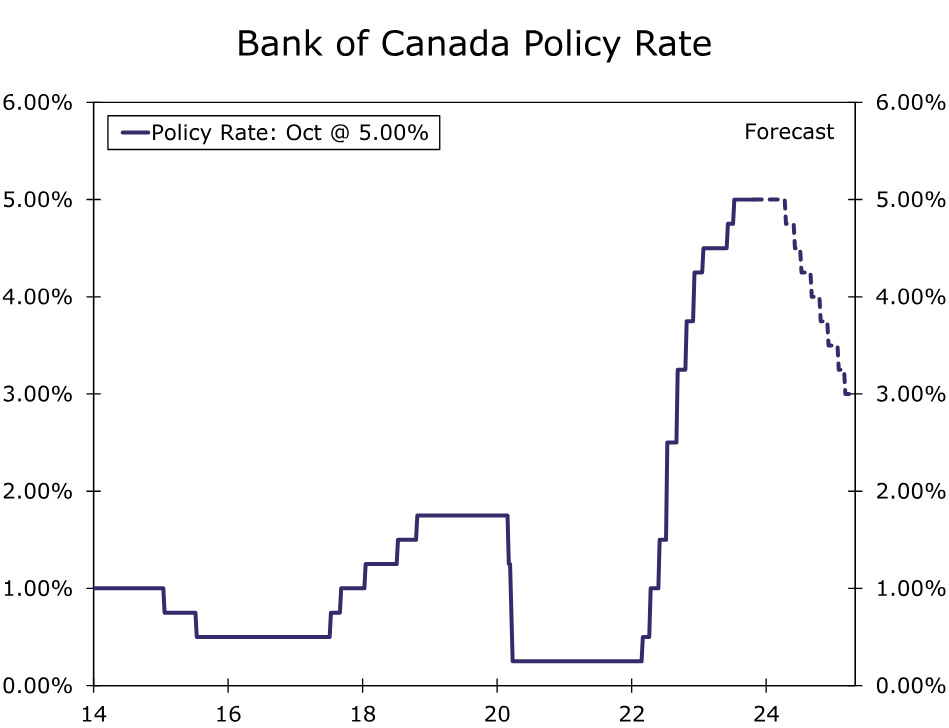

held its policy rate at 5.00% at its October announcement, and maintained a moderate tightening bias. However, we believe the BoC's interest rate pause will be an interest rate peak. Given we forecast slower growth and inflation than the central bank, we expect policy rate to hold steady for an extended period, before rate cuts begin in Q2-2024.){kind=link}

Summary

- Incoming data continues to point to increasing challenges and slower growth for the Canadian economy ahead. Past monetary tightening has led to a significant rise in the household debt servicing burden, while forward-looking surveys point to a softening business outlook. Amid this backdrop, we have lowered our Canadian GDP growth forecasts for 1.1% for 2023 and 0.7% for 2024.

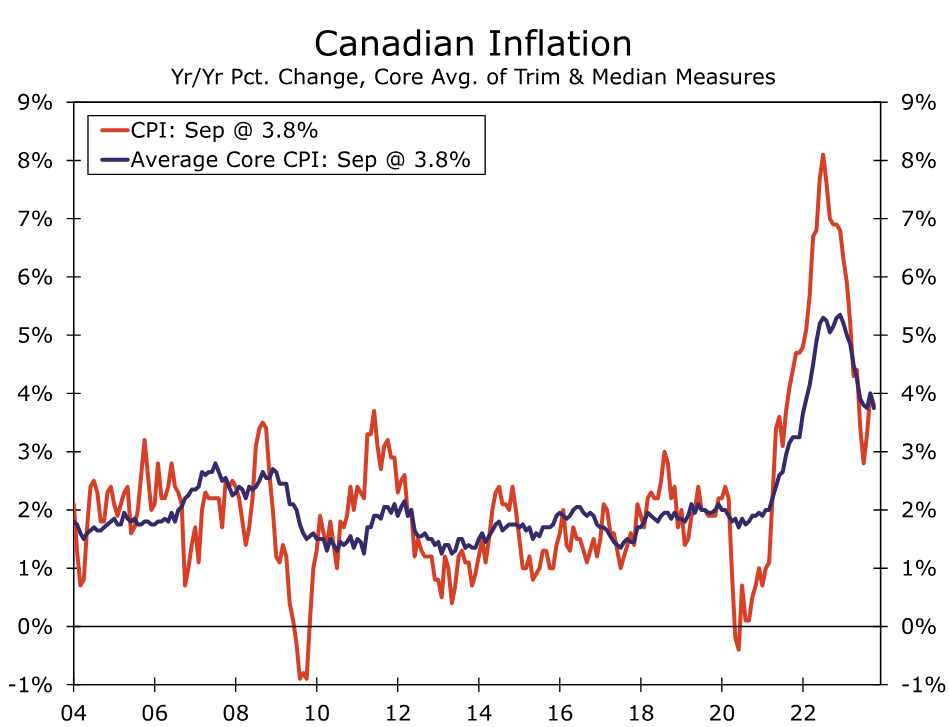

- Although Canada’s September CPI surprised to the downside, inflation remains elevated for now and continues to move only gradually in a more favorable direction.

- The Bank of Canada (BoC) held its policy rate at 5.00% at its October announcement, and maintained a moderate tightening bias. However, we believe the BoC’s interest rate pause will be an interest rate peak. Given we forecast slower growth and inflation than the central bank, we expect policy rate to hold steady for an extended period, before rate cuts begin in Q2-2024.

- As Canadian growth remains subdued and in the absence of further BoC tightening, we also see potential for further Canadian dollar weakness over the next several months.

Canadian Growth Challenges Accumulating

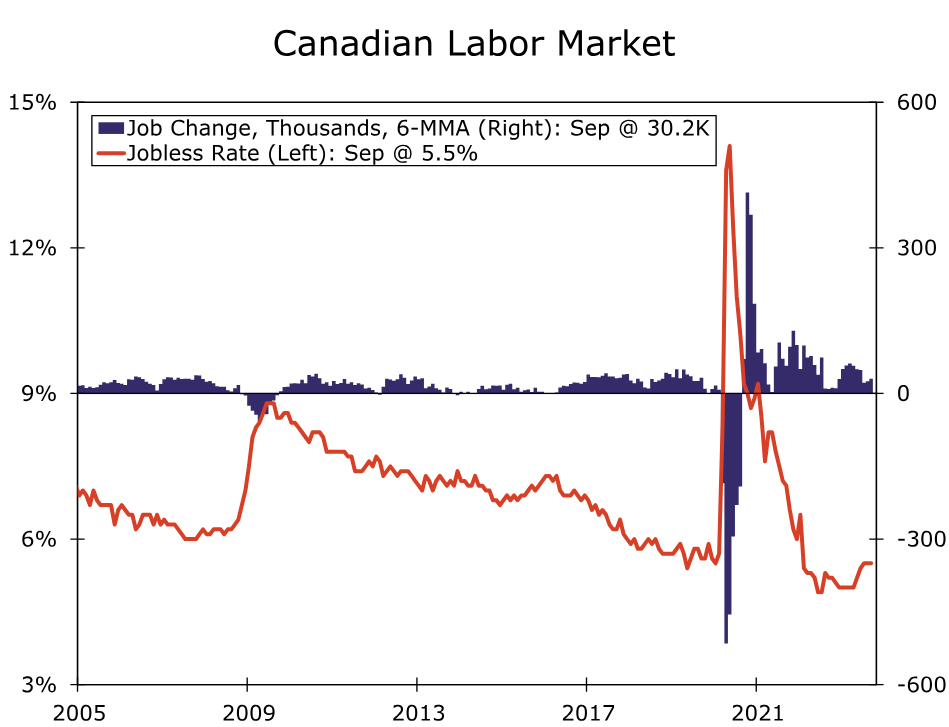

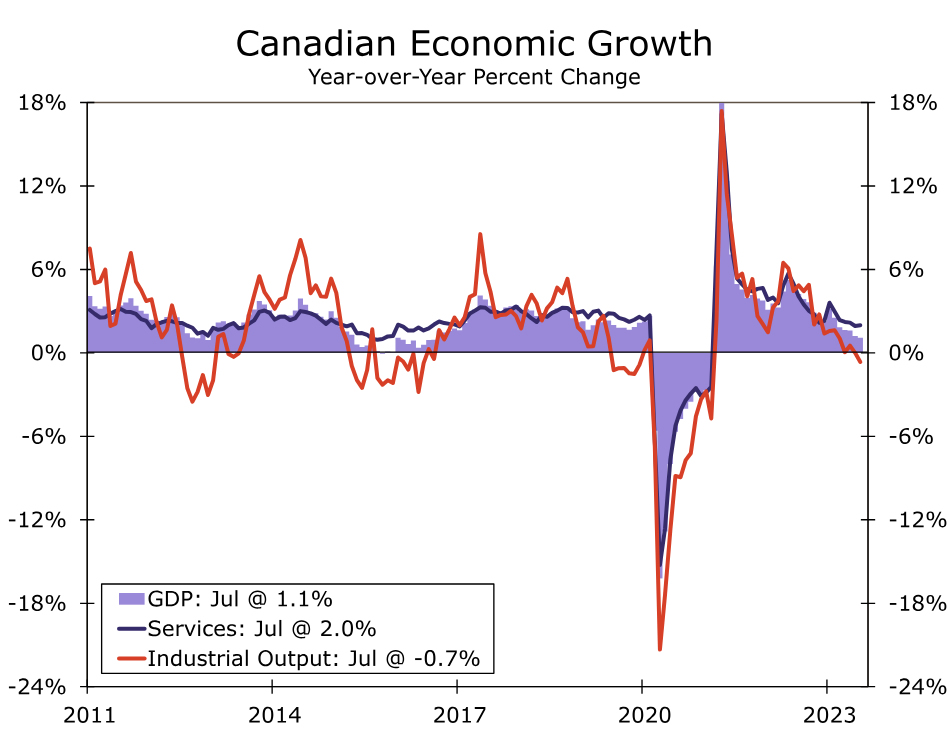

While Canada’s economy has shown pockets of strength in recent months, incoming data continues to point to increasing challenges and slower growth for the Canadian economy ahead. The main bright spot for Canada has been the labor market, which added a combined 103,700 jobs in July and August, while hourly wage growth for permanent employees remains elevated at 5.3% year-over-year. Even so, the employment gains are perhaps not as strong as they might appear at first glance. A 48,000 gain in full-time jobs accounted for less than half of the increase, whereas for the outstanding level of employment, full-time jobs make up 82% of total employment. Moreover, the July-August period saw a decline in private sector employees, with the jobs increase instead driven by a rise in public sector employees and self-employment. Other areas of the economy are noticeably less robust. Despite the employment gains, higher interest rates and cost-of-living issues appear to be contributing to consumer caution, with real retail sales having declined for three months in a row through August. More broadly, Canada’s Q2 GDP growth contracted at a 0.2% quarter-over-quarter annualized rate and, based on available data for July and preliminary data for August, is at best on track for only very modest positive growth in Q3.

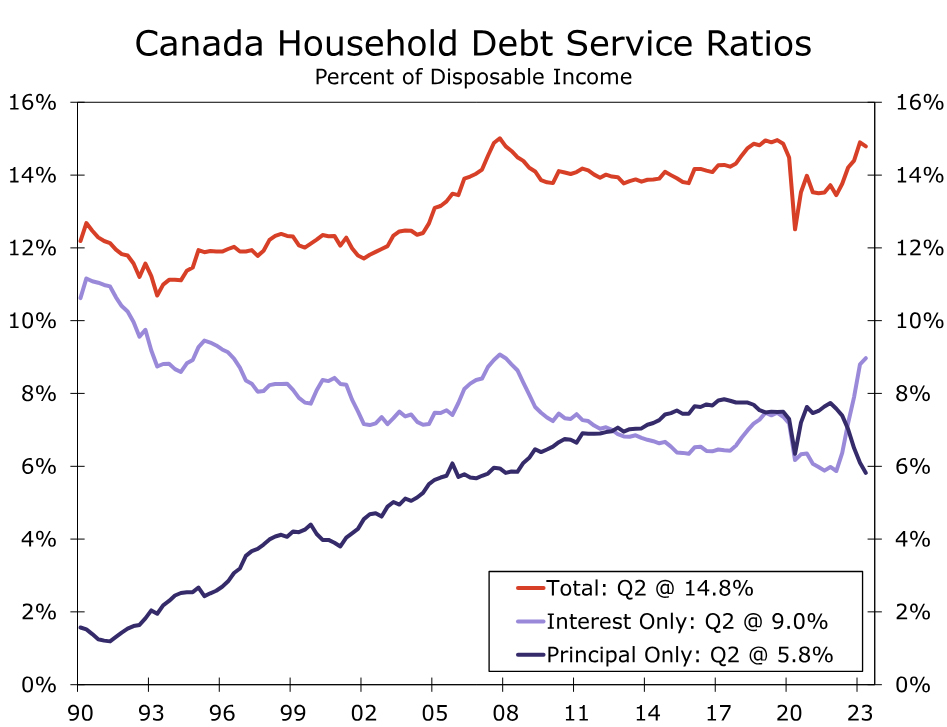

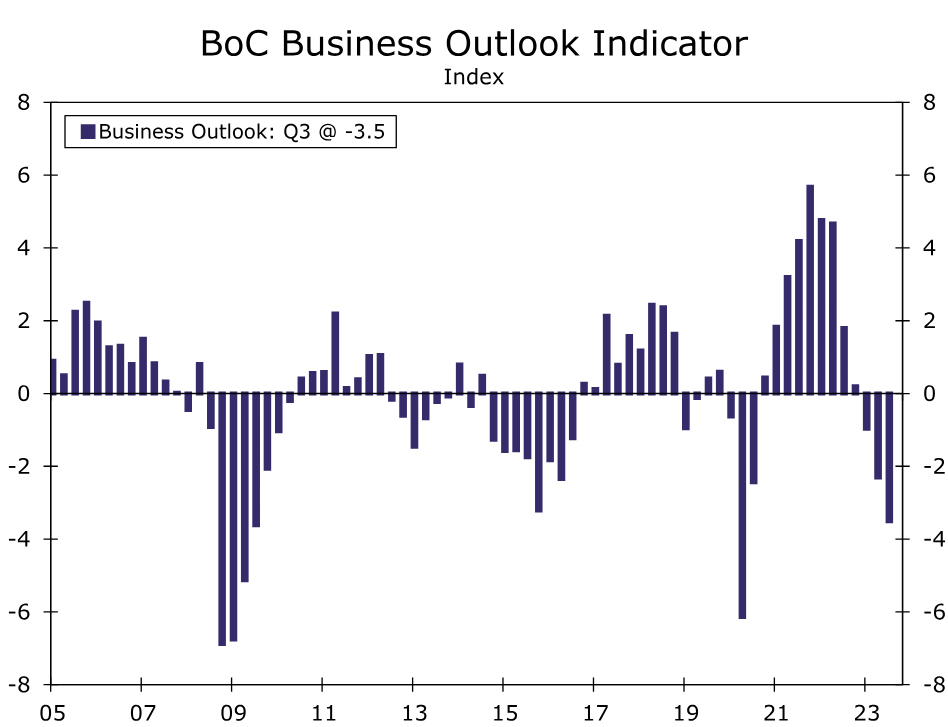

Moreover, economic fundamentals and forward-looking indicators do not point to an improvement in Canada’s growth prospects any time soon. From a consumer perspective, the outlook is mixed. Growth in real household disposable income has returned to positive territory and the household saving rate of 5.1% remains slightly above pre-pandemic levels. However, the Bank of Canada’s monetary tightening has led to a rising interest and debt servicing burden for Canadian households. In Q2, interest costs were 9.0% of disposable income, while total debt servicing costs (that is, principal and interest) were 14.8% of disposable income. Those metrics are elevated by historical standards, and suggest continued consumer restraint going forward. The outlook for businesses is similarly subdued. Declining corporate profit growth has led to a drop in business fixed investment through mid-2023, and the central bank’s Q3 Business Outlook Survey suggests the outlook may have worsened further since. The Bank of Canada’s (BoC) Business Outlook Indicator fell further to -3.5, the weakest reading since the depths of the pandemic. In addition, the Indicators of Future Sales balance, which takes into account factors such as order books, advance bookings, sales inquiries and so on, fell to zero in Q3, also the weakest reading since Q3-2020. Finally, more than half of firms surveyed by the BoC believe that the effects of past monetary tightening on their businesses are far from over. To the extent that more cautious businesses scale back hiring plans, that could add to headwinds for Canadian households and consumers. Against this backdrop we have pared our growth forecast for Canada, and now anticipate GDP growth of 1.1% in 2023 (previously 1.2%) and 0.7% in 2024 (previously 1.0%).

Canadian Inflation: High, But Heading In The Right Direction

While recent news on Canadian growth has been disappointing, news on the inflation front has been slightly more hopeful. The message from actual inflation data as well as forward-looking indicators are the same—inflation remains too high for now, but is gradually heading in the right direction. With respect to the September CPI, both headline and core inflation surprised to the downside. The headline CPI slowed to 3.8% year-over-year, while the average core CPI similarly eased to 3.8% year-over-year. Importantly, the average core CPI rose at a 3.67% three-month annualized pace through September. That is less than the increase seen in August, even if the recent trend of underlying inflation remains above the central bank’s 2% target and the underlying pace of disinflation remains frustratingly slow.

Survey data also point to elevated inflation trends that are nonetheless moving in a more favorable direction. The BoC’s Business Outlook Survey showed more firms expecting slower input and output price inflation over the next 12 months. For example, the net balance for input price inflation fell to -63 in Q3 from -53 in Q2 (that is, more respondents seeing slower input price inflation), while the net balance for output price inflation fell to -43 in Q3 from -33 in Q2 (more seeing slower output price inflation). In terms of firms’ CPI inflation expectations over the next two years, 53% saw inflation above 3% during that period, still high but less than the 64% in Q2 and 79% in Q1. Finally, in a separate survey of consumers during Q3, one-year ahead and two-year ahead inflation expectations were still elevated at 5.03% and 4.04% respectively. Nonetheless, that same survey said consumers who expect more adverse effects from rate hikes are less likely to plan major purchases such as cars or appliances, and more likely to spend on discretionary items like vacations and concerts—a hint perhaps that higher interest rates are having some impact on consumer expectations.

Bank of Canada’s Interest Rate Pause Will Be An Interest Rate Peak

Against this backdrop of slowing growth and gradually slowing inflation, the Bank of Canada once again held its policy interest rate steady at 5.00% at its October monetary policy announcement. In its accompanying statement, the BoC acknowledged softer economic activity, saying:

- There is growing evidence that past interest rate increases are dampening economic activity and relieving price pressures.

- Consumption has been subdued, and weaker demand and higher borrowing costs are weighing on business investment.

- A range of indicators suggest that supply and demand in the economy are now approaching balance.

- Economic growth is expected to be weak for the next year before increasing in late 2024 and through 2025.

The softer outlook is also reflected in the central bank’s updated projections, which forecast GDP growth of 1.2% in 2023 (compared to 1.8% in July) and 0.9% in 2024 (compared to 1.2% in July).

At the same time, the BOC kept the option of further tightening on the table, saying it is “prepared to raise the policy rate further if needed.” The central bank clearly remains somewhat wary about the inflation outlook, saying it “is concerned that progress towards price stability is slow and inflationary risks have increased.” Those inflation concerns are also reflected in the BoC’s updated inflation forecasts, which see CPI inflation at 3.0% for 2024 (previously 2.5%) and 2.2% for 2025 (previously 2.1%).

Although BoC maintained a moderate rate hike bias, we continue to believe that further tightening remains a possibility rather than a probability. We expect Canadian economic growth to slow more quickly than the central bank’s forecast, and as a result, we see slightly slower CPI inflation next year than does the central bank. We believe the Bank of Canada will hold its policy rate steady at 5.00% for an extended period. That said, as growth remains subdued and underlying inflation measures move a bit closer to the central bank’s 2% target, we still forecast Bank of Canada rate cuts beginning in Q2-2024, and a cumulative 150 bps of easing to 3.50% by the end of next year. As Canadian growth remains subdued and in the absence of further BoC tightening, we also see potential for further Canadian dollar weakness. The USD/CAD exchange rate has already reached our medium-term target of CAD1.3700, but a further move closer to CAD1.4000 over the next several months cannot be ruled out. We will provide a full assessment and updated currency forecasts in our International Economic Outlook, due for publication later this week.