{kind=link}

- US will release GDP growth data at 13:30 GMT on Thursday

- An upside surprise seems more likely than a disappointment

- Dollar could benefit from a beat, as Fed cut bets are unwound

Dollar comes back to life

The US dollar started the new year on a strong note. A series of economic indicators have reaffirmed the resilience of the US economy lately, forcing traders to reconsider how quickly and how deep the Fed will cut interest rates this year.

Investors now see just a 45% probability that the Fed will cut rates in March, down from nearly 90% last month. This rethink follows the latest prints on inflation and retail sales, which came in stronger than anticipated, challenging the notion that the US economy is losing steam.

With the labor market also remaining in good shape, there doesn’t seem to be any urgency to slash rates immediately. Several Fed officials have argued the same point lately, stressing that markets have gone overboard with pricing in such heavy rate cuts, and that the actual pace of rate reductions will likely be slower than what traders expect.

An upside GDP surprise?

With the prospect of a rate cut in March now priced almost like a coin toss, the upcoming GDP stats will be crucial in tipping the scales, driving the dollar accordingly. Economists expect the US economy to have grown at an annualized pace of 1.8% during the final quarter of 2023, driven by heavy government spending and solid consumption.

As for any surprises, a stronger-than-expected GDP print seems more likely than a disappointment. This is mostly because of the Atlanta Fed GDPNow model, which currently estimates growth at 2.4%, significantly higher than the official forecast.

This model has a solid track record in terms of predicting actual GDP numbers, and if it proves accurate this time as well, the dollar would likely benefit as investors continue to unwind bets of rapid Fed rate cuts.

Looking at the charts, euro/dollar has been in a steady decline so far this year. Another round of encouraging US data could add fuel to this selloff, pushing the pair down towards its recent low of 1.0840, a region that also encapsulates the 200-day simple moving average.

On the flipside, a disappointing GDP reading would likely propel euro/dollar higher, with the 1.1000 zone likely to act as the first major barrier to any advances.

Beyond the GDP data, another important release this week will be the latest core PCE price index on Friday.

Can the dollar keep rising?

All told, the outlook for the dollar still appears quite bright. The US economy is in much better shape than other major regions such as the Eurozone, which might already be in a minor technical recession.

With economic growth differentials favoring the United States, there’s a clear risk that the Fed will cut interest rates at a slower pace than the ECB will during this cycle, keeping the dollar supported. Historically speaking, the dollar often thrives in late-cycle environments, especially if the US economy is healthier than the rest of the world.

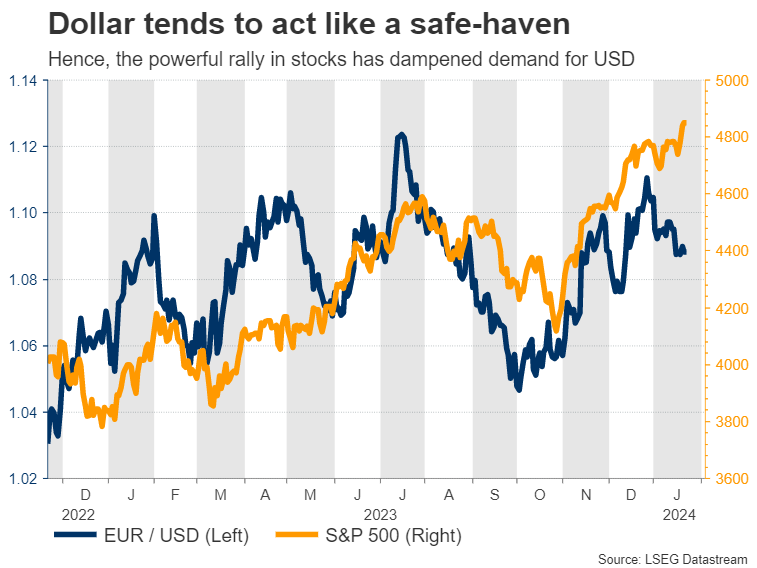

Finally, it’s worth noting that the powerful rally in stock markets has dampened demand for safe haven instruments like the dollar in recent months. If this rally loses some steam and valuations compress now that investors have started to scale back rate cut bets, it could be another element that helps the dollar advance.