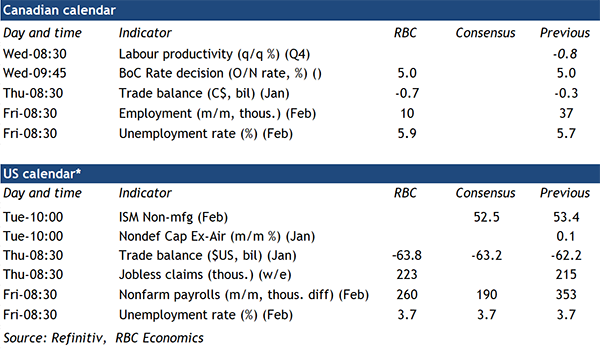

{kind=link}

The Bank of Canada is widely expected to maintain the overnight rate steady again at its meeting on Wednesday. An announcement on the ending of quantitative tightening is unlikely but we expect that to follow later in April. Over past meetings, the BoC has been gradually and cautiously moving towards a more dovish stance. Language around the need to hike rates further was already dropped in January and is unlikely to reappear in the statement next week. The central bank will instead continue to highlight softening in aggregate demand while reiterating that inflation pressures, although easing are still a risk.

Economic data since the last monetary policy meeting in January largely confirmed the weakening of the Canadian economy. The 1% annualized increase in gross domestic product in Q4 2023 was above the flat reading that the BoC expected. But details were much softer with growth in Q4 coming almost entirely from net exports. Domestic consumers and businesses on the other hand continued to pull back spending and investment activities. GDP growth was, again, slower on a per capita basis as population growth outpaced output for a sixth consecutive quarter.

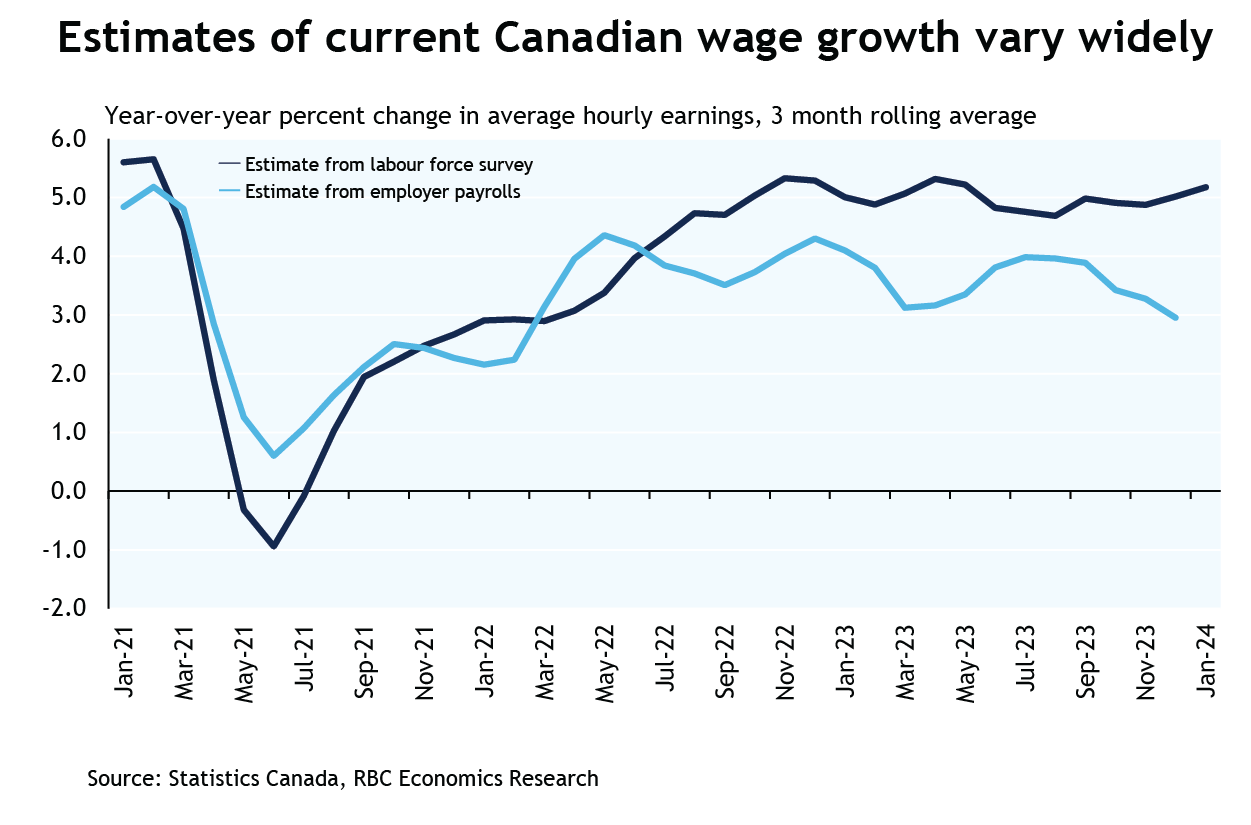

We expect February labour market data released on Friday after the BoC’s decision to show another gain in employment. It will however not be large enough to prevent an increase in the unemployment rate to 5.9% as hiring demand keeps falling short of the rising supply of workers. Labour market numbers for January were firmer than expected with wage growth remaining high. But lower job openings continue to highlight slowing labour demand. Other Statistics Canada estimates of wage growth derived from business payrolls submissions have slowed more significantly. The silver lining of all the softening in the economy is that inflation pressures will likely continue to ease rather than reaccelerate. Our base case continues to assume the BoC will start moving the overnight rate lower in June after more data confirming easing inflation back towards target.

Week ahead data watch:

January’s Canadian trade data is likely to show monthly declines in both export and exports with rail carloadings (-7.7%)— contracting sharply that month. Oil prices went up 2.8%, and that will impact the value of energy exports and imports. Overall, we expect the trade deficit ($700 million) to widen from the prior month.

The U.S. trade balance (US$-63.8B) likely widened in January given the goods deficits from the advance trade report increased by US$2.3B. Much of that was driven by higher imports of autos, and capital goods.

We expect February U.S. payroll numbers to show another solid employment gain, with growth mainly coming from the leisure and hospitality, health care, and government sectors. We expect the unemployment rate to hold steady at 3.7%.