{kind=link}

- Despite heightened rate hike speculation, BoJ to likely stand pat in December

- No change is anticipated either in yield curve control

- But yen traders will be seeking fresh clues in Tuesday’s announcement

BoJ still to join the rate hike club

The Bank of Japan is the only major central bank that has not yet raised interest rates, as despite inflation running above its 2% target for the past one-and-a-half years, Japan has yet to be declared free of deflation.

Policymakers are keen to see domestically fuelled price pressures like wage growth replacing external drivers such as last year’s energy price shock to be convinced that the inflation rate can be sustained above 2%. Whilst there have been plenty of encouraging signals from the data, there’s yet to be anything conclusive to suggest that inflation has made a permanent comeback in Japan.

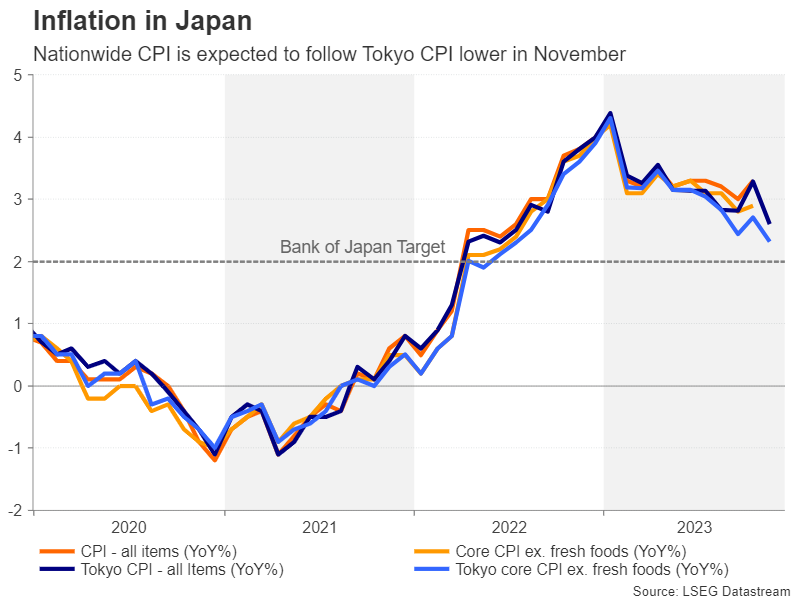

The consumer price index ticked up to 3.3% y/y in October but if the Tokyo CPI numbers, which are leading indicators, are to be believed, the nationwide readings due on Friday likely moderated in November. The GDP data is another one not going in the BoJ’s favour. The Japanese economy contracted more than expected in the third quarter, raising question marks about its strength just as the BoJ is considering exiting negative interest rates.

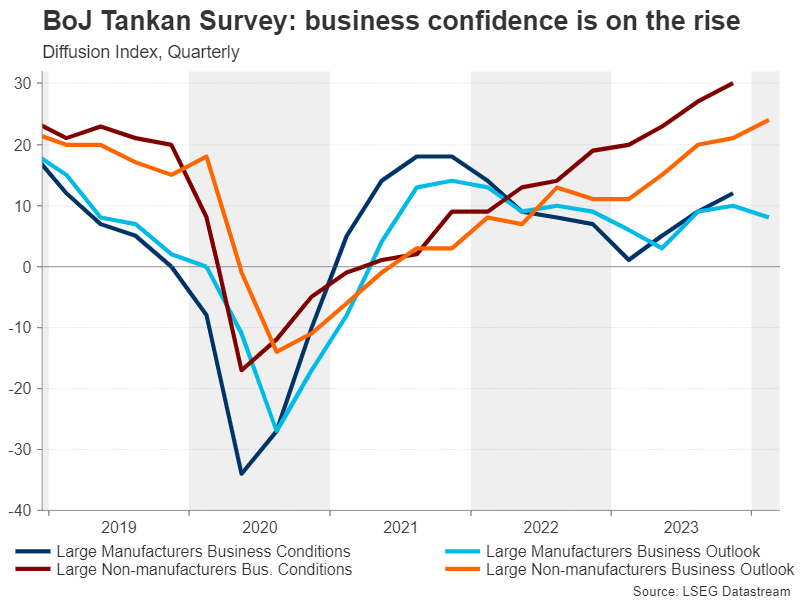

Consumers are spending less but businesses are upbeat

Much of the weakness is down to sluggish household spending. Consumption has fallen sharply in the past two quarters as household budgets have been squeezed by rising prices. It’s an entirely different story for corporate Japan, however, as businesses have been benefiting from the favourable exchange rate that’s seen the yen slump to levels last seen in 1990. Optimism among large Japanese firms has been going from strength to strength this year.

But the outlook is far from clear. The yen’s fortunes have started to change now that the Fed has opened the door to rate cuts and the BoJ is on the verge of scrapping negative rates. Moreover, growth in all the major economies is slowing, thus, this optimism may not last very long.

On the other hand, the Japanese government recently announced a large stimulus package aimed at easing the pain of high inflation on households, so a turnaround in consumer spending is possible in the coming months.

Waiting for the elusive wage acceleration

The muddied economic picture may complicate matters for policymakers, but ultimately, the BoJ will likely base its decision on whether to exit stimulus on what happens to wages. To this effect, next year’s spring wage negotiations will be crucial. Early signs of where the latest round of pay deals are headed are promising.

If the BoJ is satisfied with the outcome, there could be liftoff by April, even if all the other pieces of the jigsaw don’t quite fit properly. The Bank likely recognizes that this may be its best and only opportunity to end the highly unpopular policy of negative rates once and for all.

Will the BoJ give up control of the yield curve?

But what happens to yield curve control (YCC) policy is somewhat less straightforward. Although the BoJ significantly loosened its grip on the yield curve in October when it raised the upper bound of the 10-year yield target to 1.0%, it will probably not want to abandon YCC policy entirely so as to be able to prevent sudden moves in yields.

For investors, however, the immediate priority is the timing of any big policy shift. Some traders are speculating that the BoJ will hike rates as early as the December meeting, if not, in January. A 10-basis-point hike is not fully priced in until June so the consensus view seems to be that the BoJ will remain patient. With sovereign bond yields globally taking a dive lately, there’s also less pressure on policymakers to make any further tweaks to their YCC policy.

Yen on standby for policy hints

Yet, the rhetoric from Governor Ueda suggests some bias towards normalizing policy. Given the BoJ’s history to shock the markets, the risk of a surprise decision in January to either hike rates or end YCC, or both, cannot be dismissed.

However, such a risk is very low for the December meeting so much of the reaction in the markets will depend on any changes in Ueda’s language. Any clues that a rate increase is on the way in early 2024 could fuel the US dollar’s selloff against the Japanese currency.

Dollar/yen could extend its slide to the 61.8% Fibonacci retracement of the January-November uptrend at 136.65, which is near where prices troughed in July.

But if the BoJ disappoints by not altering much in its statement and Ueda gives little away in terms of fresh hints on the timing of a possible exit, dollar/yen could stage a rebound. Any upside could initially target the 23.6% Fibonacci of 146.09 before aiming for the 50-day moving average at 148.87.