{kind=link}

U.S. Highlights

- Higher than expected retail sales in December suggests that consumer spending remained resilient to end the year.

- Several Fed governors sought to push back against market expectations for swift and significant rate cuts.

- The housing market ended 2023 on a sour note, with both new home construction and existing home sales falling in December.

Canadian Highlights

- Bank of Canada (BoC) rate cut odds took a hit this week as stronger than expected data caused a selloff in bond markets.

- Inflation data got a lot of attention, as the BoC’s core measures moved higher in December – not the kind of move the BoC was looking for.

- Housing data also surprised higher. With sales rebounding, the average home price rose for the first time since last spring.

U.S. – A Resilient Consumer Dims Hopes for an Early Rate Cut

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

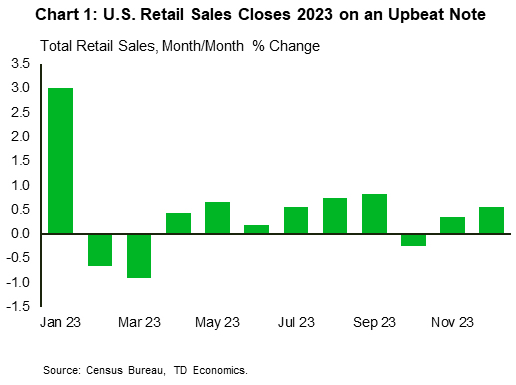

Retail sales rose 0.6% month-on-month in December, following a 0.3% gain in November (Chart 1). The breadth of the increase was also noteworthy with 9 out of the 13 categories recording gains. The “control group” which factors into the calculation of personal consumption expenditure rose an even more impressive 0.8% on the month. The stellar number suggests that consumer spending grew at a healthy clip of around 2.5% (annualized) in Q4.

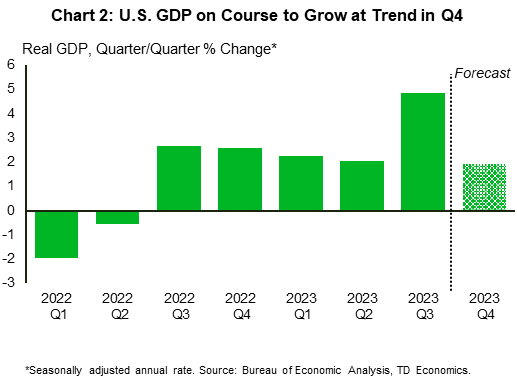

The stronger than expected retail sales report has resulted in upward revisions to expectations of Q4 GDP growth. After the report, the Atlanta Fed’s GDPNow growth estimate rose to 2.4% (from 2.2%), while our own estimate currently sits at 1.9%. (Chart 2). We won’t have to wait long to know for sure though, as the BEA is set to release the advance estimate of Q4 GDP next Thursday. Given expectations for the print to be relatively strong, there is even less pressure on the Fed to entertain rate cuts over the coming months.

The slew of Fed speakers making the rounds this week were quick to reinforce that point. “With economic activity and labor markets in good shape and inflation coming down gradually” Governor Waller sees “no reason to move as quickly or cut as rapidly as in the past.” He used terms such as “carefully calibrated and not rushed” and “lowered methodically and carefully” to push back against market expectations of sizeable cuts this year. Atlanta Fed President Bostic was on a similar page. He noted that rates could be cut earlier than Q3, “but the evidence would need to be convincing.” What’s more, he urged caution given the current uncertain environment (domestic budget battles, global conflict, elections etc.), which could have unpredictable economic impacts and re-ignite inflation pressures.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Ultimately, the timing and pace of rate cuts will depend on the strength of economic growth and inflationary pressures. This week’s data indicate that economic conditions are currently resilient. Last week’s CPI print shows there is still work to be done on the inflation front. The combination means that a policy pivot to rate cuts is unlikely to be top of mind for Fed officials just yet.

Canada – The Inflation Thorn Remains in the Side of the BoC

Bank of Canada (BoC) rate cut odds took a hit this week. Strong inflation readings alongside a surprising improvement in housing activity pushed BoC rate cut expectations from March to April. This forced a bond market selloff, as both the Canadian 2-year and 10-year yields shot-up more than 30 basis points ahead of next week’s BoC decision.

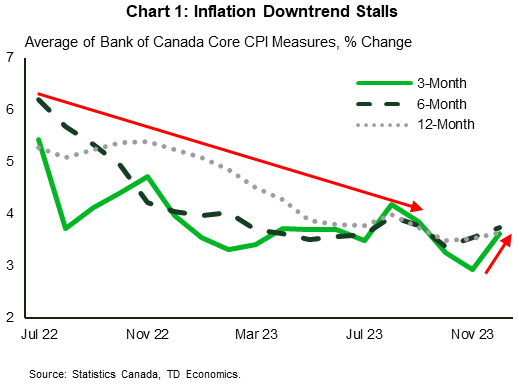

The December release of Canadian CPI got a lot of attention. Expectations were for annual inflation to move higher on base year effects (the impact of lower prices in December 2022). While this happened as expected, what took everyone by surprise was the shift higher in core inflation rates. The average of the BoC’s core measures moved up a tenth, to 3.7% year-on-year (y/y). While this doesn’t seem like much, the timelier three-month annualized rate rose from 2.9% to 3.6% (Chart 1). That was not the kind of move the BoC was looking for.

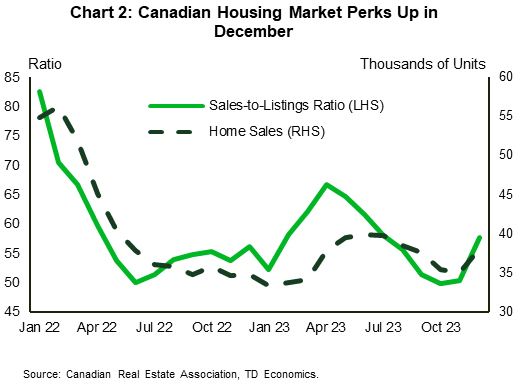

Housing data also surprised higher. Maybe it was the warmer December weather, maybe the hope that the BoC was gearing up to cut rates. Either way, home sales jumped nearly 9% month-on-month. This boost alongside a sizable drop in listings pushed market balance above its long-term average and closer to buyers’ territory (Chart 2). This caused the average house price to rise for the first time since the BoC re-started rate hikes in June 2023.

Canadians have also been actively filling shopping malls. Retail sales data for November pointed to more consumers buying clothing, shoes, and jewelry – all the stuff that was in demand during the holiday shopping season. And while overall sales were held down by less spending at food retailers, it looks like December spending will more than offset any of that weakness.

This week’s flow of data seems to be moving counter to the recent trend. Over the last 9 months, we had seen consumers pulling back as high mortgage rates reduced spending power. At the same time, the number of net-new job gains has come to a standstill. No surprise that the BoC’s newly released surveys of consumer and business sentiment continued to weaken. Importantly, nearly 70% of consumers said they have already cut spending in the face of higher rates. Businesses echoed this sentiment, with many having reported that they are seeing outright sales declines for their products. This caused ‘economic uncertainty’ to become the top concern for firms in 2024.

Where does this leave the BoC for its meeting next week? Given the upturn in data, there is little impetus for the BoC to flip the script. It will maintain its cautiousness, focusing on how the job isn’t done yet. That said, it can also hang its hat on how forward-looking indicators are pointing to greater weakness in the months ahead. Importantly, markets believe that this weakness will soon come through in the data. This belief has maintained expectations that the BoC will begin cutting rates by the spring, something that the Bank may try to lean against next week.