{kind=link}

- Quarterly Australian inflation on Wednesday; could surprise on the upside

- Chinese PMI surveys also on Wednesday; Chinese stock indices remains under pressure

- Aussie’s outperformance against the US dollar depends on stronger data releases

Market focusing on the Fed and US labour data

Amidst a week monopolized by Wednesday’s Fed meeting and Friday’s US labour market statistics, which could play a crucial role in the market’s short-term performance, the calendar also includes important data releases from both Australia and China. Especially the latter remains the big elephant in the room regarding its 2024 economic growth.

Aussie inflation in the spotlight

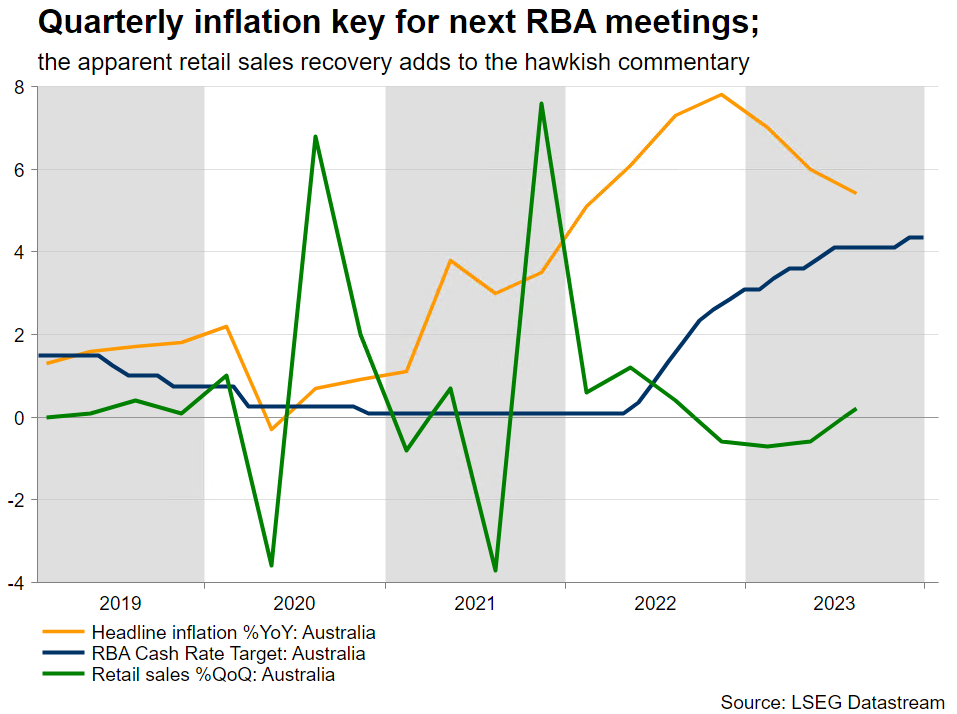

Starting with Down Under and the very important inflation report for the fourth quarter of 2023 will be released on Wednesday at 00.30 GMT. The Reserve Bank of Australia was the last one to hike by 25bps in November 2023 and has since maintained its hawkish stance. The December gathering kept the door open to further rate hikes, with the hawkish bias confirmed by the eye-opening minutes. More specifically, the comment that the “Board noted RBA staff forecast had inflation returning to top of band by end 2025 rather than midpoint” has thrown a spanner in the works for RBA doves. Nevertheless, the market is currently fully pricing in a 25bps rate cut by September 2024.

Like other central banks, the RBA remains data-driven. On Wednesday, the headline inflation is expected to show a 0.8% quarter-on-quarter change with the annual figure dropping to 4.3%, the lowest print since fourth quarter of 2021; the RBA’s favourite trimmed mean CPI is also forecast to record a similar slowdown.

Slim chance of an inflation upside surprise

With the October and November monthly CPI prints printing at 4.9% and 4.3% respectively, the December inflation figure has to slow down to 3.8% in order to confirm the market’s forecasts for the quarterly figure. However, considering that December inflation surprised on the upside across the major economies, there is a non-negligible chance of an upside surprise on Wednesday. Such an outcome would limit the RBA’s options at next week’s meeting.

China economic issues remain unaddressed

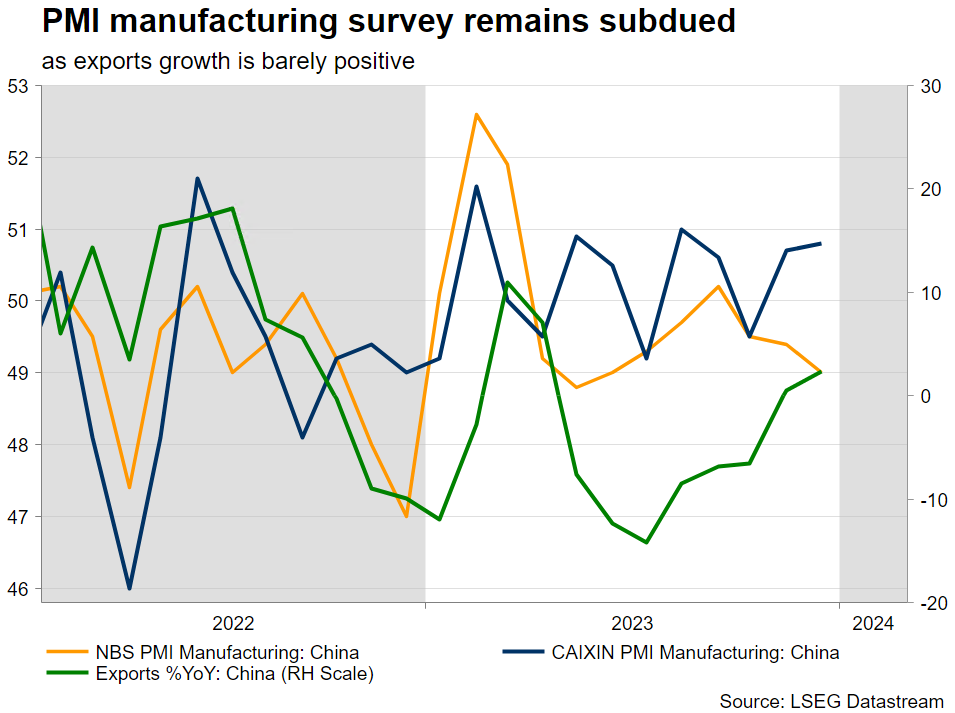

Turning to China, the January PMI surveys could enlighten the market on the economic undercurrents. Despite the numerous support programmes announced during 2023, the market remains unconvinced about their effectiveness. Other key economies like Australia and Germany are pinning their 2024 growth hopes on China overcoming its difficulties.

With the Chinese stock market remaining under severe selling pressure, the PBoC was forced to announce a 50bps Reserve requirement ratio (RRR) effective, from February 5, and has essentially also been enforcing a short sale ban. The Chinese authorities are trying to reverse the current market pessimism and are hoping that positive news from the economy will start to hit the airwaves soon. In addition, this RRR change offers significant support to domestic banks and opens the door for further announcements, possibly an MLF rate cut – the interest rate that banks borrow funds from the PBoC for up to one year – during the first quarter of 2024.

PMI surveys on the menu

Only time will tell if these measures prove successful as the market wants to see improving economic growth data to feel more confident. In this context the national PMI surveys are seen edging slightly higher with the manufacturing component remaining below 50 for the fourth consecutive month. On the other hand, the Caixin PMI manufacturing survey is expected to drop to 50.6. It is worth noting that the NBS survey has a larger poll and focuses mostly on state-owned firms while the private Caixin survey covers mostly private and export-oriented firms.

Aussie would enjoy stronger data

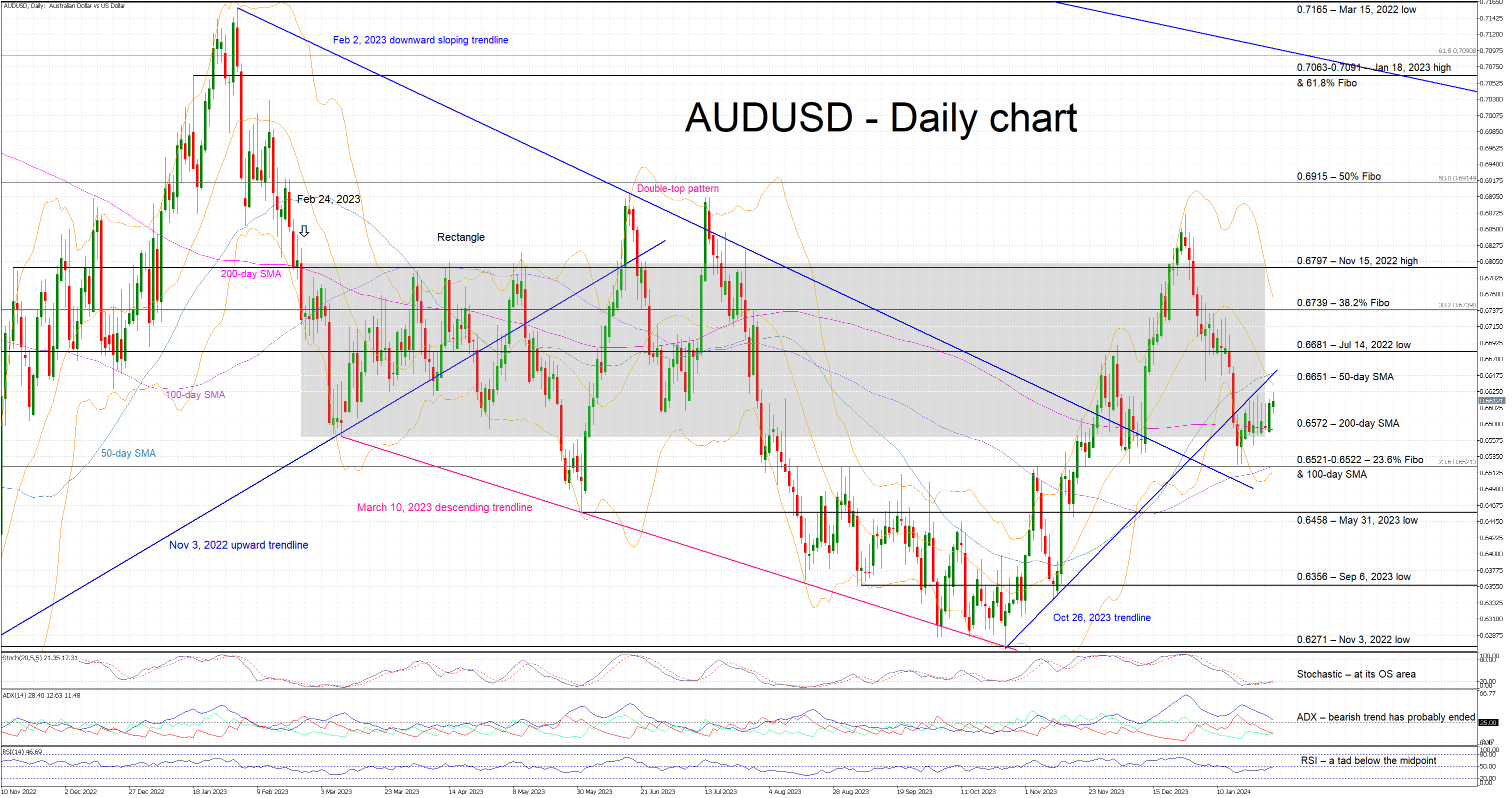

This week’s events could finally allow the aussie-US dollar pair to escape its recent range trading. It remains at the lower boundary of the rectangle that defined the price action during most of 2023 and it is hovering above its 200-day simple moving average. A strong set of data releases in both Australia and China could push aussie-dollar towards the 0.6651 level. On the flip side, a negative set of data, especially in China, could open the door for a protracted correction below the busy 0.6521-0.6522 area.