{kind=link}

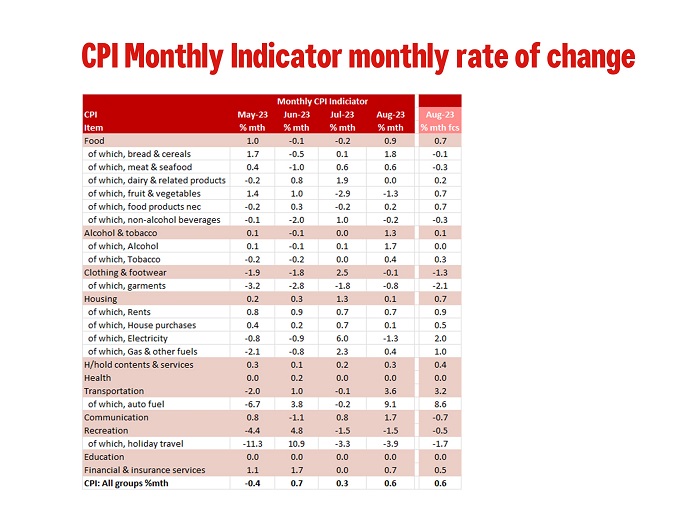

The Monthly CPI lifted 0.6% in August as expected. Inflation was restrained by various government energy rebates but there is still an upside risk to both our CPI and Trimmed Mean forecasts.

As reported by the ABS, the Monthly CPI Indicator rose 5.2% in the year to August, up from 4.9%yr in July but still a moderation from the peak of 8.4%yr in December 2022. This was in line with Westpac’s, and the market median forecast, of 5.2%yr.

As we noted in the preview, if the Monthly CPI Indicator printed as expected it would be pointing to some upside risk to our current forecast for the September quarter CPI of 0.9%qtr/5.1%yr.

It is also worth noting that the Monthly Indicator Trimmed Mean printed 5.6%yr, flat with the July print and so still a moderation from the peak of 7.2% in December 2022. This also suggests there is some upside risk to our current Trimmed Mean forecast for the September quarter of 0.8%qtr/4.7%yr.

In annual terms, the most significant contributors to the August increase were housing (6.6%), transport (7.4%), food & non-alcoholic beverages (4.4%) and insurance & financial services (8.8%).

The ABS noted that the rate of inflation for housing, at 6.6%yr, was lower than it was in July (7.3%). New dwelling prices are up 4.8%yr, the lowest annual pace since August 2021, as price increases for building materials continued to ease, reflecting improved supply conditions. Rents are up 7.8%yr, slightly higher than July’s 7.6%yr print, as the rental market continues to tighten.

As readers will know we prefer to look at the monthly changes to give us a better guide of what we think the current quarter will look like for inflation. In August, the Monthly CPI Indicator lifted 0.6%, in line with our forecast and consistent with our overall view on inflation momentum. There were, however, some interesting divergences in the components.

Food prices were broadly in line with expectations, but alcohol & tobacco were stronger at 1.3% vs 0.1% forecast, as was clothing & footwear (–0.1% vs –1.3% forecast).

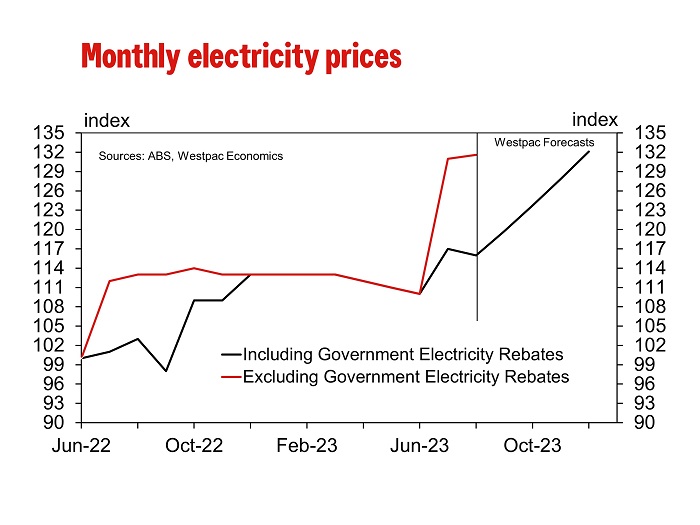

The larger surprise for us was housing, which rose just 0.1% vs our forecast of 0.7% due to softer than expected rents (0.7% vs 0.9% forecast), dwelling purchase costs (0.1% vs. 0.5% forecast) while electricity prices fell (–1.3%) due to the impact of government rebates compared to our forecast for a modest increase (2.0%). Gas & other household fuels also rose more modestly than expected (0.4% vs 1.0% forecast).

The ABS provided some detail around the rebates. The fall in August was due the introduction of rebates from the Energy Bill Relief fund for concession households in Melbourne. Without the Energy Bill Relief Fund rebates in Melbourne, electricity prices would have risen 0.5% in August. Energy Bill Relief Fund rebates, introduced in July 2023, continue to reduce electricity bills for concession households in Sydney, Adelaide, Hobart, Darwin and Canberra and for all households in Brisbane and Perth this month.

Looking forward, the ABS notes that in addition to concession households, households newly eligible for the Energy Bill relief fund will likely see these rebates reflected in energy bills from October for Sydney, Adelaide, Hobart, Darwin and Canberra. For Melbourne, rebates for newly eligible households will be reflected from November 2023. As such, the level of electricity prices is unlikely to get to the level it is without rebates before December this year, or it could extend into the first quarter of 2024.

We are currenting revising our CPI forecast in light of this data including the critical update of the quarterly services prices. But we can note that in our preview, we suggested that if the monthly indicator printed as expected it would point to some upside risk to our current Q3 CPI forecast of 0.9%qtr/5.1%yr.