{kind=link}

Summary

- As universally expected, the voting members of the FOMC decided unanimously at their meeting today to make no changes to the Fed’s policy stance, keeping the fed funds target range at 5.25-5.50% and maintaining the current pace of quantitative tightening.

- The FOMC also removed its implicit “bias” to tighten further. That is, the Committee dropped its reference toward “any additional policy firming that may be appropriate…”

- But we are not convinced the conditions will yet be in place to induce the FOMC to cut rates as soon as its March 20 meeting. The statement indicated that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.”

- A rate cut in March is not out of the question, but it would likely take another small increase in core PCE prices in January, in conjunction with soft data on economic activity, to compel the Committee to move in March.

- We look for the FOMC to cut rates by 25 bps at its meeting on May 1 and then another 100 bps by the end of 2024.

FOMC Removes “Bias” to Tighten Further

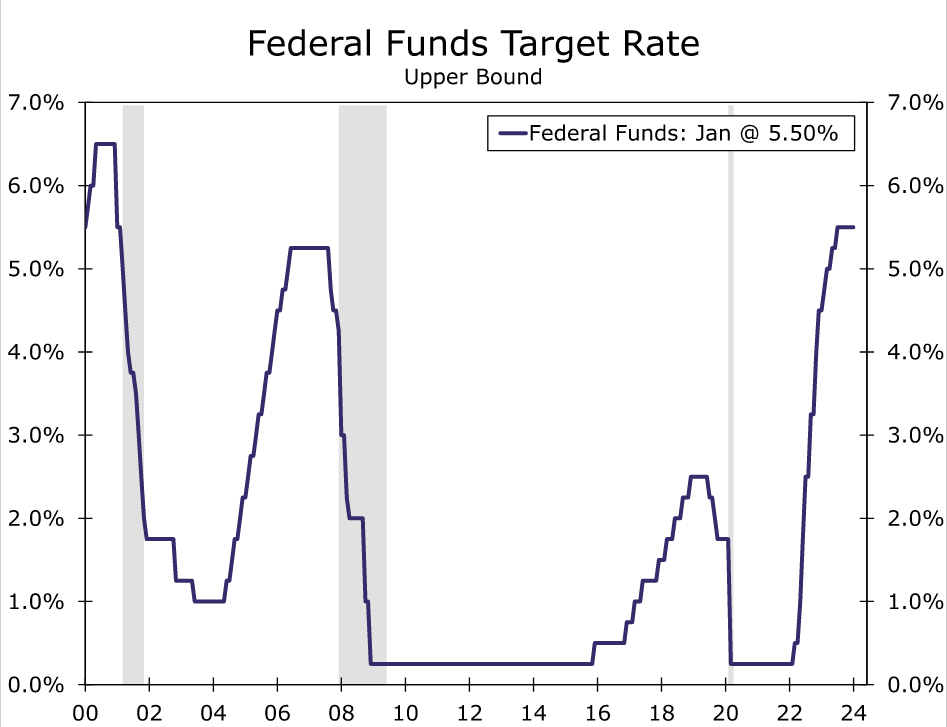

As universally expected, the voting members of the Federal Open Market Committee (FOMC) decided unanimously at their meeting today to make no changes to the Fed’s policy stance. After hiking rates by 525 bps between March 2022 and July 2023, the Committee has subsequently maintained its target range for the federal funds rate at 5.25%–5.50% (Figure 1).

In an important development, the Committee removed its implicit “bias” to tighten policy further in its post-meeting statement. That is, the statements that were released last autumn noted that the Committee would take into account a range of information when “determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time.” This sentence was tweaked in December to state “in determining the extent of any (emphasis ours) additional policy firming that may be appropriate…” Today’s statement noted that “the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks” when “considering any adjustment to the target range for the federal funds rate.” Until today, the FOMC statement was signaling that it was more likely that rates would need to rise further in the near term than to decline. The language in today’s statement signals a more balanced approach towards the next move for the fed funds rate. In the post-meeting press conference, however, Powell stated that “we believe that our policy rate is likely at its peak for this tightening cycle.”

But the Committee Needs “Greater Confidence” Inflation is Moving to 2%

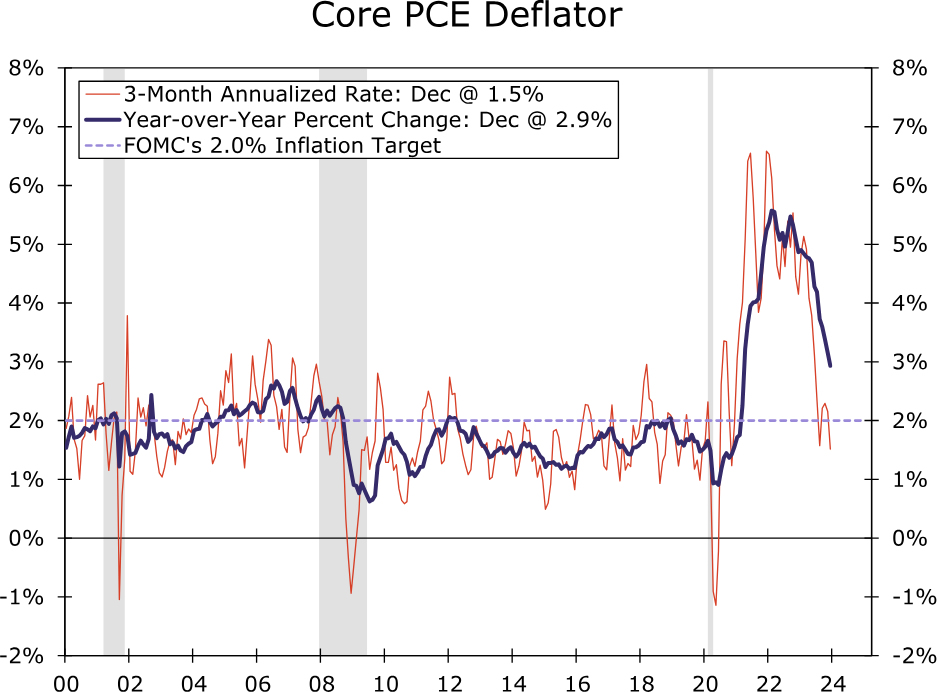

But we are not convinced the conditions will yet be in place to induce the FOMC to cut rates as soon as its March 20 meeting. Today’s statement also noted that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” As shown in Figure 2, the year-over-year change in core PCE inflation, which Fed officials believe is the best measure of the underlying rate of consumer price inflation, printed at 2.9% in December, which is still meaningfully above the Committee’s target of 2%. Although the core PCE deflator has risen at an annualized rate of only 1.5% over the past few months, it would be premature, in our view, to confidently claim that the economy is now out of the inflation woods. The FOMC will get only one more reading on PCE inflation before its next policy meeting on March 20. We are not entirely convinced that just one more data point will give the FOMC “greater confidence” that inflation is moving back toward 2% on a sustainable basis.

We Look for First Rate Cut in May

As we discussed in our most recent U.S. Economic Outlook, we look for the FOMC to cut rates by 25 bps at its meeting on May 1. Despite today’s statement that many market participants initially viewed as mildly “hawkish” – bond yields moved a few basis points higher in the immediate aftermath of the news – we maintain our view of a 25 bps rate cut on May 1. The FOMC will receive three more PCE prints between now and May 1. The 1.5% annualized rate of change in the core PCE deflator over the past three months indicates that the year-over-year rate of core PCE inflation will recede further in coming months. Moreover, we look for monthly changes in the core PCE deflator to remain benign in the foreseeable future. In our view, the FOMC will feel confident three months from now that inflation is moving back toward 2% on a sustained basis. A rate cut in March is not out of the question, but we would probably need to see a small increase in January core PCE prices, due at the end of February, in conjunction with soft data on economic activity, to compel the Committee to move in March.

We look for the FOMC to continue to cut rates after May. Specifically, we forecast that the Committee will reduce its target for the federal funds rate by 25 bps at each of the policy meetings on June 12, July 31 and September 18. As we noted in our most recent U.S. Economic Outlook, the decline in inflation that we anticipate in coming months will cause the real fed funds rate to rise further if the FOMC keeps its target range for the nominal fed funds rate unchanged. In other words, the real stance of monetary policy will tighten further if the FOMC stands pat. The Committee will need to reduce the target range in coming months just to keep the real stance of monetary policy unchanged. We currently forecast that the Committee will take a breather at its November 7 meeting, before ending the year with one more 25 bps cut on December 18. In sum, we forecast the FOMC will cut rates by 125 bps by the end of 2024. Stay tuned.