{kind=link}

- Fed, ECB, BoE and SNB hold their final policy decisions of the year

- Will they push back on rate cut expectations?

- US CPI and flash PMIs will be crucial too

- UK GDP, Aussie jobs also on the agenda

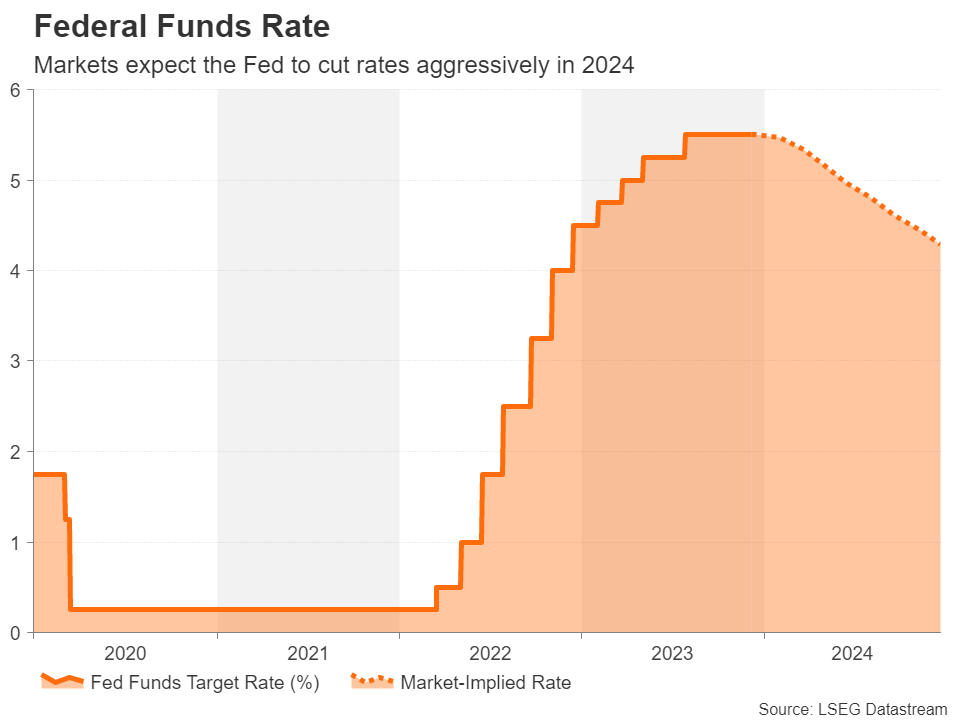

Fed to hold rates but will it signal big cuts?

The Federal Reserve is almost certain to keep its policy rate unchanged on Wednesday as the US economy finally appears to be losing some steam and inflation is coming under control. Chair Powell has set the bar high for raising rates again, while investors have gone a step further and completely priced out any chance of additional tightening.

The focus therefore on Wednesday will be how soon the Fed will start lowering rates, specifically how many rate cuts do FOMC members foresee in the updated dot plot that’s due the same day. In the last dot plot, policymakers were projecting that rates would end 2024 at 5.1%.

Following the recent soft readings on inflation, markets are betting that the Fed will cut rates five times in 2024, with a 25-bps reduction fully priced in for May. If policymakers push back against such expectations and predict fewer cuts, the US dollar could gain on the back of the hawkish signals.

The most bullish scenario for the dollar is if the Fed doesn’t even adjust its median projection for 2024.

Still, a hawkish rate path will likely not be enough to set the markets straight and Powell will have a tough task on his hands convincing investors that rate cuts are not on the near-term horizon, especially if the inflation data keeps surprising to the downside.

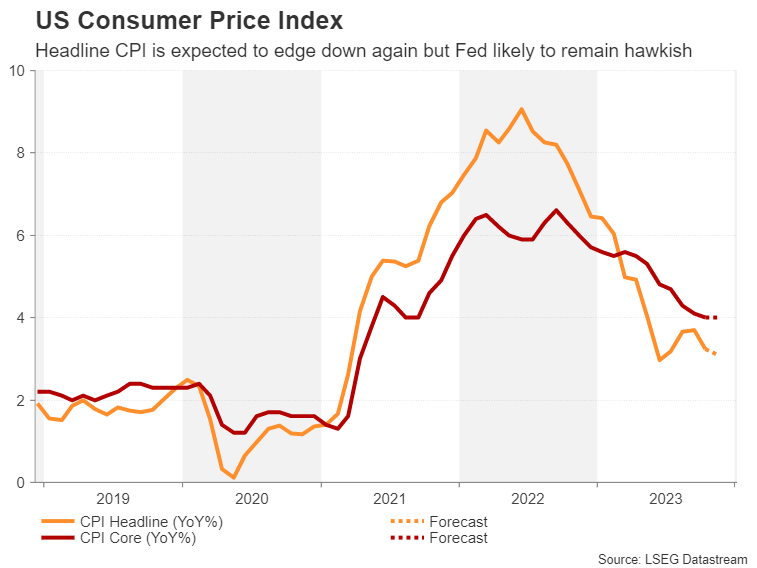

The CPI report for November is due on Tuesday and the forecast is for the annual rate of headline CPI to have inched down to 3.1% from 3.2%.

Investors will also be keeping an eye on the retail sales numbers for the same month on Thursday, while on Friday, there’s a raft of releases, including the Empire State manufacturing index, industrial production, as well as the flash S&P Global PMIs for December.

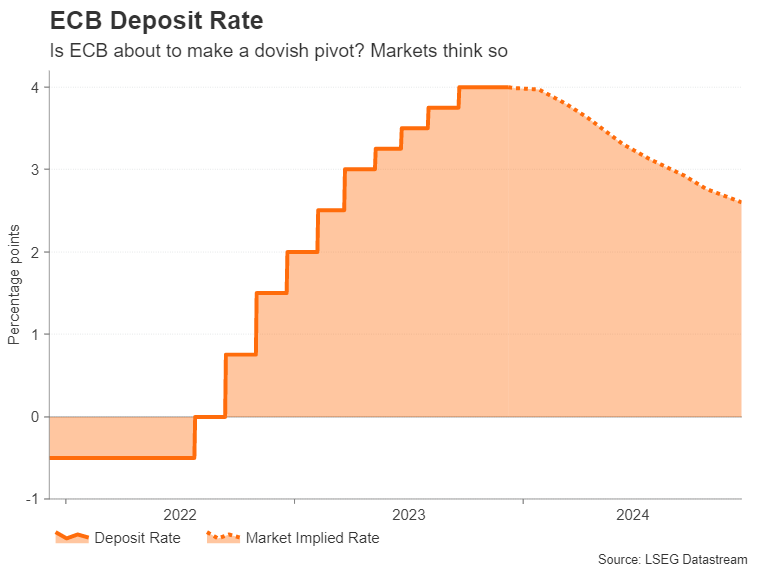

Will ECB decision add to euro’s downside?

The European Central Bank convenes for the final time this year on Thursday and the consensus is that it will keep the deposit rate at 4.0% for the second meeting in a row. Inflation has tumbled quite sharply in the past few months, hitting a more than two-year low of 2.4% y/y in November.

Even ECB policymakers have been taken by surprise by the speed at which inflation has come down lately. Subsequently, the tone has started to shift quite substantially within the Governing Council and a rate hike has now been firmly taken off the table.

Investors don’t see anything upsetting this downward trajectory in inflation and combined with the weakening economic backdrop, speculation is intensifying that the ECB will be the first major central bank to cut, possibly in April.

The euro has come under considerable pressure from the rate cut expectations, slipping below $1.08.

Should President Lagarde endorse the market view in her press conference, there could be further losses for the euro, while there’s not likely to be much relief from the data either.

The flash December PMIs are due on Friday. Only a modest uptick is expected for the services and manufacturing PMIs, though both readings are forecast to remain below 50.

BoE still flying the higher for longer flag

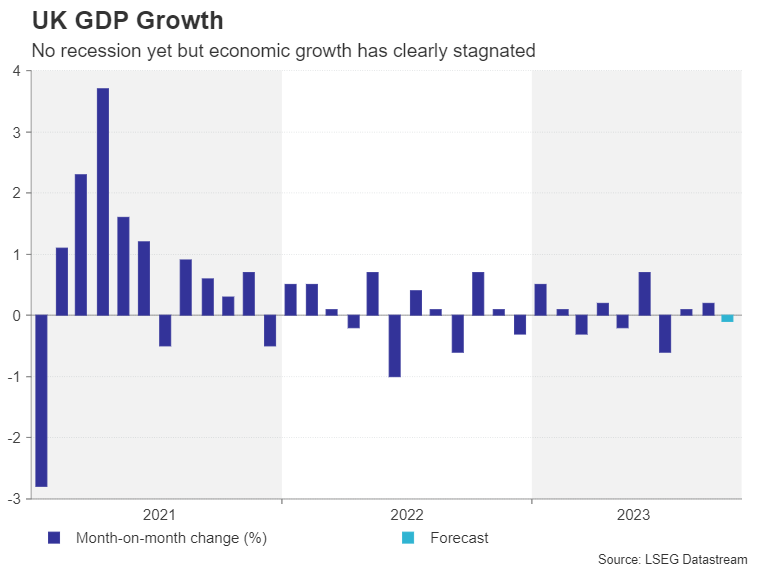

There was finally some good news for the Bank of England last month when inflation nose-dived below 5.0% in October. The pound, however, has perked up against the US dollar as the Fed is seen being less hawkish than the BoE. Another reason why sterling has bounced back lately is that the UK economy so far appears to be steering clear of a recession.

GDP and industrial production figures for October out on Wednesday will provide an updated view on the state of the economy, while there will be further clues from Friday’s flash PMIs. Tuesday’s employment report will be important too as the slowdown in the labour market has yet to translate to a moderation in super-hot wage increases.

The Bank of England is doing its best to strike a balanced tone amid sticky inflation and the ongoing concerns about stagnating growth. But policymakers have had to backtrack on some of their dovish remarks, with Governor Bailey doubling down on the higher for longer stance recently in an attempt to dampen speculation about an early rate cut.

No change in rates is anticipated on Thursday when the BoE meets, but should Bailey try to again brush off rate cut expectations by using stronger language in the statement, the pound is unlikely to gain much unless it is backed by upbeat data or a softer US dollar.

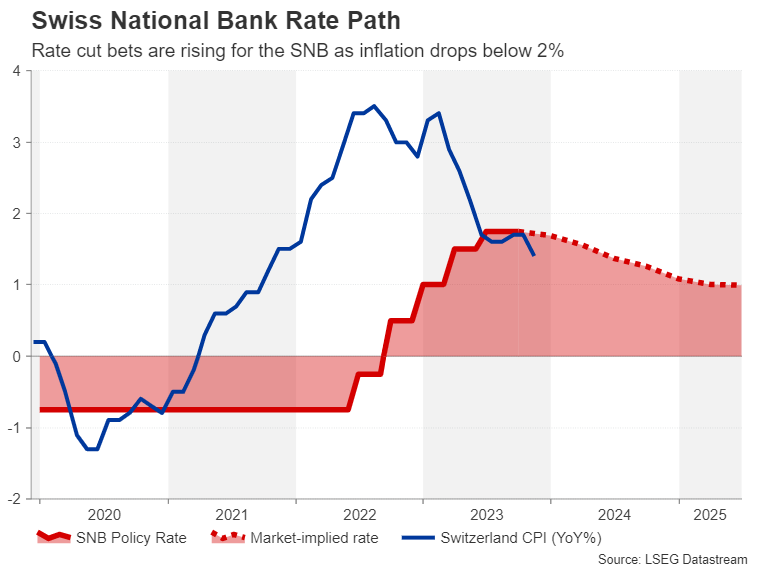

Swiss franc shines ahead of SNB decision

In Switzerland, the central bank will announce its decision early on Thursday. Markets are pricing in a 25% probability for an immediate rate cut. This follows a streak of disappointing data releases, with annual inflation sinking to just 1.4% in November and yearly GDP growth nearly coming to a standstill in the third quarter.

That said, the SNB is highly unlikely to cut rates so soon. The latest commentary from SNB Chairman Jordan in mid-November pointed to the possibility of raising rates further, so it would be a dramatic U-turn to abandon that stance and cut rates immediately.

More likely is that the SNB keeps rates unchanged but abandons its tightening bias and shifts to a neutral position instead. The question is, will that be enough to hurt the Swiss franc, which is the best performing major currency of this year? Markets are already pricing in three rate cuts for 2024, so a neutral shift wouldn’t be any surprise.

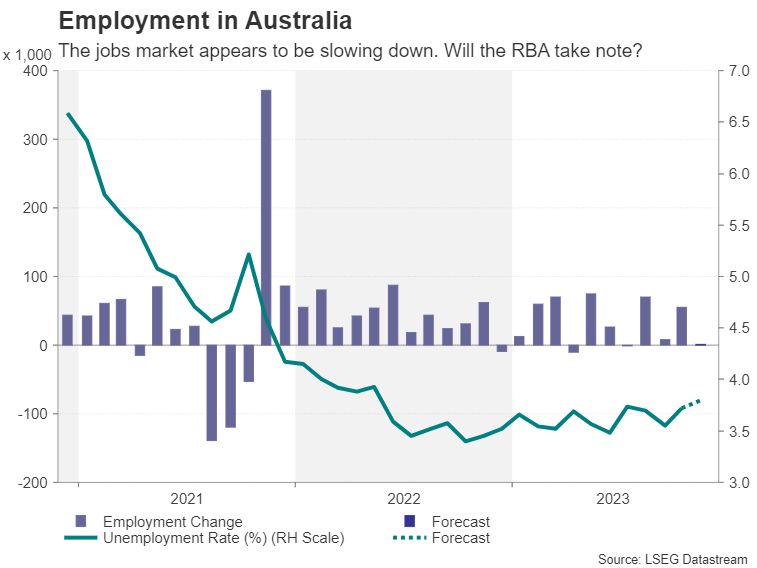

Aussie at risk from weakening economy

Another currency outperforming of late is the Australian dollar. A more hawkish Reserve Bank of Australia has been behind the aussie’s recent rebound but there are doubts about how long Governor Bullock will be able to maintain this rhetoric as the economic data has started to disappoint.

Following the bigger-than-expected drop in CPI in October, traders will be watching Thursday’s employment numbers for November. The flash PMIs on Friday will also be eyed, so will the batch of Chinese releases.

China’s consumer and producer price indices are out on Saturday, and on Friday, attention will turn to the industrial output and retail sales figures for November.

Any improvement in the Chinese data has the potential to offset any downbeat indicators for the domestic economy for the aussie. But the overall market mood will be just as crucial for risk-sensitive currencies and that will likely be determined by the Fed’s message on Wednesday.

Across the Tasman Sea, the third quarter GDP print will be the main item on the agenda for the New Zealand dollar.

Yen rocked by rate hike bets

Speculation is mounting that the Bank of Japan will exit negative rates as early as the December meeting, catapulting the yen sharply higher. Next week’s data are unlikely to significantly alter those expectations but will nevertheless be monitored, particularly the quarterly Tankan survey that’s out on Wednesday. Policymakers would feel more confident about raising interest rates if the data is headed in the right direction so there is scope for the yen to extend its gains in the coming days.

Other Japanese releases will include corporate goods prices on Tuesday, machinery orders on Thursday and the flash PMIs on Friday.