{kind=link}

U.S. Highlights

- The U.S. economy ended 2023 on a solid note, with GDP rising 3.3% quarter-over-quarter (annualized) – smashing expectations for a more moderate gain of 2%.

- The consumer remained a key factor underpinning last quarter’s strength, with spending accelerating sharply through the holiday shopping season.

- Inflation continued to drift lower in December, with the 12-month change on core PCE – the Fed’s preferred inflation measure – slipping below 3%.

Canadian Highlights

- The Bank of Canada held their policy rate at 5% this week, while making minor tweaks to their forecasts. Messaging accompanying the decision pointed to no change in rates for the time being.

- Markets have priced in a rate cut in June. Our own call sees rates beginning to move lower in the second quarter.

- The federal government announced a cap on international student visas this week. This will weigh on consumption and offer some relief to Canada’s rental market.

U.S. – The Final Approach

The latest data has shown the U.S. economy had all the markings of a soft landing as 2023 drew to a close. Economic growth held up better than expected, the labor market is coming back into better balance, and price pressures are quickly abating. Market pricing on the timing of the first Fed rate cut has seesawed between March and May in recent months, with March currently priced as a coin-toss. But with progress on the inflation front showing no signs of stalling, market sentiment remained in risk-on mode this week, with the S&P 500 edging up 1% for the week, reaching yet another all-time high. Shorter-term yields drifted a bit lower, leading to a further flattening in the yield curve. At the time of writing, the inversion of the 10Y-2Y spread had narrowed to just -20bps – well off the peak inversion of -110bps seen back in July.

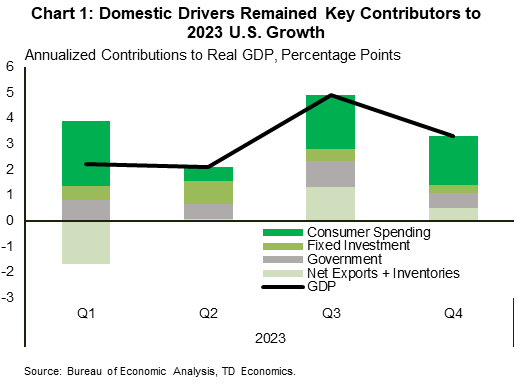

The Bureau of Economic Analysis’ advance estimate of fourth quarter real GDP came in at 3.3%, a downshift from Q3’s blistering 4.9%, but well above the consensus forecast calling for a more moderate gain of 2%. Economic resilience remained on full display, with the consumer, private investment, and government spending accounting for the lion’s share of last quarter’s gain (Chart 1). While the rearview mirror isn’t always the best guide to the road ahead, the solid end to last year provides a more favorable starting point heading into 2024.

This is especially true for the consumer. The monthly income and spend figures for December – released a day after the GDP report – showed consumer spending accelerated sharply through the holiday shopping season. This was happening even though the tailwinds from excess savings had slowed from the gale force gust felt at the beginning of the tightening cycle to just a gentle breeze by the end of last year. At the same time, 27 million student loan borrowers were faced with the harsh reality of having to restart regular loan repayments in October following the expiration of the three-year student loan moratorium. But neither of these factors appear to have phased the consumer, as a still sturdy labor market has continued to support meaningful gains in real income and help to sustain a healthy pace of consumer spending.

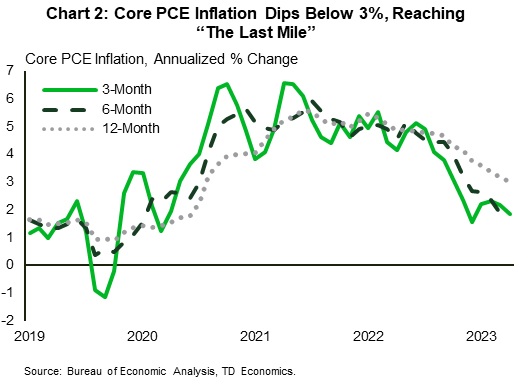

The puzzle has been on the inflation front. Despite the economy continuing to run well above its long-run potential through H2’2023, inflation has still made incredible progress. As of December, the 12-month rate of change on core PCE fell to 2.9%, while the annualized 3-and-6-month rates slipped to 1.5% and 1.9%, respectively (Chart 2). Falling goods prices and some cooling in non-housing services have both been the key contributors to the recent downward pressure on inflation.

From the Fed’s perspective, time (and the economic data) remain on their side. With the economy showing no signs of keeling over, and the labor market still relatively tight, policymakers can afford to be patient. Fed officials will want to see at least a few more ‘soft’ readings on inflation and a bit more easing in the labor market before pulling the trigger on rate cuts.

Canada – Feds, BoC Steal This Show This Week

Multigenerational highs in Canada’s population growth have strained the country’s social systems and inflamed the country’s housing crisis. In view of these challenges (and others), the federal government announced a cap on international students. The idea is that in the fall of this year, the number of student visas will be rolled back to 2022 levels, and some estimates suggest that this could lower the student intake by at least 200k spots over time. To put this figure in perspective, it would amount to roughly 20% of Canada’s massive population inflow in 2023.

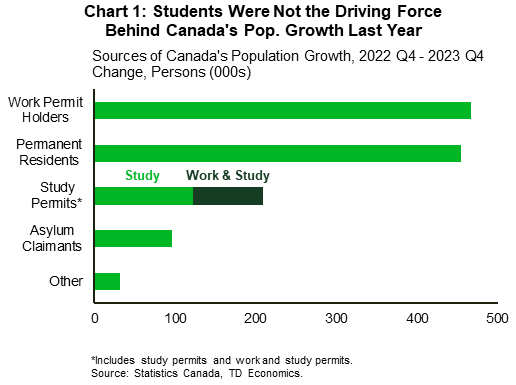

This will undoubtedly sap some steam from Canada’s frothy population growth. This weaker growth will then weigh on consumption and housing. On the latter, the policy should slow down rent growth relative to its prior trajectory. However, it’s tough to envision a large-scale cool down in rents this year. Note that even if this policy begins to weigh on population growth this year, it was newcomers with work permits (not students) who were largely responsible for Canada’s population surge last year (Chart 1). What’s more, immigration levels (untouched by the policy) remain robust.

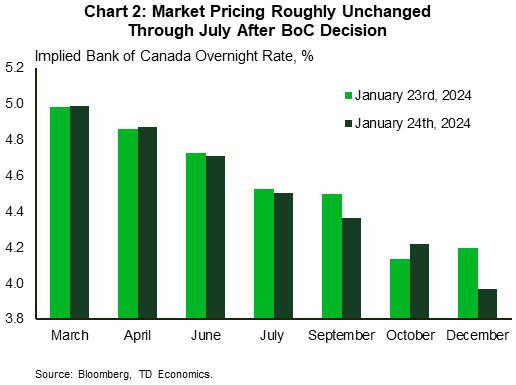

The even bigger news this week for financial markets was the Bank of Canada’s interest rate decision. There are a handful of important takeaways. First, the Bank of Canada left their policy rate on hold, as expected. Second, their inflation and economic growth forecasts were little changed from the prior report. Notably, the Bank still sees headline inflation falling to 2.4% by the end of this year and 2.1% by the final quarter of 2025. These projections match our own. However, we see the economy posting weaker growth in 2024 and 2025, with rising debt service costs keeping the pressure on Canada’s highly indebted households. Third, the statement accompanying the decision was a touch more dovish than October, and Governor Macklem’s opening remarks after the decision noted that no further tightening will be required if their forecast evolves as expected. Fourth, the Bank took great pains to acknowledge that shelter costs will be a “material headwind” against the return of inflation to its target. These costs do complicate the Bank’s inflation fight, as they are partly due to factors beyond the Bank’s control, and policymakers will seemingly not “look through” them when setting policy. Fifth, Governor Macklem acknowledged the broad range of inflation indicators that the Bank is looking at to get a sense of underlying inflation, even if the preferred measures are CPI-trim and CPI-median. This could offer the Bank some degree of optionality on how they frame the trend in inflation moving forward.

The Bank’s interest rate decision didn’t meaningfully sway the markets’ rate expectations, at least over the next few meetings (Chart 2). June remains the likeliest month for the first rate cut, in the mind of markets. Our own expectation is that policymakers will be in position to cut their policy rate sometime in the second quarter of this year.