{kind=link}

U.S. Highlights

U.S. inflation rose more than anticipated to start the year, on a Consumer Price Index basis, largely due to greater price pressures within the services sector.

However, retail spending surprised to the downside in January, suggesting that consumer spending may be less vigorous than the stunning pace of last year.

A slowdown in housing starts and less optimistic small businesses also suggest that economic momentum may be cooling.

Canadian Highlights

- Canadian home sales increased for the second straight month in January. However, price growth was soggy, with sellers lowering their price expectations. However, firmer price growth is likely moving forward.

- Homebuilders continue to break ground on new homes at an impressive pace. However, starts still trail fundamental housing requirements flowing from Canada’s sizzling population growth.

- Next week’s inflation report is likely to show little change in overall inflation and sticky core measures, keeping policymakers vigilant on rates.

U.S. – Inflation Progress Stalls and Spending Falls in January

This week saw some key data releases to help gauge the state of the U.S. economy at the start of 2024, and the likely timing of a Fed rate cut. Among them were the CPI inflation and retail sales reports for January. While inflation was higher than expected, retail spending came in notably lower. Markets reacted strongly to the inflation data with stocks falling sharply and treasury yields rising.

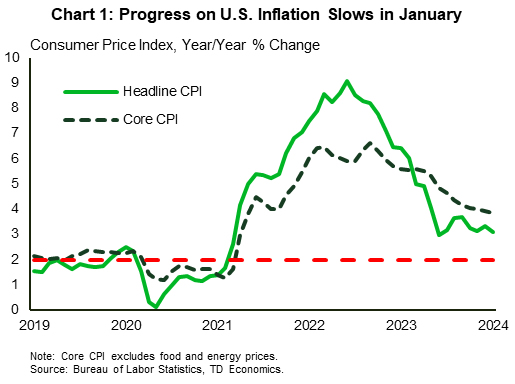

Taking a closer looker at CPI, the headline figure came in at 3.1% year-on-year (Chart 1). While this was lower than December’s 3.4%, it was higher than market expectations for 2.9%. The core measure matched December’s pace at 3.9%, but again was higher than expectations (3.7%). The near-term movements showed that progress on the disinflation front stalled a bit, largely due to services. Both monthly headline and core inflation accelerated relative to December. Also, both the 3-month and 6-month annualized growth for core CPI accelerated, suggesting that the process to tame inflation is likely to progress in uneven spurts. The producer price index corroborated the stalled CPI signal, with the PPI rising by 0.3% m/m in January (markets expected 0.1%) relative to -0.1% in December.

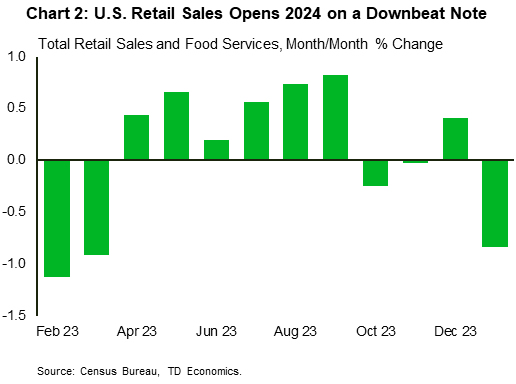

Turning to retail spending, consumers were a lot less jolly coming off the holiday season. Retail sales declined by 0.8% m/m in January (Chart 2). The sizeable decline was much larger than market expectations, however severe winter weather during January likely played a part in keeping consumers on the sidelines. Technical aspects of how the seasonally adjusted data is calculated may also have contributed to the relatively large decline. Nonetheless, the pullback suggests that consumer spending may be less of tailwind to U.S. economic resilience than it was last year.

Signals from the small business sector also suggest that economic activity might be slower in 2024. The NFIB’s small business optimism index declined to 89.9 from 91.1 in December, marking the biggest monthly decline since late-2022. On balance, small firms were generally less upbeat about their economic prospects, with the net percent of firms anticipating a better economy falling by 2 points. Given the higher exposure of small businesses to domestic economic conditions compared to larger firms, their downbeat mood points to headwinds ahead for the economy.

On the housing front, starts also disappointed expectations falling 14.8% to a five-month low (1.33 million) in January. The decline was in both the single and multi-family segments. Permits for future construction also fell on the month, implying that recovery in the housing market will be slow as buyers await lower mortgage rates.

Overall, data for January largely came in below expectations. This has left many market participants wondering what it all means for the timing of rate cuts. FOMC members have repeatedly stated that they need to see steady evidence that inflation is on a consistent path back to 2%. While the CPI and PPI data suggest that progress may be slow going for a bit, the pullback in other indicators point to an economy that is cooling. As such, Fed members may soon have the evidence that they need to begin the cutting cycle – it may just be later than markets desire.

Canada – Housing to Offer Little Shelter from Inflation

Canada’s economic calendar was relatively light this week, so markets took their cue from developments south of the border. A hotter-than-expected U.S. inflation report reminded markets that the fight is not over, prompting a re-pricing of rate cut expectations. The prospect of delayed fed rate cuts pushed U.S. yields higher, dragging their Canadian counterparts along with them, while also weighing on the loonie. The Canadian 10-year yield hit 3.67% early in the week – the highest since November, before it retreated into week’s end on softer U.S. consumer spending data.

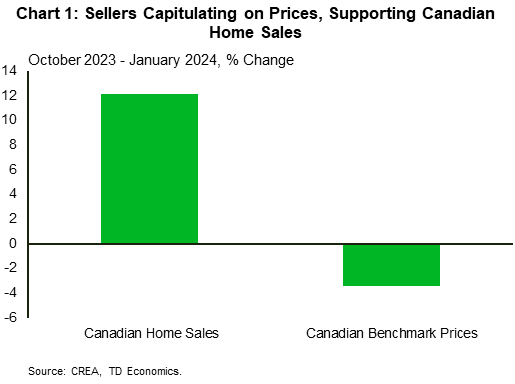

Although the Canadian data slate was light this week, it certainly wasn’t barren. Housing took centre stage, thanks to reports on home sales and prices, alongside the latest data on homebuilding. Home sales increased for the second straight month in January, benefitting from lower borrowing costs in recent months, favourable weather conditions, and ample pent-up demand. The signal from home prices was much softer, with average home prices up only modestly while quality-adjusted benchmark prices declined.

Looking at the big picture, home sales have surged since rates broke meaningfully lower in October, while price growth has lagged (Chart 1). Our view on this dichotomy is that sellers have lowered the price expectations in order to move their homes, especially in Ontario and B.C., where conditions have recently favoured buyers. However, with supply/demand conditions now much more balanced in these markets, weak price performances are likely in the rear view.

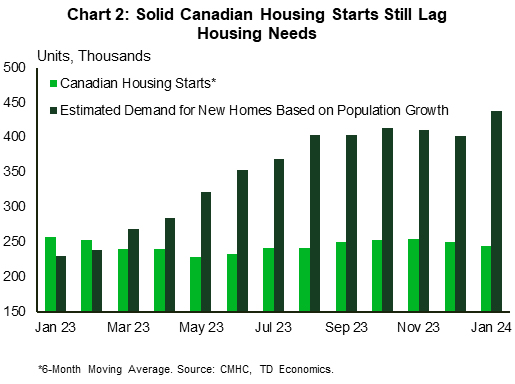

This is not just a story for the short-term, either, as Canadian housing shortages should support higher prices over the longer-term. This week, we received homebuilding data which showed a January decline, but that starts are still elevated on a trend basis. However, the rate at which builders are breaking ground continues to lag fundamental requirements from tremendously strong population growth which has persisted into this year (Chart 2).

Resurgent housing demand, alongside tighter markets, is sure to raise some eyebrows at the Bank of Canada. Rising housing market activity supports GDP growth through a direct boost to residential investment and can stoke consumer spending as well. Meanwhile, home prices feed directly into the CPI through the shelter component, which accounts for nearly 30% of the index. We agree with the Bank of Canada that inflation can hit its 2% target, despite only gradual improvements in the shelter component. However, if the housing market heats up by more than policymakers expect, this could delay rate cuts and/or alter the speed at which they’re delivered.

We won’t have to wait long to observe the impacts of housing market activity on consumer costs, as the January CPI report is on tap next week. The consensus expectation is that overall inflation was little changed last month, while the Bank’s preferred core measures are likely to remain sticky at above 3.5%. The Canadian inflation battle clearly still has legs, which will keep the Bank vigilant on rates.