{kind=link}

Summary

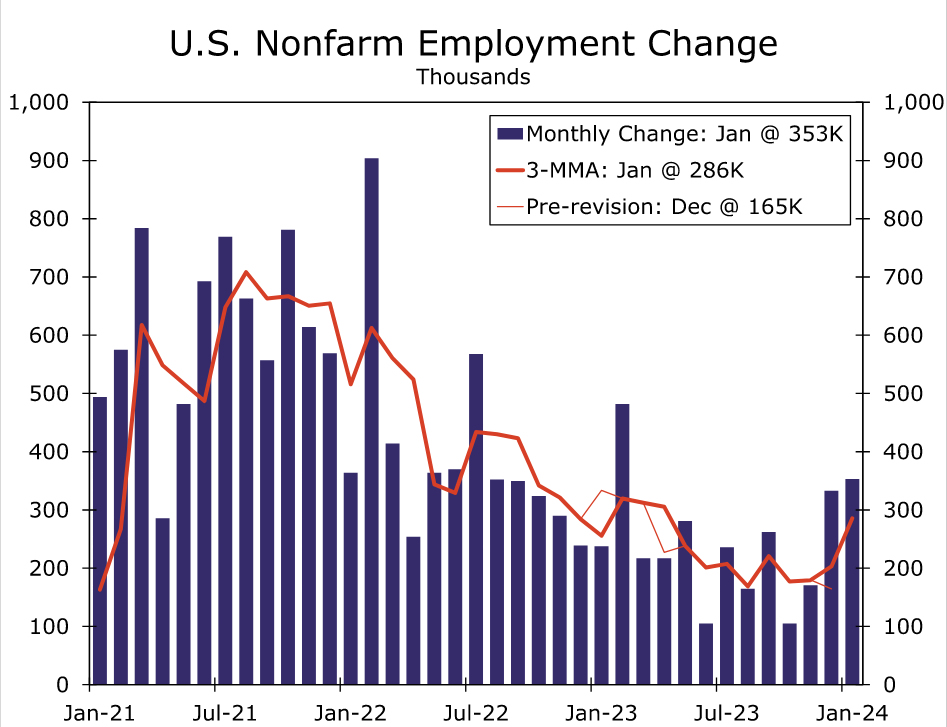

Hiring once again came out of the gate strong in 2023. Nonfarm payrolls rose by 353K in January, blowing past consensus expectations for a 185K gain. What’s more, revisions point to stronger momentum in hiring through the end of last year; payrolls in the fourth quarter of 2023 are now reported to have grown an average of 203K compared to 165K prior to today’s report.

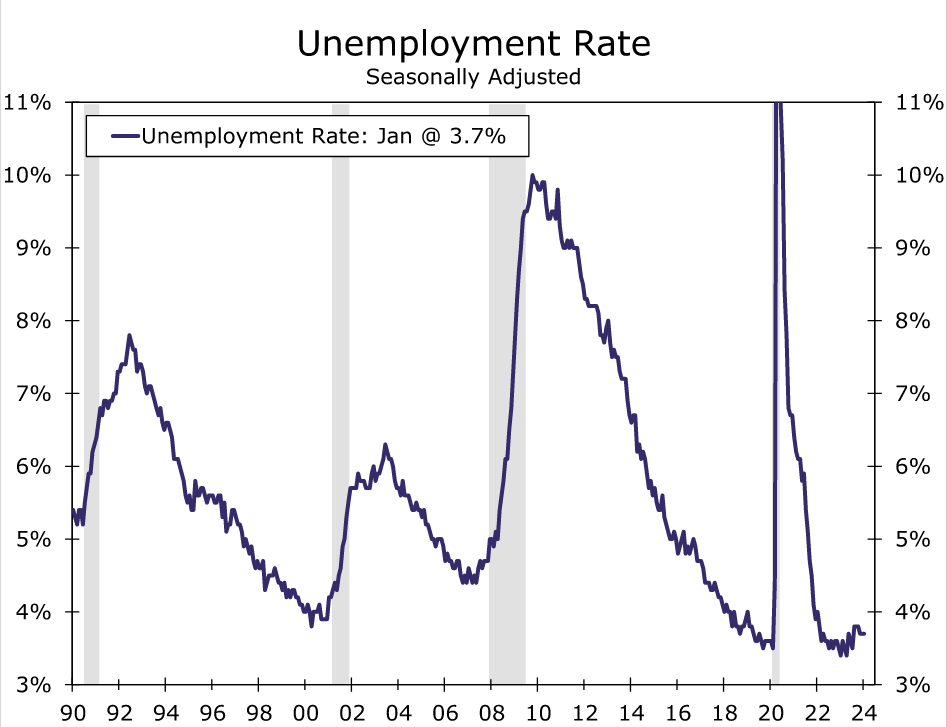

Overall, the jobs market appears to be on firmer footing than implied only a month ago. In addition to the solid number of jobs added, employment gains broadened across industries in January. Joblessness also remains low, with the unemployment rate unchanged at 3.7%. Average hourly earnings growth of 0.6% in January, double the expected gain, further points to a still-strong labor market.

Chair Powell made clear in his post-meeting press conference on Wednesday that a rate cut in March was not the Committee’s base case. But he left open the possibility that a cut could occur if the economic data came in unexpectedly soft. Today’s employment report reinforces the view that a March rate cut is not in the cards. Rate cuts are coming this year, but we think it will take until the May meeting for the FOMC to reach a consensus that inflation is on a sustainable path to 2%.

A Knockout Report

Nonfarm payroll growth in January blew past expectations, rising 353K compared to consensus expectations for a 185K gain. The sizzling print reflects that while employers are not as eager to take on new workers as they were a year or two ago, they remain reluctant to let existing workers go. January typically sees sharp drops in employment on a non-seasonally adjusted basis, and this January payrolls fell by 2.64 million compared to an average of 2.74 million the prior five years and 2.94 million the five years preceding the pandemic.

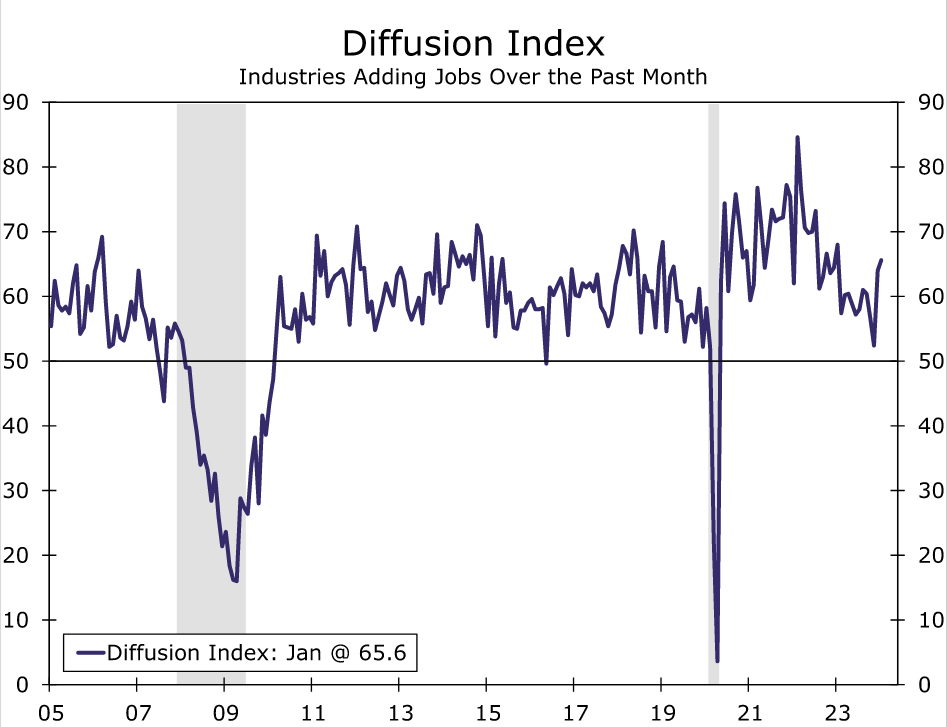

Employment growth in January was more broadly-based across industries relative to recent months. The labor market diffusion index, a measure of job growth breadth, posted its highest reading since January 2023. Job gains were led by professional and business services (+74K), health care (+70K), retail trade (+45K) and government (+36K).

The good news extended beyond just January. Revisions to the prior two months’ added another 126K to job growth in December and November. This pushed the three-month moving average on nonfarm payroll growth up to 286K, its highest reading since April 2023.

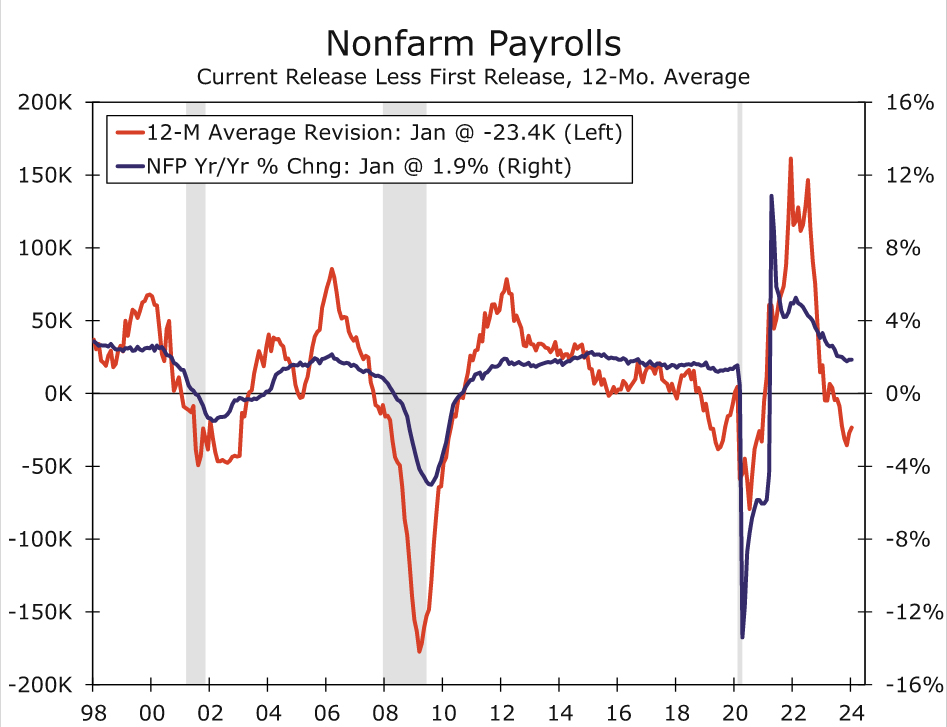

In addition to the usual revisions due to late survey responses to the prior two months data, today’s report included annual benchmark revisions along with revised seasonal factors to the Establishment Survey. The benchmark showed a more moderate pace of hiring in 2022 and early 2023. The level of payrolls as of March 2023 was revised down by 266K, which was a bit smaller than the preliminary estimates for a decline of 306K and the largest downward revision since 2019 (-489K). The monthly trend in hiring late in the year looks stronger than it did before the revisions. Payrolls in the fourth quarter are now reported to have increased an average of 203K per month compared to 165K prior to today’s report.

In another sign that the labor market remains on solid footing, the unemployment rate held at 3.7%, bucking expectations for an increase to 3.8%. January’s Household Survey data included new population controls, but unlike the Establishment Survey, prior monthly data were not revised. Therefore, the changes in the level of household employment and the labor force are ineffective this month, but ratios such as the labor force participation rate and unemployment rate are more reliable. The unemployment rate points to a still-tight jobs market as the robust growth in labor supply through much of 2023 has started to fizzle. The labor force participation rate was unchanged at 62.5% in January, down from 62.8% as recently as November.

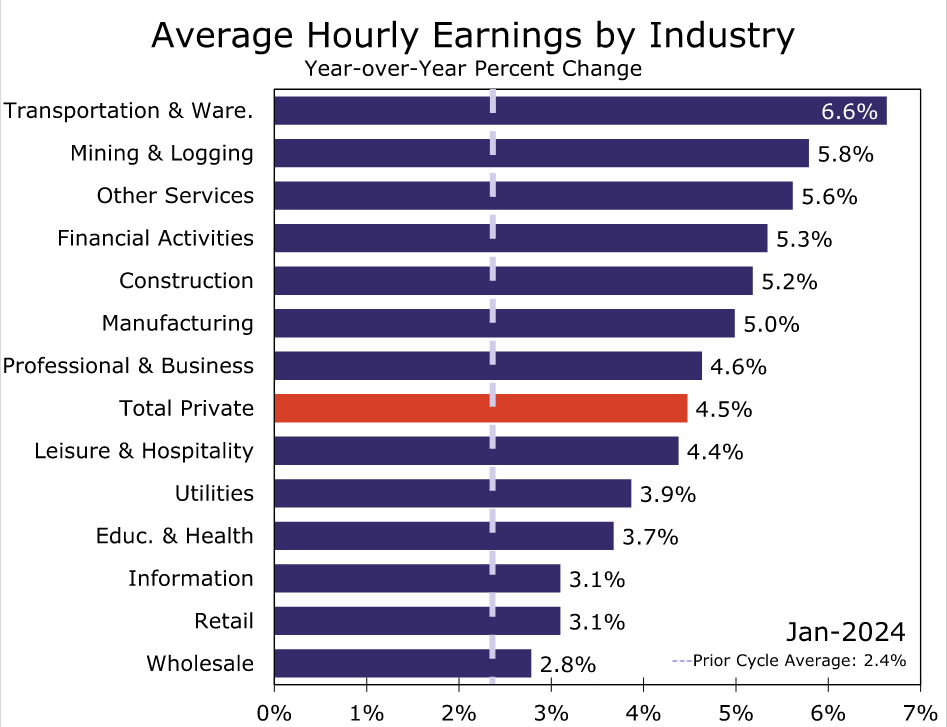

January’s average hourly earnings (AHE) further demonstrate that the jobs market is far from weak. AHE rose 0.6% in January, double the consensus forecast for a 0.3% increase. What’s more, strength was broad based, with nine of the 13 major industries posting monthly gains of at least 0.4%. Average hourly earnings among private sector workers have increased at a 5.4% annualized pace on a three-month basis and 4.5% on a 12-month basis. The pickup contrasts with the recent signal from the employment cost index that labor costs are falling back in line with the pace consistent with the Fed’s inflation target. However, average hourly earnings can be volatile on a monthly basis and are prone to revision, in addition to providing a narrower look at compensation costs (the ECI includes benefit costs in addition to wages & salaries as well as public sector workers). We put more weight on the ECI, and we suspect the FOMC will do the same. That said, the AHE data from today are yet another weight on the scale pointing to a stronger-than-expected labor market to start the year.

March Rate Cut Odds Fade Further

In his press conference after this week’s FOMC meeting, Chair Powell threw cold water on the idea of a rate cut at the next meeting on March 19-20. Powell stated that “based on the meeting today, I would tell you that I don’t think it’s likely that the Committee will reach a level of confidence by the time of the March meeting to identify March as the time [to cut rates]. But that’s to be seen.” Two employment reports and two CPI reports between the January and March meetings, as well as a slew of other economic data, left the door ajar for a March cut should the data point to more softness in inflation and the economy than expected.

Today’s employment report clearly reinforces the view that a rate cut is not coming at the March meeting. Nonfarm payroll growth is humming along at a much stronger pace than previously reported, and the unemployment rate remains low at 3.7%. The doves on the FOMC should feel comforted that the labor market is not on the precipice of a material deterioration in the near term, while the hawks likely will feel emboldened to wait for at least a few more inflation data points to ensure that the inflation genie is back in the bottle.