{kind=link}

Summary

It was a busy week for foreign central banks, with several offering their first monetary policy assessment of 2024. The Bank of Japan held monetary policy unchanged, but its announcement and updated economic forecasts kept it on track for an April rate hike, in our view. The Bank of Canada’s announcement was modestly dovish in tone, suggesting some risk that an initial rate cut could come earlier than our base case for monetary easing in June. The European Central Bank had offered hawkish guidance ahead of this week’s meeting, but its announcement was arguably more neutral in tone. Given downbeat economic trends and the ECB’s data dependence, our base case remains for an initial rate cut in April, although we acknowledge the risks are tilted toward a later move in June. Finally, the People’s Bank of China lowered its Reserve Requirement Ratio to provide long-term liquidity to the market. While that could offer some support to the economy, we still expect China’s GDP growth to be slower in 2024 than 2023.

Foreign Central Banks Kick Off 2024

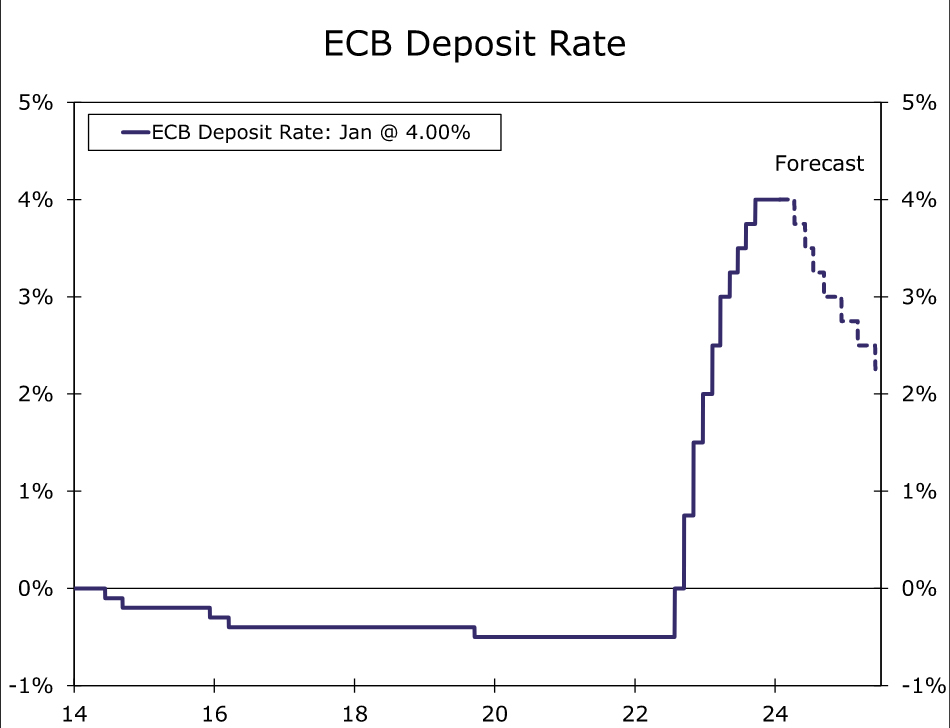

It was a busy week for foreign central banks, with several institutions making their first monetary policy announcements of this year, and offering insight to the potential paths of their respective monetary policy stances through 2024. The European Central Bank (ECB) monetary policy announcement was perhaps not quite as hawkish as expected. In the lead up to this meeting, ECB President Lagrade suggested a rate cut was likely by or in the summer, and some of the more hawkish policymakers suggested the summer or later. ECB policymakers have also indicated a desire to see early 2024 wage data before adjusting their monetary policy stance. However, considering this leadup, the ECB’s policy announcement was perhaps more neutral in tone. The ECB reiterated that it “considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution” toward returning inflation to its 2% medium-term target in a timely manner. The ECB also again highlighted a data-dependent approach to conducting monetary policy. On that front, the ECB said the declining trend in underlying inflation has continued, and that past interest rate increases continue to be “transmitted forcefully into financing conditions. Tight financing conditions are dampening demand, and this is helping to push down inflation.” While ECB policymakers have guided market participants toward summer rate cuts, their assessment on the Eurozone economy appears notably underwhelming. As a result some market participants, including ourselves, still see potential for ECB easing to come earlier, during the spring.

This dichotomy between the ECB’s policy guidance and its assessment of the economy was also apparent during ECB President Lagarde’s press conference. She said the consensus was that a rate cut debate was premature, and she stood by her comments on summer rate-cut timing. At the same time, she said data signal economic weakness in the near-term, that the December inflation rebound was less than expected and almost all underlying measures fell in December. She added that short-term inflation expectations gauges are down markedly, and did not over-emphasize the inflationary risks from the Red Sea crisis. Combining the policy guidance with the assessment of the economy, the upcoming data should still be key as to the exact timing of an initial ECB rate cut. If GDP growth stays soft, sentiment surveys remain in contraction territory and underlying inflation continues to improve, then the rate cut debate could intensify in March and April, and monetary easing in April (for now still our base case) remains possible. However, should activity or sentiment data show some resilience, or improving inflation trends get interrupted, the June meeting will come more clearly into focus as the most likely timing for initial ECB easing.

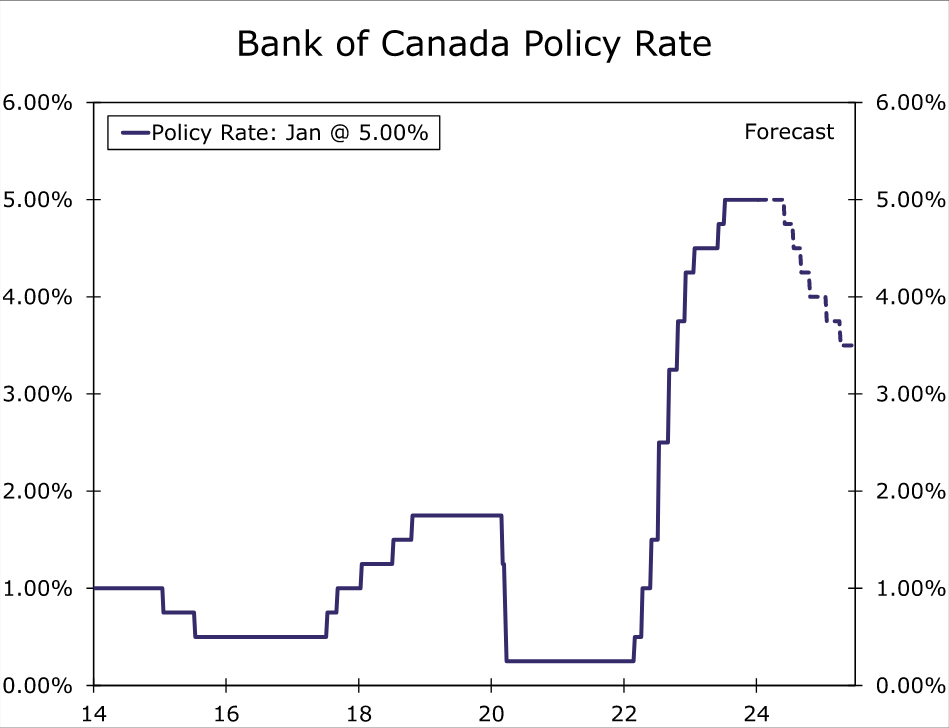

In its first announcement of 2024, the Bank of Canada (BoC) offered a moderately dovish shift in its monetary policy outlook. The BoC lowered its GDP growth forecasts, predicting zero growth in Q4-2023, and shaving its 2024 and 2025 GDP growth forecasts to 0.8% and 2.4% respectively. Against this backdrop, the BoC said the economy now looks to be operating in “modest excess supply”, suggesting some slack has opened up. BoC Governor Macklem also highlighted a shift in monetary policy focus, saying discussions are shifting from whether the policy rate is restrictive enough, to how long it needs to stay at the current level. Macklem did not completely rule out further rate hikes though, if new developments pushed inflation higher. As for the possible timing of rate cuts, the central bank said it is still concerned about risks to the inflation outlook, particularly the persistence in underlying inflation, and the BoC wants to see further and sustained easing in core inflation. In our view, Canada’s economy is already weak enough to elicit rate cuts from the central bank if wage and price inflation co-operate. With wage growth and core inflation still elevated for the time being, however, we maintain our call for an initial BoC rate cut in June. That said, we view the risks as clearly tilted to an earlier April move, a risk that could crystallize if wages or prices were to slow sharply in the next few months.

The Bank of Japan (BoJ) held monetary policy steady at its January announcement, keeping its policy rate at -0.10% and leaving its Yield Curve Control parameters untouched. In formal guidance that was unchanged, the BoJ said it will “patiently continue with monetary easing” and “will not hesitate to take additional easing measures if necessary.” That said, the central bank still appears to be laying the groundwork for a rate hike sometime during the earlier part of 2024, perhaps by April. In a notable shift in language, the BoJ said the certainty of achieving its economic projections has continued to gradually increase. BoJ Governor Ueda said the central bank will carefully assess data, including the spring wage talks, to see if the virtuous cycle of wages and prices is strengthening. The broader view on those spring wage talks appears to be constructive. In a recent Bloomberg survey, for example, some 94% of economists anticipated that the 2024 spring wage talks would result in an average wage increase that either matched, or was higher, that the average 3.6% wage increase achieved in 2023. Ueda also highlighted that more data will be available in April than March, and that a policy decision can be made even ahead of wage details for all small firms being available. Finally, the BoJ raised its forecast for medium-term (FY 2025) core inflation slightly to 1.8%, from 1.7% previously. Overall, we view BoJ policymakers’ assessment of the economy and inflation as encouraging enough to keep our call for a 10 bps policy rate hike to 0.00% in April on track.

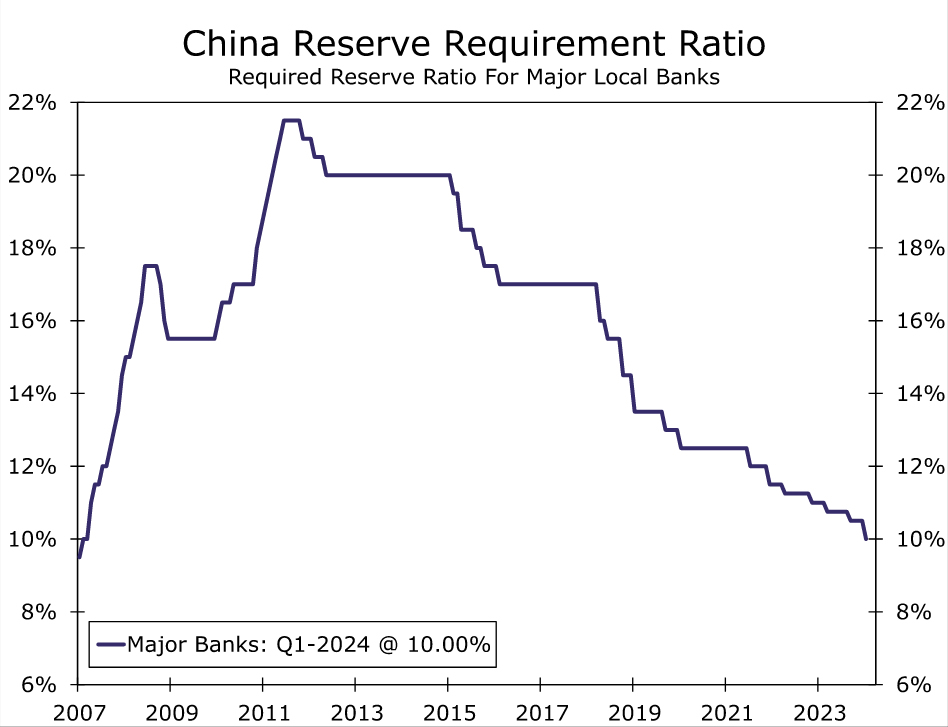

Finally, the People’s Bank of China (PBoC) announced a reduction in its Reserve Requirement Ratio (RRR) to ease domestic liquidity conditions. Effective from 5 February, the RRR will be lowered by 0.50 percentage points, reducing that ratio to 10.00% for major banks. The move will provide around 1 trillion yuan in long-term liquidity to the market, according the PBoC Governor. Still, these policy moves come in the context of weak domestic demand, disinflation and deleveraging and, as a result, we still anticipate a moderate slowdown in China’s GDP in 2024.