{kind=link}

- The 2024 market theme remains for several rate cuts from most central banks

- Fed is seen cutting rates six times despite the November Presidential election

- ECB and the BoC to cut first; RBA the last one to join the club

- BoJ is finally seen hiking for the first time since 2007 – will it prove wishful thinking?

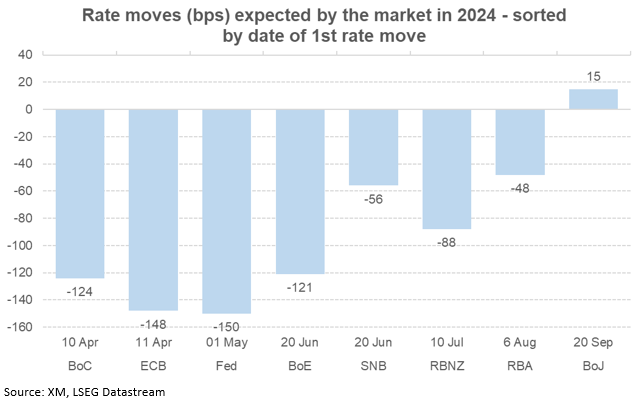

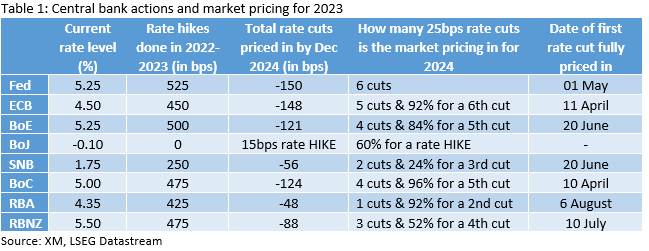

Last year ended with clear feelings from the market’s side about the direction of rates in 2024: rate cuts across the board, apart from the Bank of Japan. Two weeks into the new year and the market is trying to digest an already busy calendar. Inflation data from both the US and the euro area, and the US labour market have already made an impact on expectations. Therefore, what is currently priced in?

ECB and Fed: 6 rate cuts?

The two most important central banks appear to be on similar paths. The ECB is expected to ease policy by 148 bps in 2024, a tad below the 150bps of Fed easing currently priced in. These market expectations do not align with the underlying economic sentiment as there seems a divergence between the strong growth recorded in the US, causing some Fed hawks to mention rate hikes lately, and the continued economic weakness seen in the Euro area, as portrayed by the PMI surveys.

One of the reasons for the current rate expectations is probably the contradictory rhetoric at the last central bank meetings in December 2023. More specifically, the Fed’s Powell dovish rhetoric, which was not entirely evident at the recent minutes, and President Lagarde’s hawkish stance have allowed the market to forecast any almost equal number of rate cuts.

BoE and BoC: dangerously close to 5 rates cuts

Moving down the list, the Bank of England and the Bank of Canada are fighting for the third spot with the most rate cuts currently being priced in. Currently, the BoC “wins” with 124bps of rate cuts expected by the December 19, 2024 gathering. While traditionally seen following very closely the Fed’s movements, in 2024 it is expected to announce its first 25 bps easing at the April 10 meeting, ahead of the Fed. This sounds a bit extreme considering the current inflation rate and the possibly stronger oil performance during 2024 on the back of OPEC’s disagreements. Of course, there are a few dark horses, for example the housing sector, so the BoC is expected to walk on a tightrope.

Not far below, with 121bps of rate cuts currently priced in, comes the BoE. The market is expecting a slower start as the first 25bps rate cut is currently being priced in by June 20, 2024, around 2.5 months after the ECB’s expected first rate move. The higher inflation rate, the pre-election shenanigans and the expected accommodative fiscal stance, which should support consumer spending, appear to affect the market expectations.

RBNZ: almost 4 rate cuts

Not far from the major central banks, the RBNZ is seen cutting rates by 88bps in 2024, unravelling only a small part of its recent tightening cycle. July is currently being touted as the likely month for the first rate cut despite the fact the RBNZ remains hawkish on the back of the latest OCR projections pointing to another rate hike in 2024.

RBA and SNB: 2 rate cuts?

The SNB and the RBA are seen following the rest of the pack with around two rate hikes priced in for 2024. The former is expected to announce a 25bps rate cut in June, mostly to counter further strengthening of its already expensive Swiss franc, especially against the euro. On the other hand, the RBA was the last one to hike in 2023 and it is thus expected to be the last one to announce a rate cut in August 2024. China’s expected growth pick-up could delay even more the start of the easing cycle, but eventually the RBA will probably be forced to follow this path.

BoJ: to finally hike in 2024?

The Bank of Japan is once again the outlier. The market expects that 2024 will be marked by a return to monetary policy normality for the BoJ. This could be wishful thinking by the market or simply a repeat of last year’s modest hiking expectations, which were not confirmed as the BoJ only tweaked its yield curve control program. A total of 15bps of rate hikes is currently priced in by the end of 2024 but even a small 10bps rate move, seen in September 2024, holds significant signaling value for the BoJ.