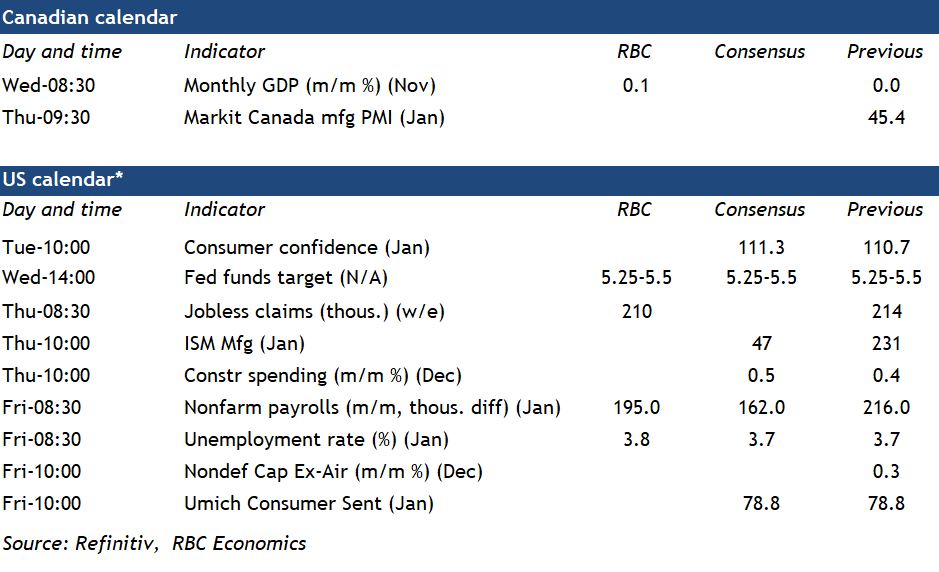

estimate released on Wednesday will probably tick higher for the first time in six months, but the economic backdrop to end 2023 still looks soft.){kind=link}

The November Canadian gross domestic product (GDP) estimate released on Wednesday will probably tick higher for the first time in six months, but the economic backdrop to end 2023 still looks soft.

We expect a 0.1% increase in GDP from October, which would be in line with Statistics Canada’s early estimate a month ago. These advance estimates have been prone to revisions. Still, data released since for November has largely been consistent with a tick higher in output. Retail sale volumes edged lower in November, but manufacturing and wholesale sale volumes rose (by 1.6% and 0.6% month-over-month, respectively) and oil production in Alberta increased.

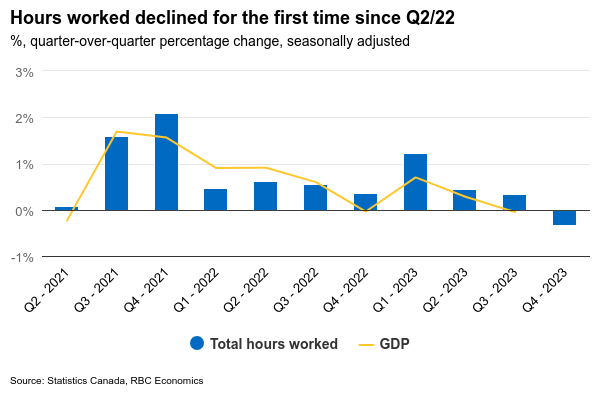

Still, other indicators have been softer. Employment continued to rise through the end of last year, but actual hours worked declined for the first time in Q4 since the early days of the pandemic (Q2/2020). The early estimate of December manufacturing sales was down 0.6%.

The economic growth data looks substantially weaker on a per-capita basis after controlling for still rapid population growth. We continue to expect a small decline in Q4 GDP once all the numbers have been counted, but even a small increase would leave output per person down for a sixth consecutive quarter.

The labour market also still looks substantially softer with the unemployment rate up 0.8 percentage points since spring 2023. The Bank of Canada has referenced the softer economic backdrop as the reason additional interest rate hikes this year are unlikely and we continue to expect a pivot to gradual cuts by mid-year.

Week ahead data watch

The U.S. Federal Reserve is widely expected to hold the fed funds target range unchanged for a fourth consecutive meeting on Wednesday. Attention will be focused on any hints on the potential timing of a pivot to cuts. Another round of strong GDP data in Q4 showed that the economy is still weathering higher interest rates better than expected. But slowing price growth is leaving the Fed with flexibility to hold the line on interest rates for now – and to respond with lower rates later this year (we expect before mid-year) once the economy starts to soften more significantly.

Next Friday, we will get the first U.S. jobs report for 2024. Payroll employment is likely up by 195K in January, slightly below the 216K in December. The unemployment rate should continue to edge up to 3.8% from 3.7% in December, reflecting some easing conditions in the labour market.