kept interest rates unchanged after raising them by 25bps in November. The November hike followed a period of four months where borrowing costs remained steady, and it was based on the assessment that the progress in driving inflation back within the 2-3% target range was slower than previously expected.){kind=link}

- RBA stands pat in December after considering a hike

- Rate cut bets come forth after weak data and slowing inflation

- But CPI details may allow officials to keep the tightening door open

- The decision will be announced on Tuesday at 03:30 GMT

December’s hawkish hold

At its December decision, the Reserve Bank of Australia (RBA) kept interest rates unchanged after raising them by 25bps in November. The November hike followed a period of four months where borrowing costs remained steady, and it was based on the assessment that the progress in driving inflation back within the 2-3% target range was slower than previously expected.

Officials took the sidelines again in December as the limited information on the domestic economy since November had been broadly in line with their expectations. However, they did not close the door to further tightening, noting that whether this will be needed will depend on the data and the evolving assessment of risks. The minutes of the gathering revealed that the board even discussed whether it was appropriate to raise rates by another 25bps.

Weak data spark rate cut speculation

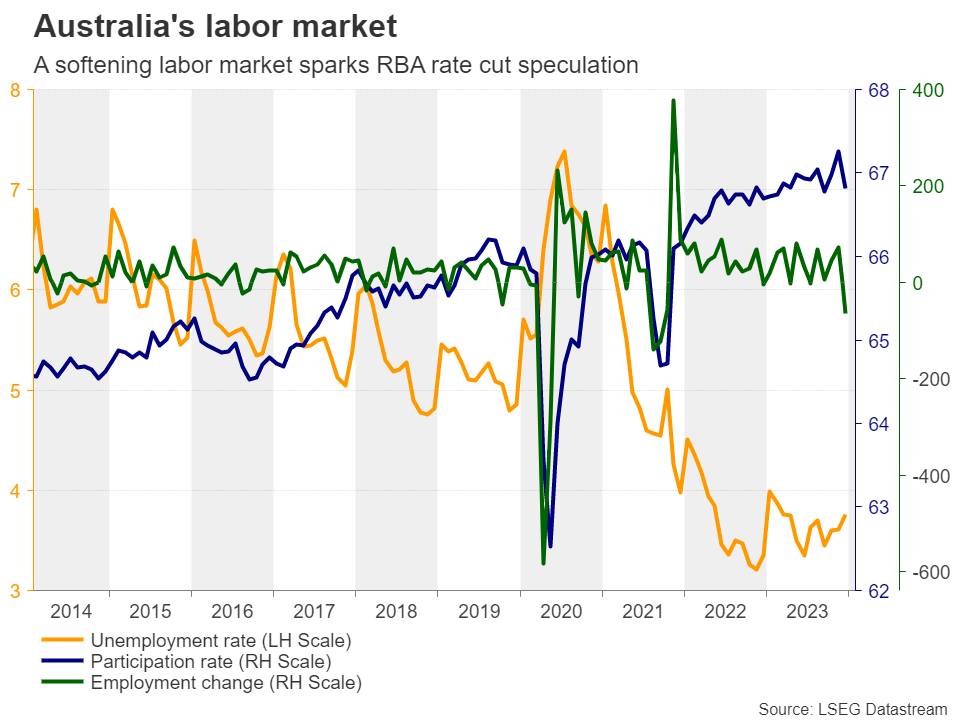

After the meeting, data revealed that the Australian economy continued to slow to 0.2% q/q from 0.4% in Q3, 2023, and although the employment and retail sales numbers for November came in better than expected, the December prints revealed weakness, with the labor market losing 106.6k jobs, which is the most since the COVID-related lockdowns.

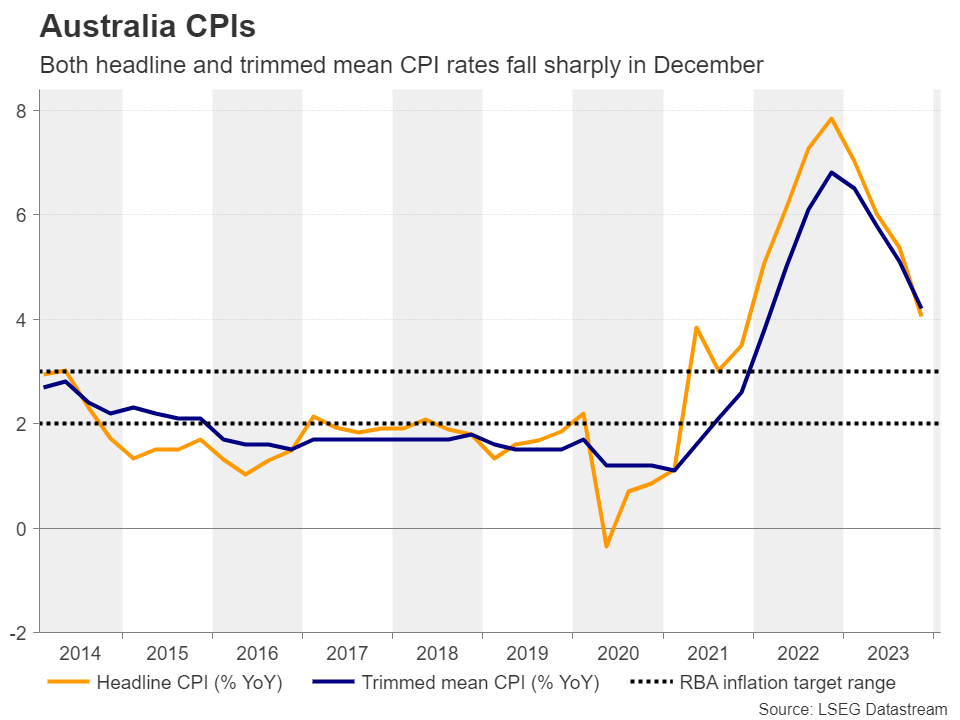

This has led investors to start speculating that interest rates have already peaked, and that the RBA’s next move will be a cut. Ahead of Wednesday’s CPI numbers, the market’s implied path was indicating a first 25bps reduction to be delivered in September. But that timing came forth following the bigger than expected slowdown in Australian inflation for Q4.

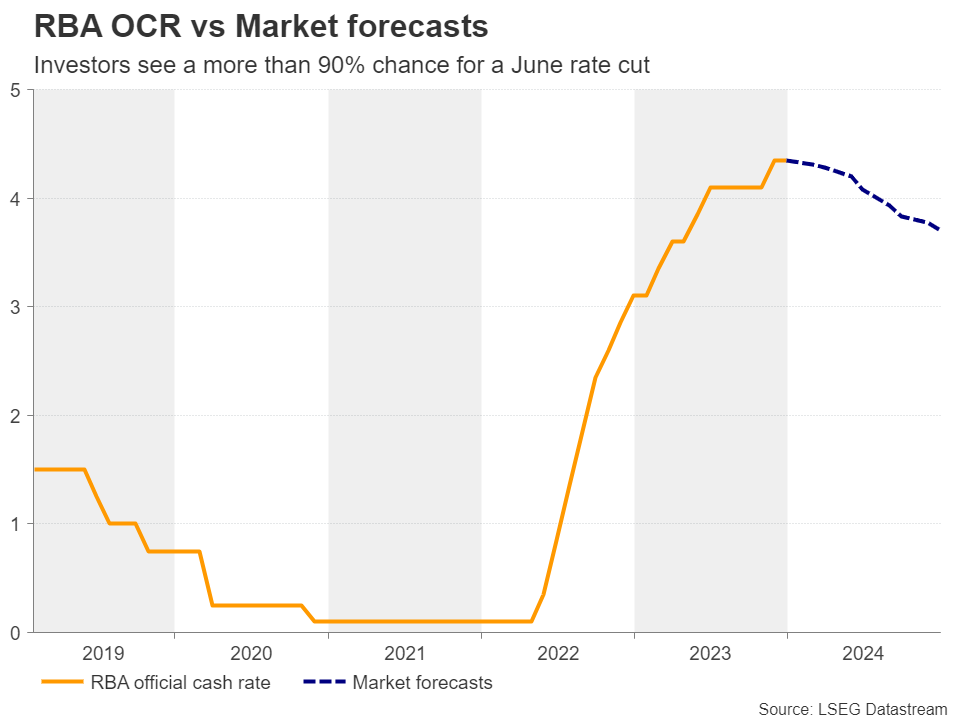

The headline CPI rate for the quarter dropped by more than a percentage point, to 4.1% from 5.4%, while the monthly y/y rate for December slipped to 3.4% from 4.3%, suggesting that it may not take long for inflation to return within the RBA’s target range of 2-3%. Investors are now pricing in a more than 90% probability for the Bank to cut rates in June, while they are factoring in nearly another 40bps worth of rate cuts by the end of the year.

Is this tightening crusade over?

The weak economic data and the slowdown in inflation may prompt policymakers to stay sidelined again when they meet for the first time this year, this coming Tuesday. However, with Governor Michelle Bullock making her latest appearances in her hawkish suit, they are unlikely to suddenly switch from a hiking bias to signaling rate cuts. Thus, the big question on everyone’s mind may be whether they will keep or drop their hiking bias.

The details of the CPI report revealed that non-tradable goods and services inflation, which are mostly driven by domestic demand, held at 5.4%, while rent inflation, although it eased somewhat, remained well elevated at 7.3%. With that in mind, policymakers may decide to keep the option of higher rates on the table for a while longer, at least until they are assured that inflation will not spiral out of control again.

China worries may keep aussie in check

Such a decision could prove positive for the aussie, but will it be enough to help the currency stage a long-lasting recovery? After all, apart from the market’s repricing regarding the future of Australian interest rates, the aussie is also affected by developments surrounding China, the world’s second largest economy and Australia’s main trading partner.

Although China’s decision to take measures and stabilize market confidence helped the risk-linked currency temporarily, the optimism was overshadowed by intensifying concerns about China’s real-estate sector after Evergrande was ordered to be liquidated. The improvement in the Chinese PMIs for January did not help either, perhaps as the manufacturing sector continued contracting for the fourth straight month.

Thus, should the RBA maintain its tightening bias, aussie/dollar could gain and perhaps break above 0.6620 or even above the 0.6650 barrier. However, any advances could remain limited near the 0.6730 area.

Now, in case the RBA signals the end of its tightening crusade, the pair may drop back down to the low of January 17, at around 0.6525, the break of which would confirm a lower low on the daily chart and perhaps pave the way towards the low of November 17 at around 0.6450.