{kind=link}

- Bank of Canada kicks off March round of central bank meetings

- Dovish tilt is possible after CPI drops back below 3.0%

- Wednesday’s decision, due 14:45 GMT, may deepen loonie’s losses

Progress on inflation

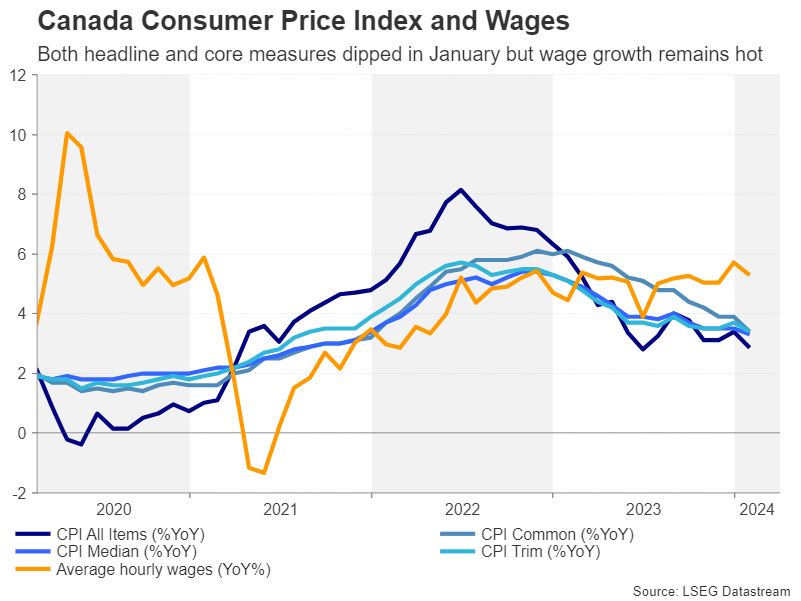

The Bank of Canada heads towards its second policy meeting of the year with some good news on the inflation front. The consumer price index eased to 2.9% y/y in January from 3.4%, falling below 3.0% for the first time since June 2023 when the disinflation process came to a pause.

Crucially for policymakers, all three of the Bank of Canada’s core measures of inflation tumbled in January to levels last seen in late 2021. Whilst it’s too early to know whether this will be another temporary dip, the likelihood that inflation will soon hit 2% has gone up, raising the prospect of a rate cut sooner rather than later.

Overall rate cut expectations have been pared back since the start of the year, in line with the repricing for the Fed and other major central banks. Nevertheless, a 25-basis-point rate cut is now almost fully priced in for June.

Will the BoC flag a rate cut?

The Bank of Canada had predicted in January that inflation would hold around 3.0% in the first half of 2024 so the lower-than-expected CPI print could prompt officials to anticipate a faster return to the 2% target.

However, policymakers will likely want to see more evidence of inflation heading towards 2% in a sustainable manner and more data won’t become available until the Bank of Canada’s April meeting when coincidentally a new set of projections are also due to be published. Hence, a major policy shift is unlikely at the March meeting.

Not a good start to 2024 for the loonie

Yet, for the Canadian dollar, which has been on the backfoot versus the greenback all year, even a slight dovish lean by tweaking the language in the statement could worsen the bearish pressure.

Dollar/loonie is currently trading near two-month highs as the pair eyes the 1.3600 level. A dovish hold on Wednesday could see the pair test the 61.8% Fibonacci retracement level of the November-December downleg before aiming for the 78.6% Fibonacci of 1.3745.

However, if the BoC maintains a cautious stance amid concerns about the housing market heating up again, dollar/loonie could pull back towards its ascending trendline that is being tracked by the 20-day moving average. A bigger correction would bring the 50-day moving average into scope at 1.3439.

Canada’s property market conundrum

Canada’s property slump appears to have bottomed and there are some indications that house prices have started to rise again. A recovery in the housing market at a time when shelter costs are already very high due to rising rental prices and higher mortgage costs could complicate things for the Bank of Canada.

Shelter inflation is currently the biggest upward contributor to prices in Canada and cutting rates risks exacerbating the problem.

A brighter outlook

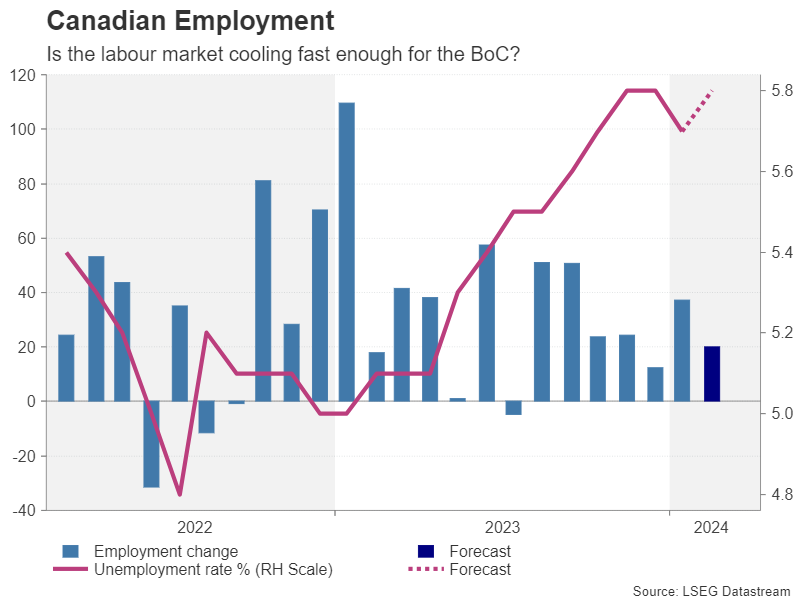

The rebound in housing comes amid a broader bounce back in economic activity. Canada’s economy returned to growth in the final quarter of 2024 following a contraction in GDP in Q3. The jobs market also appears to be on the mend with the unemployment ticking lower in January.

The next employment report is released on Friday (13:30 GMT) and investors will be watching for more signs that jobs growth is picking up. With wage growth running above 5.0%, a hot labour market would be another obstacle for the Bank of Canada to cut rates anytime soon.