{kind=link}

Summary

- The U.K. economic environment remains challenging, with Q3 GDP contracting slightly and the fourth quarter starting on a subdued note. Even with some improvement in consumer fundamentals and sentiment surveys, we believe a mild technical recession for the U.K. remains more likely than not.

- Stubborn persistence in U.K. price and wage inflation has started to break, with both prices and wages surprising to the downside in recent months. While these are clearly welcome developments, wage inflation is likely still too high to sustainably achieve the central bank’s 2% inflation target, and it’s not yet clear how long the more muted pace of price increases will persist.

- The U.K. growth and inflation slowdown suggests the risks are tilted towards an earlier rate cut than our current base case of the August meeting. An initial rate cut could perhaps come in June, possibly May.

- Nonetheless, we still think the risks are tilted towards more gradual easing than reflected in current market pricing, which already sees around a 75% chance of an initial rate cut by the time of the May meeting. Against this backdrop, we think U.K. bond yields could drift higher from current levels. It could also mean moderate gains in the pound against the U.S. dollar as 2024 progresses, especially if—as we expect—the U.S. economy moderates and the Fed eases monetary policy as well.

U.K. Economy Flirting With Recession

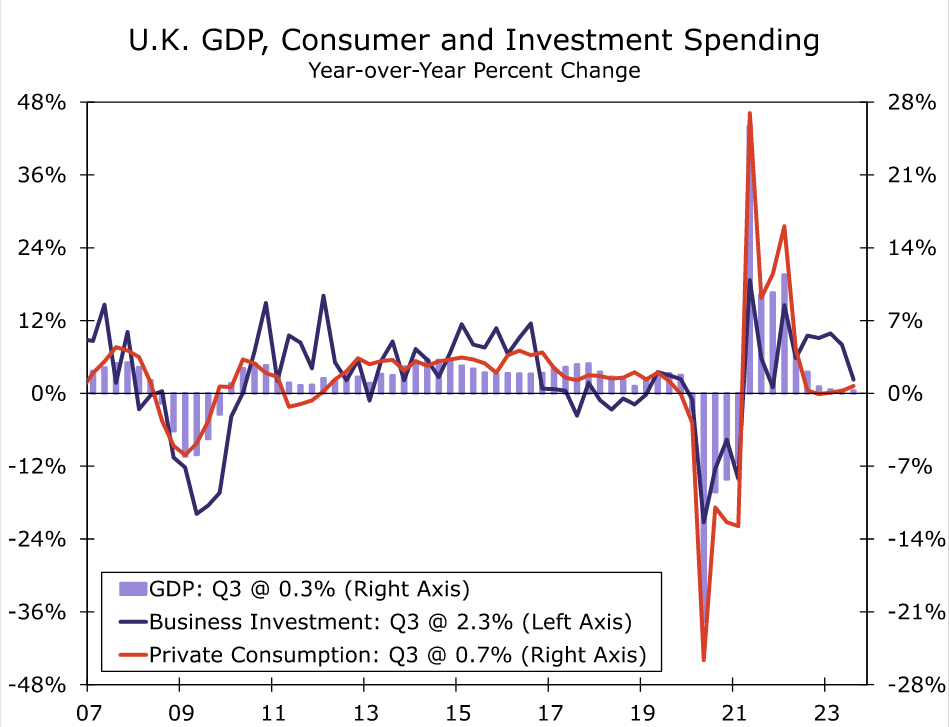

Recent data have highlighted the challenging environment still facing the U.K economy. After avoiding the threat of contraction over the past few quarters, revised data for Q3-2023 GDP showed the economy finally shrank by 0.1% quarter-over-quarter, compared to the previously reported flat outcome. The downward revision was due in part to consumer spending which fell 0.5%, a larger than initially reported decline, while exports were revised to show a modest fall in Q3. Finally, with downward revisions also evident in prior quarters, Q3 GDP rose just 0.3% year-over-year, down from an initially reported 0.6% increase.

The final quarter of 2023 started on an equally soft footing. For October, U.K. GDP fell a larger-than-forecast 0.3% month-over-month, as services activity fell 0.2% and industrial output fell 0.8%. While unusually wet weather likely crimped activity in some sectors, the level of October GDP was still 0.1% below its Q3 average. That suggests the U.K. is still dangerously close to a (mild) technical recession—that is, two consecutive quarters of negative GDP growth.

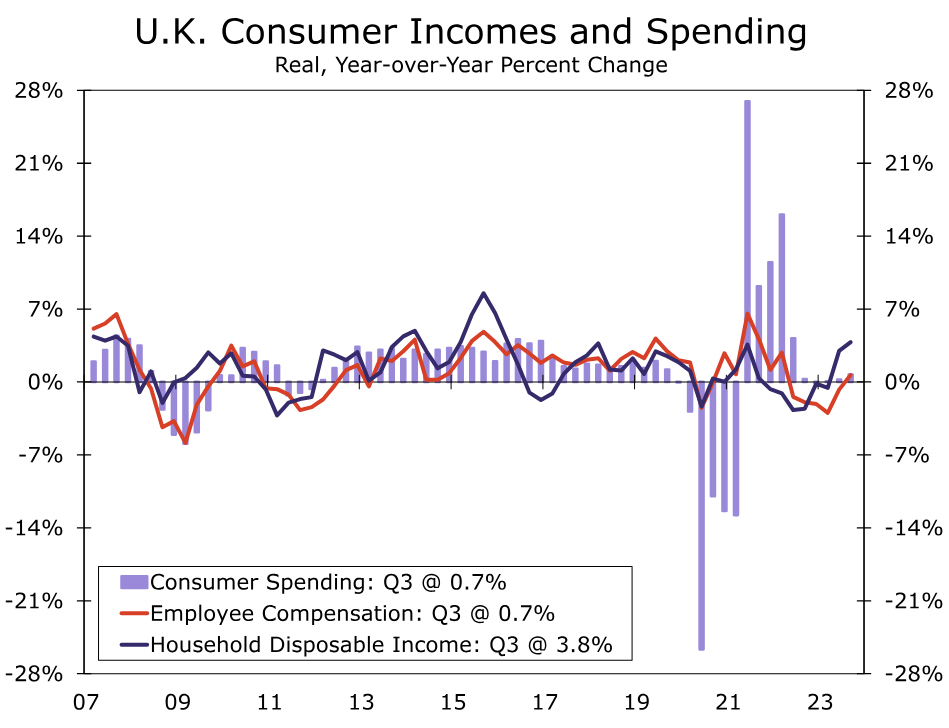

While a technical recession is possible and, indeed, perhaps more likely than not, such a downturn is not yet inevitable. Consumer fundamentals, while mixed, hint that the worst of the U.K consumer slowdown may be behind us. For the third quarter the rise in nominal household incomes outpaced the increase in prices, meaning that Q3 real household disposable income rose 0.4% quarter-over-quarter and is now up 3.8% year-over-year. Combined with subdued consumer spending, that also led to an increase in the household savings rate to 10.1% of disposable income in Q3. The savings rate is up from 9.5% in Q2, and well above the levels that prevailed prior to the pandemic. On a less encouraging note, and something of an offset to these improving fundamentals, the Bank of England’s interest rate hikes are increasingly flowing through to household budgets and cash flows. For Q3-2023, interest costs represented 5.5% of household income, around four times the1.4% of income as recently as Q3-2021. Still, considering the improving trends in real incomes and household savings, further declines in U.K. consumer spending may be limited, even given the backdrop of sharply higher interest rates over the past several quarters.

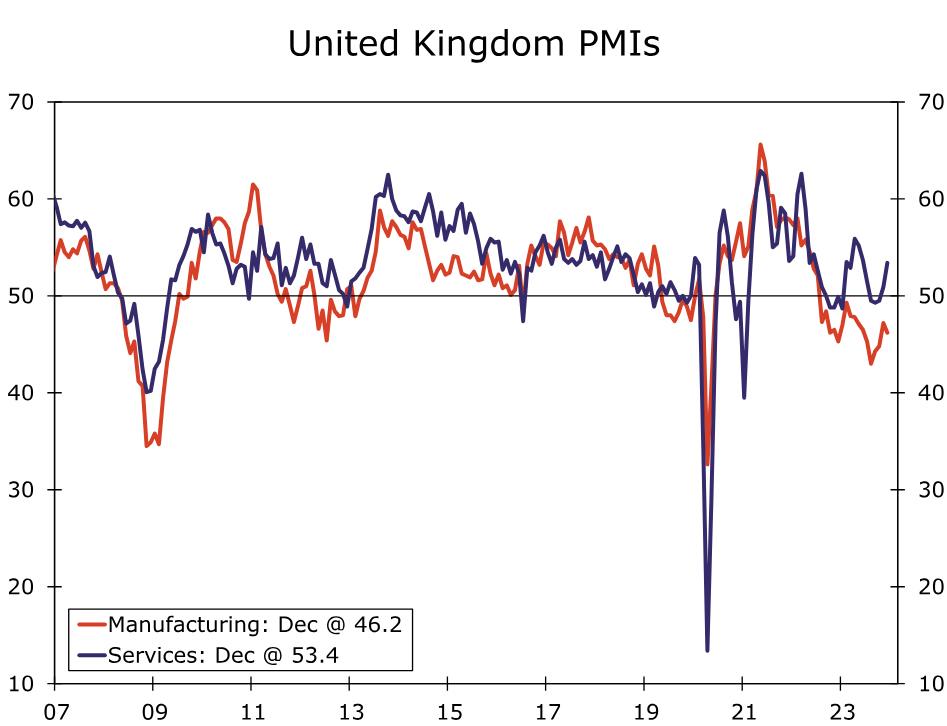

Sentiment surveys also offer hope that the U.K. economy could end the fourth quarter on a better note than it started. The U.K. manufacturing PMI slipped to 46.2 in December, and has been contraction territory since mid-2022. However, for the more economically dominant service sector, the services PMI has improved in recent months. The U.K. services PMI rose to 53.4 in December, a level consistent with moderate expansion. Overall, recent economic indicators are mixed, and we still lean towards a mild U.K. recession. But regardless of whether that recession occurs, our outlook for the U.K. economy is decidedly subpar. Our base case forecast is for U.K. GDP growth of 0.5% in 2023 and 0.1% for 2024, even if improving sentiment surveys hint at modest upside risk to the 2024 outlook.

U.K. Inflation Fever Is Breaking

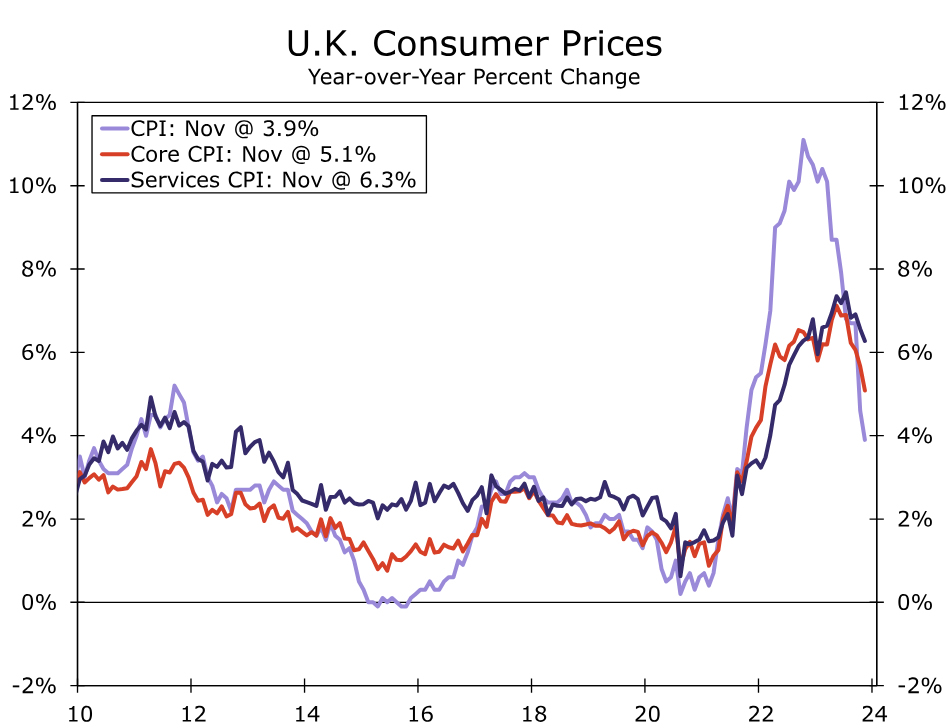

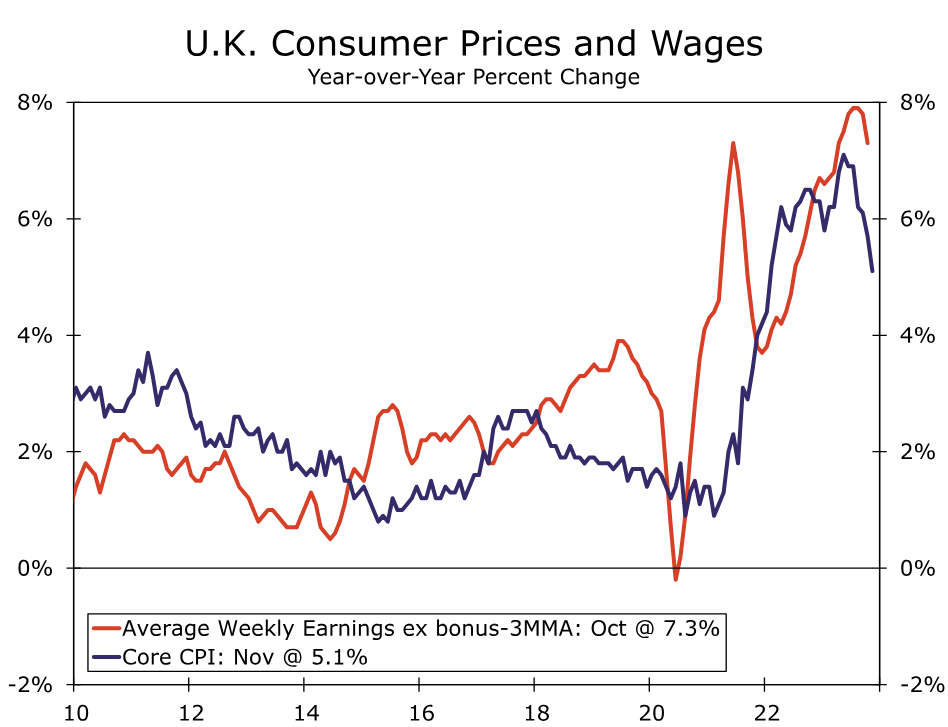

Just as U.K. economic growth has apparently come under increasing pressure, a more welcome development has been a significant improvement in U.K. inflation trends. U.K. price inflation and wage inflation trends have been stubbornly elevated for an extended period, and more so than for peer economies such as the Eurozone and United States. In recent months, however, the U.K. has started to enjoy favorable surprises on the price and wage front, at least as it pertains in returning CPI inflation towards its 2% inflation target. For November, U.K. headline inflation slowed more than forecast to 3.9% year-over-year, the slowest pace since late 2021. U.K. core inflation and services inflation similarly surprised to the downside, slowing to 5.1% and 6.3% respectively. In fact, we estimate that on a three-month annualized basis the U.K. core CPI has slowed below a 2% pace, although it is not yet clear that muted rate of price increase will continue.

In addition, stubbornly persistent wage growth has also shown some signs of easing in recent months. In particular, growth in average weekly earnings slowed more than expected to 7.2% year-over-year for the three months to October, while growth in average weekly earnings excluding bonuses slowed to 7.3% for the same period. While that slower wage growth is clearly a welcome development from an inflation-fighting perspective, for now the pace of wage growth is probably still at a level that is inconsistent with CPI inflation returning to and staying at the 2% target over a long term horizon.

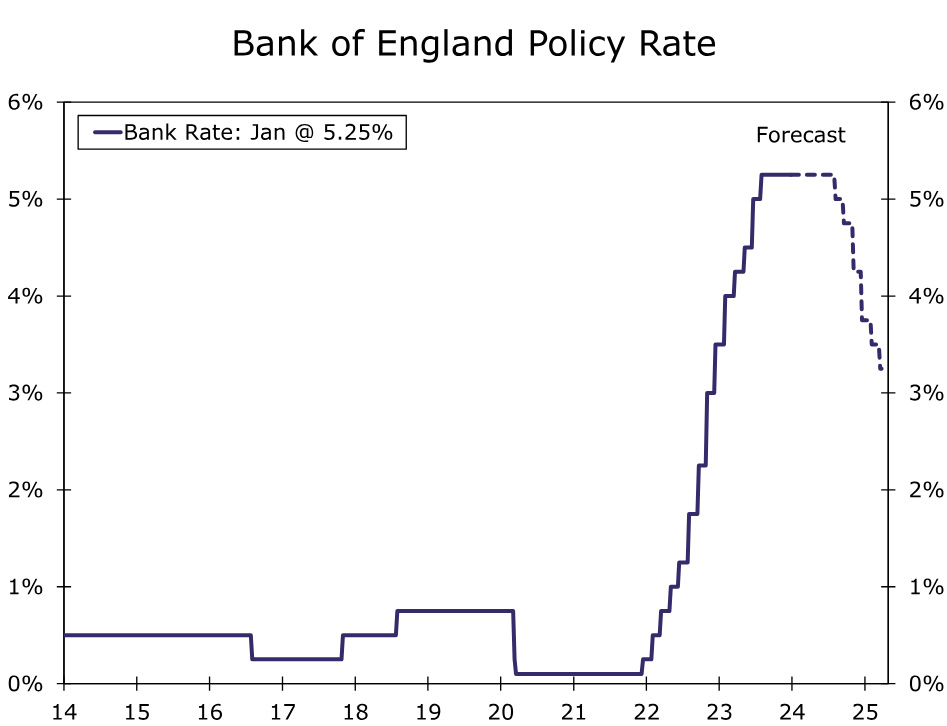

Before the most recent slowing and in U.K. growth and inflation, and amid a backdrop of hawkish comments from Bank of England (BoE) policymakers who had pledged to keep interest rates “higher for longer”, we took the opportunity to adjust our BoE monetary policy outlook, anticipating a later initial rate cut in August. That timing adjustment now appears to be somewhat inopportune, and the latest deceleration in the U.K. economy could still elicit earlier rather than later Bank of England monetary easing.

Nonetheless, the outlook remains quite uncertain at this point. As we highlighted above, it is not clear how long the recent muted pace of price increases will last, and we still view the current level of wage inflation as inconsistent with achieving the 2% inflation target on a sustainable basis, suggesting that even with the softening in U.K. data, BoE rate cuts are not imminent. That is, BoE rate cuts could occur earlier than our base case of the August meeting, but not much earlier—perhaps June, and certainly no earlier than May. The BoE’s monetary policy announcement on 1 February, which will include updated policy guidance and economic projections in the accompanying Inflation Report, should provide further clarity into the outlook for U.K. monetary policy. That is, whether an initial August rate cut still seems likely, or a June or May cut seem more probable.

Even if the outlook is not entirely certain, we still believe the risks are tilted towards more gradual easing than market participants currently expect. At this time a May BoE rate cut is already 75% priced in by market participants. While we think an initial cut in May is possible, we also think initial moves in June or August also remain in play. The risk of more gradual Bank of England easing than currently expected by market participants could see U.K. bond yields drift higher from current levels. Higher bond yields and gradual easing could also see moderate gains in the pound against the U.S. dollar as 2024 progresses, especially if—as we expect—the U.S. economy moderates and the Fed eases monetary policy as well.