff at its upcoming meeting on March 19-20.

- Since the Committee last met, the U.S. inflation data have come in a bit stronger than expected, while the labor market generally has remained resilient. With payroll growth still solid and inflation proving to be a bit stickier recently, we suspect the FOMC will still be seeking greater confidence at the end of its meeting next week that inflation is headed back to 2% on a durable basis.

- That said, beneath the robust headline figures, we see building evidence that the labor market is cooling and inflation is still slowing on trend. Chair Powell testified to Congress shortly before the March blackout period that the Committee is “not far” from the confidence needed to dial back the level of policy restriction.

- We now expect the FOMC will initiate the first cut to the federal funds rate at its June 12 meeting (our previous expectation was at the May 1 meeting). We look for 100 bps of easing in total this year and another 100 bps of easing over the course of 2025 to bring the fed funds target range to 3.25%-3.50% by year-end 2025.

- In light of the recent slate of data and Fed-speak, we see few changes to the post-meeting statement after a meaningful rework following the January meeting.

- The March meeting will include an update to the Committee’s Summary of Economic Projections (SEP). We do not expect material changes to the median projections for real GDP growth and the unemployment rate.

- The story is similar for inflation. Our most recent forecast projects headline and core PCE inflation of 2.3% and 2.5%, respectively, in 2024. The Committee’s median projection in the December SEP was 2.4% for both headline and core PCE, suggesting that the current outlook is not materially different from December for most FOMC members. We think the core PCE inflation median for 2024 will rise by a tenth or so, putting it closer to the midpoint of the central tendency range from December.

- That said, even if the magnitude of the changes to the outlook for growth and inflation are relatively small, the direction of the revisions likely will be toward a hotter outlook, i.e. faster growth, and higher inflation. Will the dots follow suit?

- Our base case is that the median dot for 2024 will remain unchanged at 4.625%, but the risks are skewed toward a higher median given the distribution of the prior dots and the recent run of inflation data. Similarly, we expect no change to the 2025 and 2026 median dots, though here too we think the risks are skewed to the upside.

- A slowdown in the pace of the Fed’s balance sheet runoff program also appears to be coming closer into view, and the Committee is likely to have a broad discussion of the central bank’s plan for quantitative tightening (QT) at the March meeting.

- Our base case remains that the FOMC will announce a plan to slow the pace of QT at its June meeting, although we would not be shocked if the Committee decided to do so one meeting earlier or later. Specifically, we expect the runoff caps for Treasury securities to be reduced to $30 billion while MBS caps are dropped to $20 billion starting on July 1. We anticipate this slower pace of QT running until year-end 2024.

A Little More Conversation, but Still No Action

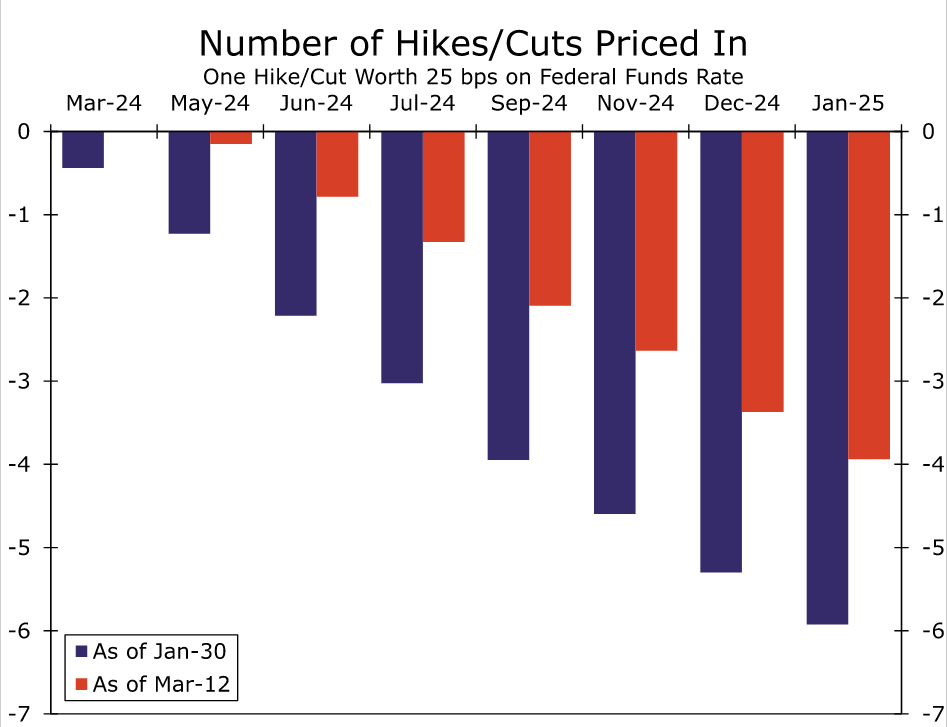

We do not expect any policy changes from the FOMC at its meeting next week, but the Committee’s post-meeting communications should shed more light on the potential path of policy adjustments later this year. The prospects of the first rate cut occurring on March 20 initially started to slip away at the end of the Committee’s last meeting on January 31. In the post-meeting press conference, Chair Powell shared that “I don’t think it’s likely that the Committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that.” Since then, generally stronger-than-expected data and the string of Fed officials indicating they are in no big rush to ease policy have driven down the odds of a rate cut at next week’s meeting to essentially nil. Expectations that a rate cut could first come at the May 1 meeting have also been pared back (Figure 1).

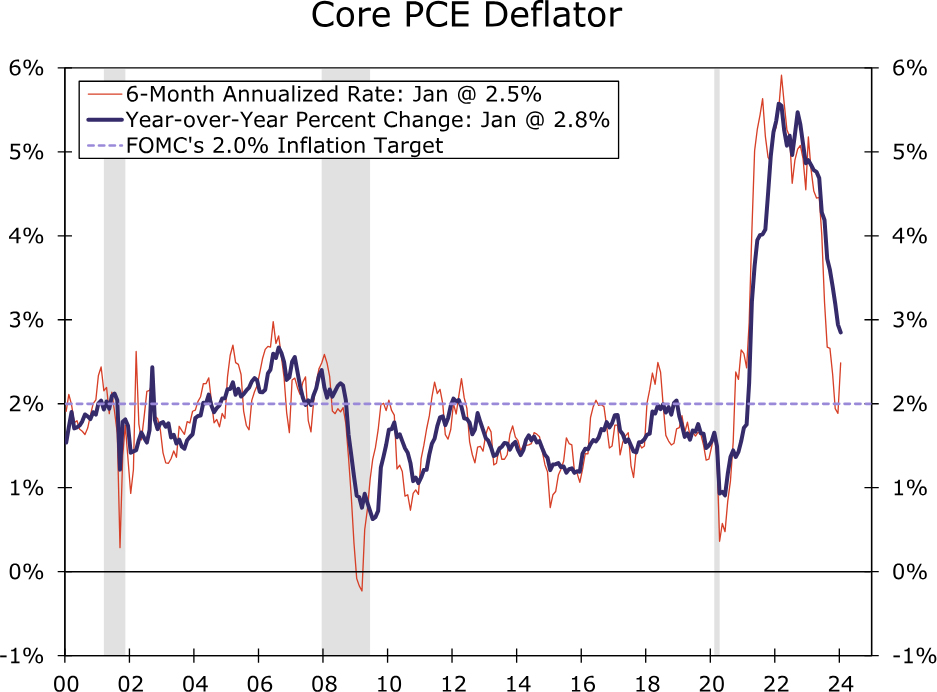

The tempered expectations for rate cuts follows a pickup in inflation to start the year. After the 6-month annualized rate of change in the core PCE deflator slowed to below 2% in the second half of last year, a hot print at the start of 2024 pushed this rate back up to 2.5% in January (Figure 2). The Consumer Price Index, which includes data through February, shows core inflation running at a 4.2% annualized rate the past three months compared to the 3.3% clip at the time of the FOMC’s past meeting.

Job growth has also held up well in recent months. In February, nonfarm payrolls again surpassed consensus expectations, and the three-month average pace of 265K remains well above the ~100K pace that we estimate is currently needed to absorb labor force entrants. With the jobs market holding up for now and inflation looking a little stickier of late, Fed officials over the inter-meeting period seem to largely be on the same page as Governor Waller when it comes to the near-term prospect of rate cuts: “What’s the rush?”

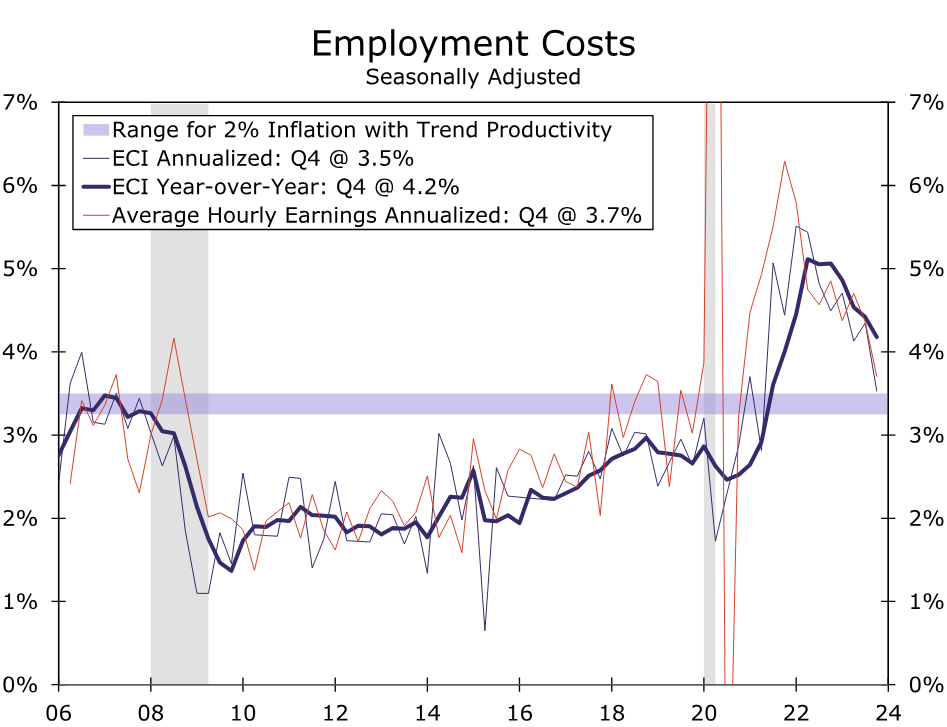

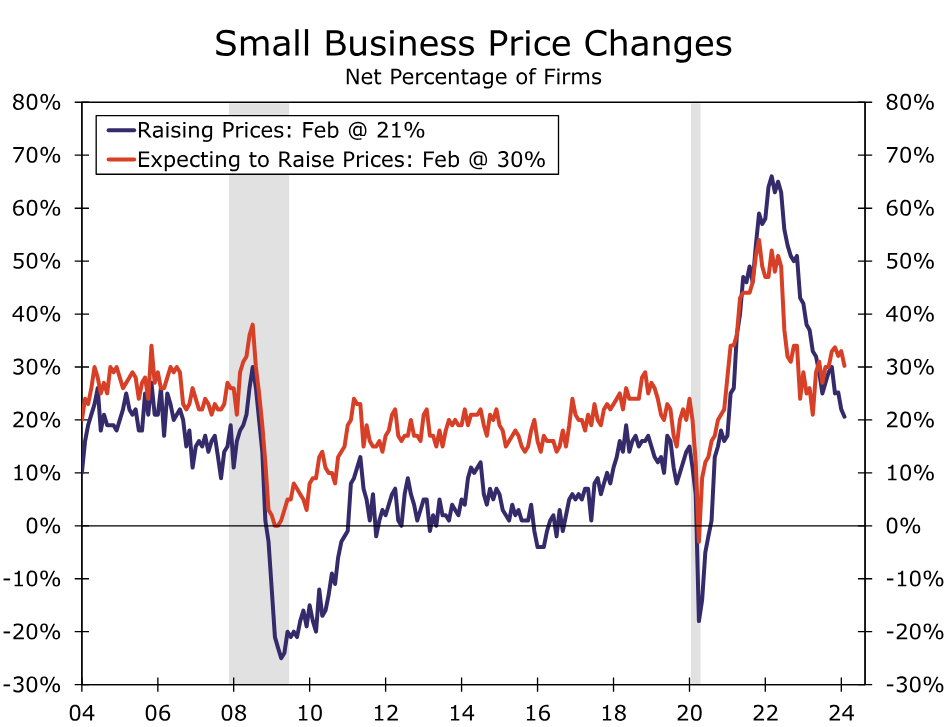

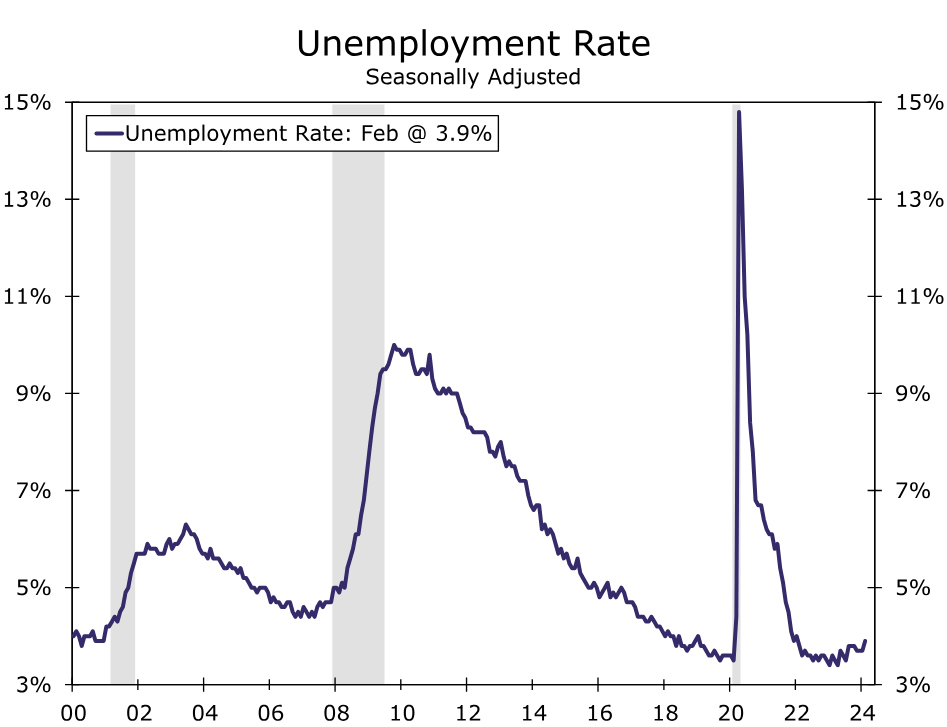

While most Fed officials seem in no hurry to ease policy, we expect the post-meeting communications to indicate that the FOMC continues to inch toward rate cuts later this year. Beyond the strength of nonfarm payrolls lies broad signs of labor market softening that suggest it does not need to cool significantly more for the Fed to achieve price stability. The unemployment rate reached a two-year high in February of 3.9%, while a pickup in layoff announcements and decline in job openings and hiring plans indicate demand for workers is diminishing. While wage growth currently remains stronger than during the last cycle, the trend continues to cool and, accounting for productivity growth, is not far from the pace consistent with the Fed’s inflation target of 2% (Figure 3). Businesses are having more difficulty passing on higher costs to consumers, as was noted in the Fed’s most recent Beige Book, and a shrinking share of businesses report raising prices (Figure 4). Furthermore, the improvement in supply chains since 2022 is helping to keep a lid on goods prices. With the jobs market in better balance and inflation pressures continuing to subside, Chair Powell testified to Congress shortly before the March blackout period that the Committee is “not far” from the confidence needed to dial back the level of policy restriction.

In light of the recent slate of data and Fed-speak, we see few changes to the post-meeting statement. The characterization of recent economic conditions may be tweaked slightly. We would not be surprised for the statement to note that the recent pace of economic activity appears to have cooled from the fourth quarter’s solid pace, or that the unemployment rate has moved up but remains low.

Elsewhere, adjustments are likely to be minimal after a meaningful rework following the January meeting. January’s statement removed the directional bias of the next rate move in a clear sign the hiking cycle probably has ended. The statement also noted that the risks to the inflation and employment sides of its mandate “are moving into better balance,” but the FOMC would need to see “greater confidence that inflation is moving sustainably back toward 2%” before it is appropriate to reduce the fed funds target range. With the three-month annualized rate of core CPI inflation strengthening to 4.2% through February, we suspect the FOMC will still be seeking greater confidence at the end of its meeting next weekand will not hint that a rate cut is imminent at its following meeting on May 1.

We now expect the FOMC will initiate the first cut to the federal funds rate at its June 12 meeting (our previous expectation was the May meeting). We look for 100 bps of easing in total this year and another 100 bps of easing over the course of 2025 to bring the fed funds target range to 3.25%-3.50% by year-end 2025. We will publish a more detailed update on our expectations for the path of the fed funds rate, inflation and economic growth tomorrow in our March Monthly Economic Outlook.

SEP: Will the 2024 Median Dot Go Higher?

With the statement likely to offer nothing new in terms of rate guidance, the updated Summary of Economic Projections (SEP) will shed light on how the Committee sees the path of interest rates, economic growth and inflation unfolding beyond the next couple of months. The current SEP was released at the December FOMC meeting and, as discussed above, the economy generally has remained solid over the past few months. Real GDP rose 3.1% on a year-ago basis in Q4-2023, half a percentage point stronger than the median Committee projection in the December SEP. Similarly, the unemployment rate was 3.9% in February, a tenth above the median projection for year-end 2023 but still two-tenths below the median projection for year-end 2024 (Figure 5). It is still early in the year, and the fundamental picture has not changed much since December, so we doubt most Committee members will want to make major changes in their projections for economic growth and unemployment. We expect the medians for growth and the unemployment rate to remain more or less unchanged.

The story on the inflation front is similar. PCE inflation finished 2023 roughly in line with the Committee’s expectations, but price growth topped expectations in January. Our most recent forecast looks for PCE inflation to be 2.3% year-over-year in Q4-2024. Excluding food and energy prices, we look for core PCE inflation of 2.5% over the same period. The median projections for 2024 inflation in the December SEP were 2.4% for both headline and core, and the central tendency ranges were 2.2%-2.5% and 2.4%-2.7%. This suggests to us that the inflation outlook is not materially different from what it was in December for most participants. We think the core PCE inflation median for 2024 probably will rise by a tenth or so, putting it closer to the midpoint of the central tendency range from December. Upward revisions much larger than this would surprise us and suggest that the Committee is more worried about the recent inflation data.

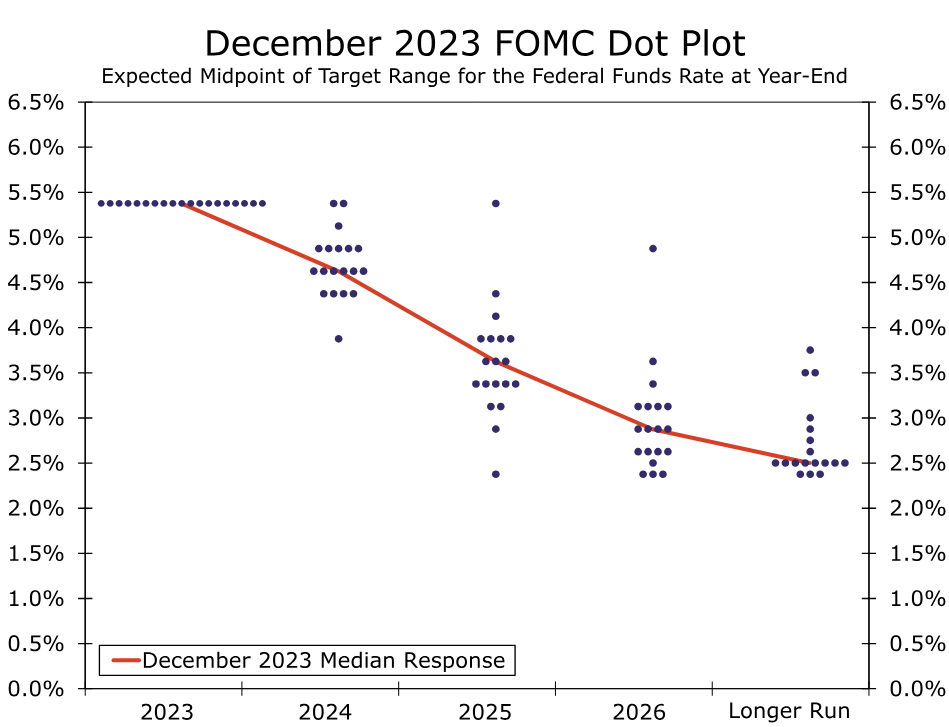

On balance, we expect the revisions to the Committee’s expectations for growth, unemployment and inflation to be relatively modest. However, we think the direction of these revisions will be toward a hotter outlook, i.e. faster growth, and higher inflation. This raises the question of whether the dots will follow suit. The median dot for 2024 currently sits at 4.625%, implying 75 bps of rate cuts by year-end (Figure 6). The distribution of the 2024 dots has an upward bias. Eight participants submitted projections in December with less than 75 bps of easing, while just five participants penciled in more than 75 bps of cuts. As a result, if just two participants shift from 75 bps of easing to 50 bps, the median will move from the former to the latter.

Our base case is that the median dot for 2024 will remain unchanged at 4.625%, but the risks are skewed toward a higher median given the distribution of the December dots and the recent run of inflation data. Similarly, we expect no change to the 2025 and 2026 median dots, though here too we think the risks are skewed to the upside.

QT Discussion to Occur at March Meeting

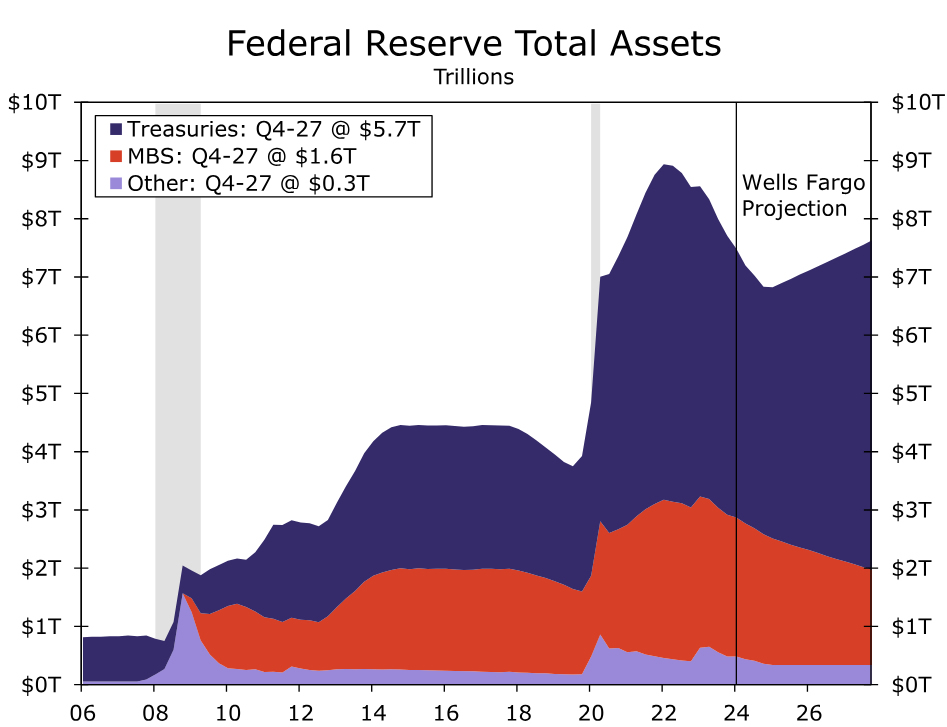

The FOMC is not only inching closer to cutting the fed funds rate. A slowdown in the pace of the Fed’s balance sheet runoff program also appears to be coming closer into view. In his post-meeting press conference after the January FOMC meeting, Chair Powell made clear that the Committee would engage in a broad discussion of the central bank’s balance sheet runoff program, more commonly know as quantitative tightening (QT), at the March meeting. The FOMC began allowing a maximum of $30 billion of Treasury securities and $17.5 billion of mortgage-backed securities (MBS) per month to roll off its balance sheet in June 2022. These caps were increased to $60 billion and $35 billion, respectively, in September 2022, and they have subsequently remained unchanged. At present, the Fed’s balance sheet totals roughly $7.5 trillion, down from nearly $9 trillion at its peak in Q2-2022.

Our base case remains that the FOMC will announce a plan to slow the pace of QT at its June meeting, although we would not be shocked if the Committee decided to do so one meeting earlier or later (May 1 or July 31). Specifically, we expect the runoff caps for Treasury securities to be reduced to $30 billion while MBS caps are dropped to $20 billion starting on July 1. We anticipate this slower pace of QT running until year-end 2024. Starting in 2025, we look for balance sheet growth to resume to accommodate organic growth in liabilities (e.g., paper currency and bank reserves). We expect the FOMC will continue to passively reduce its MBS holdings in 2025 and beyond while replacing these MBS with Treasury securities, a move that would replicate what occurred in 2019.

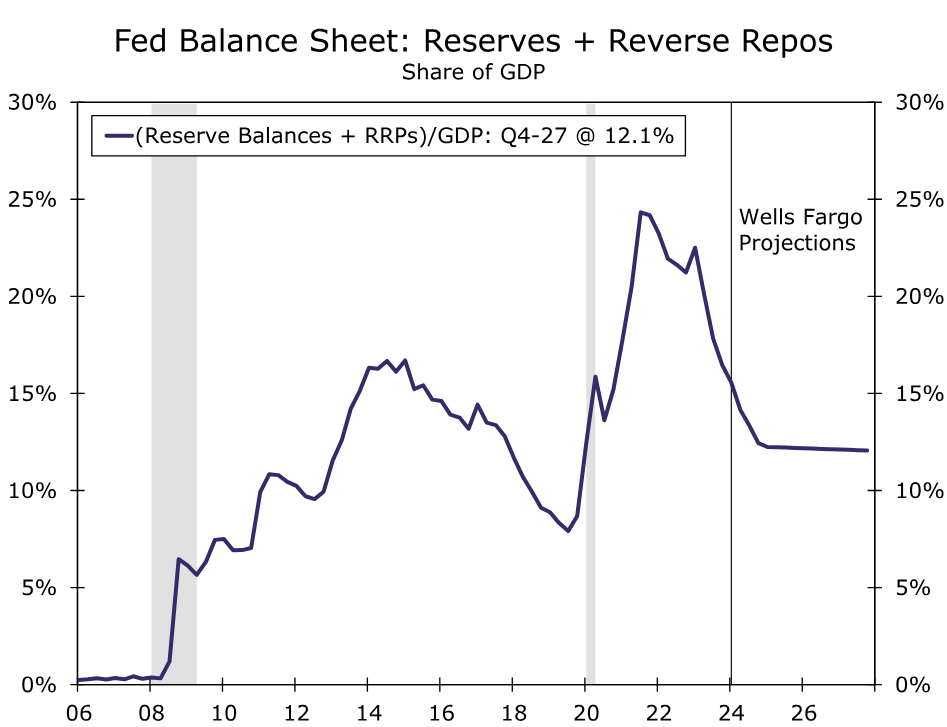

If our forecast is realized, the Fed’s balance sheet would reach a trough of $6.8 trillion or so at year-end 2024 and begin growing gradually again thereafter (Figure 7). The nadir in the Fed’s balance sheet would be only a bit higher than the $6.5 trillion projection in our “middle-of-the-road” scenario outlined in our report on QT from last October. In this scenario, we look for RRP balances to decline to about $200 billion by year-end, with bank reserves that are around $3 trillion at the trough. As a share of GDP, this would represent a meaningful liquidity buffer relative to pre-pandemic levels (Figure 8).

1 – Quotation from Governor Waller at the Finding Forward Speaker Series at the University of St. Thomas on February 22, 2024.