{kind=link}

- NFP report and Eurozone CPI will be the week’s focal point on Friday

- FOMC minutes and ISM PMIs will also be crucial for the US dollar

- Canadian employment and Chinese PMIs might attract attention too

Rate cut bets in overdrive

It’s been one big rollercoaster ride for the US dollar in 2023, as hopes of a Fed pivot were repeatedly dented by surprisingly strong economic data, which more often than not, has come from the robust performance of the American labour market. But traders seem surer this time that a pivot is just around the corner, as Fed chief Powell himself has dropped subtle hints about it.

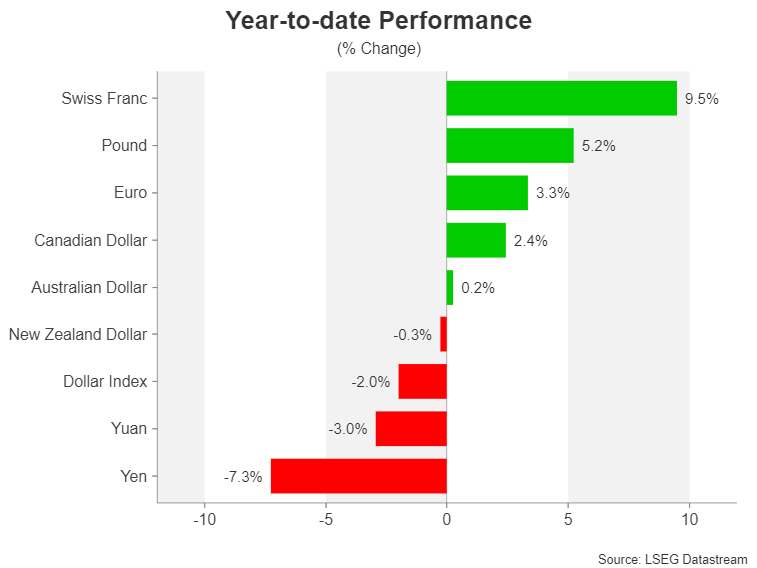

Thus, despite a powerful rebound during the summer and autumn, the greenback looks set to finish the year with losses of almost 3% against a basket of currencies. That rally was driven by a surge in Treasury yields, which have since been tarnished by heightened expectations of aggressive rate cuts over the coming year.

Cumulative rate cut odds for 2024 are fast approaching 160 basis points. This seems excessive when considering that the US economy is not in recession and Fed officials are only predicting about three 25-bps cuts. The minutes of the December meeting that produced those forecasts are due on Wednesday and FOMC members might attempt to use the publication to reinforce their view of only modest policy easing over the next couple of years.

A not too cold, not too hot jobs report

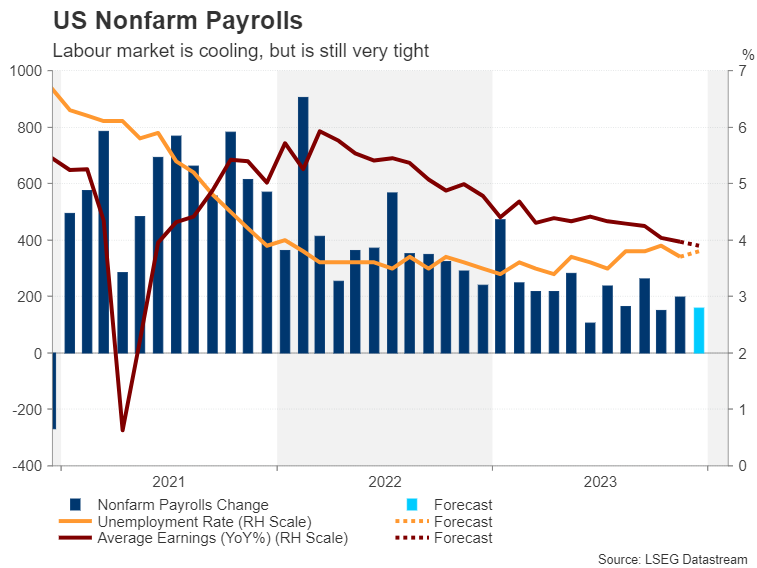

Another clue on the rate path will be policymakers’ outlook on the jobs market as they’ve recently indicated that as inflation comes down, their focus on the Fed’s other mandate – employment – will increase.

This might explain Powell’s lack of caution in being eager to steer policy towards easing on fear that holding rates at restrictive levels for too long might push up the unemployment rate. However, it’s been so far so good as far as the labour market is concerned. Jobs growth has slowed but companies aren’t laying off staff in big numbers, allowing wages to rise at a moderate pace.

Analysts don’t expect this picture to have altered much in December. Nonfarm payrolls are projected to rise by 158k, down from 199k in November, while the jobless rate is forecast to tick up slightly to 3.8%. Average earnings aren’t anticipated to rock the boat either, with the month-on-month rate expected at 0.3% and the year-on-year figure at 3.9% versus 4.0% previously.

Will there be a rude awakening for the markets?

Given investors’ strong conviction that the Fed will soon start slashing rates, a small beat or miss in the headline print is unlikely to generate anything more than a kneejerk reaction in the dollar. A very disappointing report isn’t very probable as weekly jobless claims have been quite low during the month. So if there will be a shock, it will be from an unexpectedly hot report.

The dollar could jump higher along with yields, while Wall Street could succumb to panic selling from investors scaling back their rate cut bets on the back of upbeat NFP readings. But in the event that the jobs data fails to provide any fresh direction, investors will probably turn to the other releases of the week.

These will include the ISM manufacturing and non-manufacturing PMIs, due on Wednesday and Friday, respectively, the JOLTS job openings on Wednesday, Challenger layoffs on Thursday, and factory orders on Friday.

Some risks ahead for the loonie and aussie

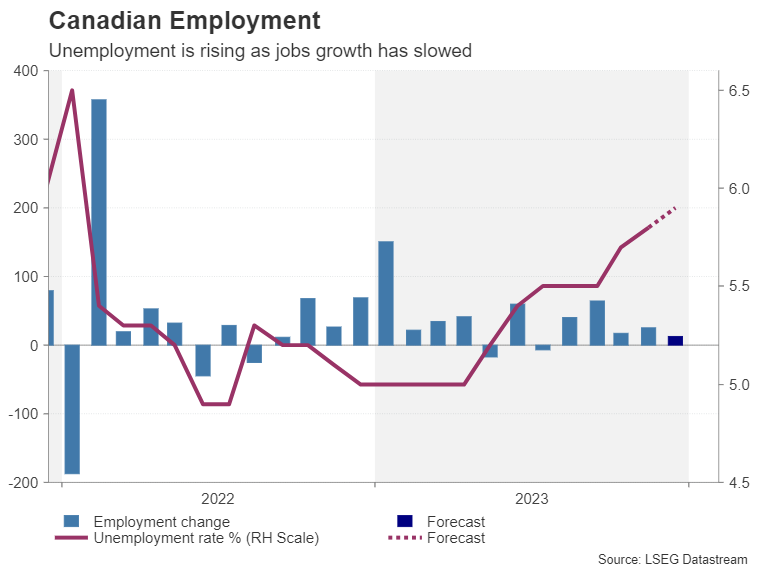

Across the border in Canada, the loonie will be keeping tabs on the domestic labour market as rate cut bets for the Bank of Canada have also been ratcheted up lately. The Canadian dollar is on track to have gained about 2.5% against its US counterpart in 2023, faring somewhat better than the other commodity-linked currencies, the Australian and New Zealand dollars. Less exposure to China and a more unquestionably hawkish stance by the BoC have contributed to its relative outperformance versus the aussie and kiwi.

However, there’s a risk that 2024 might be more of a struggle for the loonie if stagnating economic growth forces the Bank of Canada to start lowering rates. The country’s unemployment rate has been steadily edging up since May and likely rose further in December to 5.9%, data on Friday is expected to show.

Although employment has been rising during this period, it hasn’t been able to keep pace with the growth in the number of jobseekers. It’s expected that the economy added just 13.2k jobs in December. Nevertheless, wage growth remains elevated at 5.0% so investors will be watching that figure too, as well as the latest Ivey PMI gauge on Friday.

PMI data will also be important for the Australian dollar as China’s two sets of releases are due next week. The official government survey is out on Sunday and the Caixin/S&P Global version will follow on Tuesday. Any slowdown in China’s manufacturing PMIs in December could hurt risk sentiment at the turn of the year, weighing on equities as well as the aussie.

Eurozone inflation could reverse decline

A currency that will probably take the middle spot in the 2023 FX league table is the euro. The single currency has had a few ups and downs of its own over the past year, but overall, it’s been propped up by a more hawkish-than-anticipated ECB. It’s likely, though, that in 2024, a weaker Eurozone economy will spur the European Central Bank to slash rates more than the Fed. Yet, with US yields falling faster than Eurozone ones, the euro has come out a winner from all the frenzy of rate cut speculation.

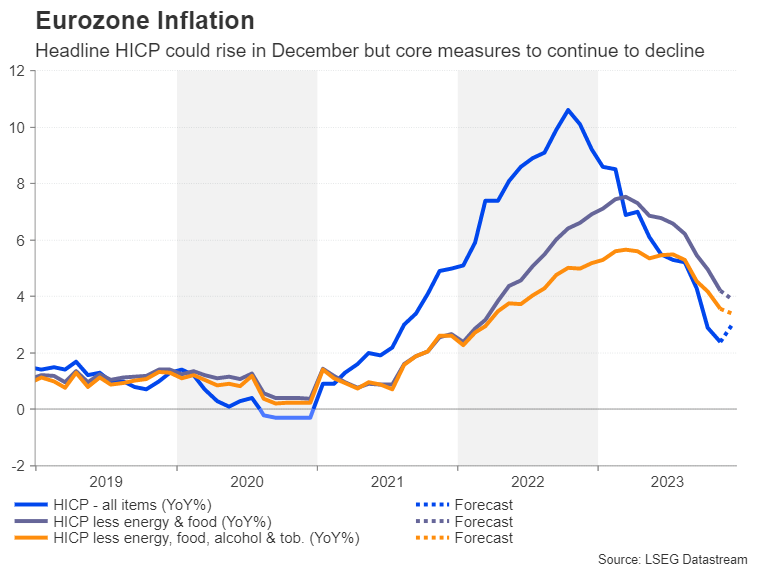

Unlike the Fed, the ECB is wary about sending any pivot signals before it can be sure that inflation is well and truly headed towards 2%. The flash CPI readings for December will probably justify this caution on Friday. Headline CPI is forecast to accelerate from 2.4% to 3.0% y/y in December, suggesting there’s still some way to go before inflation settles sustainably around the 2% target.

However, the forecasts for the underlying measures of inflation are more encouraging, with core CPI that excludes food and energy, as well as tobacco and alcohol prices, projected to decline from 3.6% to 3.4% y/y.

If that turns out to be the case, investors may well leave their rate cut wagers untampered, meaning there may not be any additional boost for the euro against the greenback from any pickup in headline inflation.