could fall by around 1%-1.5% in the several weeks following the start of the shutdown. Also in recent shutdown episodes, three months after the shutdown began the dollar had recovered its losses and there was no meaningful or long-lasting impact on the dollar. In the event a U.S. government shutdown does occur, we would expect a similar pattern to unfold, and we would not make significant changes to our longer-term outlook for the U.S. dollar.){kind=link}

Summary

A potential U.S. government shutdown that could start October 1st looms, the chances of which are more or less seen as a coin flip at this point. Should a shutdown transpire, there could be a negative impact of the U.S dollar, albeit one that is likely to be modest and short-lived. Recent history suggests the U.S. dollar index (DXY) could fall by around 1%-1.5% in the several weeks following the start of the shutdown. Also in recent shutdown episodes, three months after the shutdown began the dollar had recovered its losses and there was no meaningful or long-lasting impact on the dollar. In the event a U.S. government shutdown does occur, we would expect a similar pattern to unfold, and we would not make significant changes to our longer-term outlook for the U.S. dollar.

Potential U.S. Shutdown Looms For the U.S. Dollar

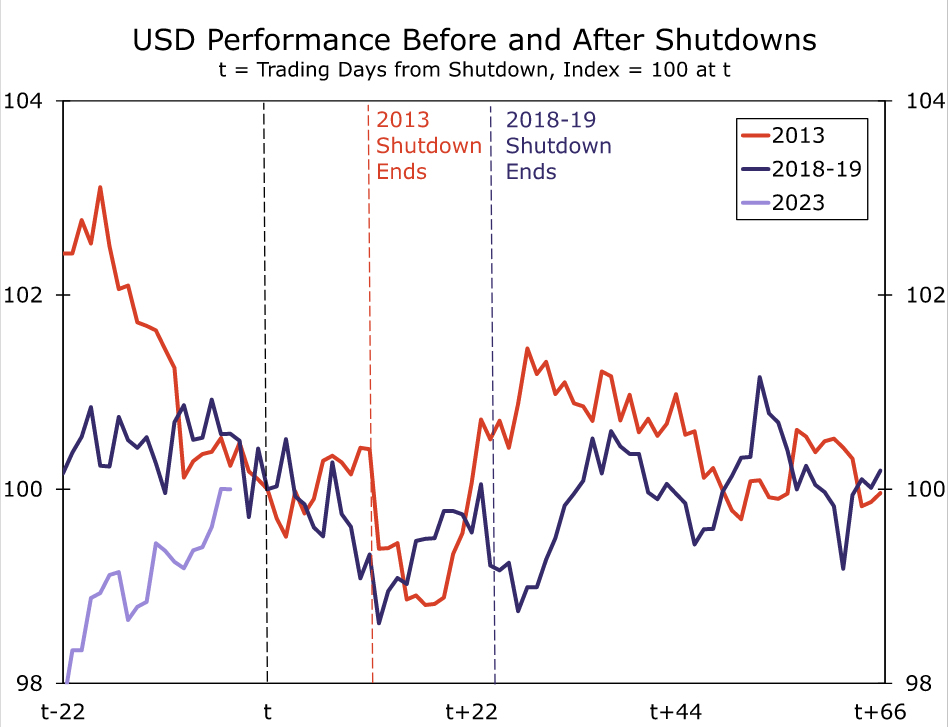

Last week our U.S. economics colleagues wrote about the potential for a U.S government shutdown that could begin on 1 October. At this point, our teammates believe the chances of U.S. government shutdown are more or less a coin flip. In recent U.S. government shut down episodes, the direct hit to U.S. growth was modest. Consumer confidence has historically dipped during periods of a government shutdown, and while the impact to U.S. growth has typically been immaterial, not all the lost economic activity was fully recovered. The above report captures the economic impact of a government shutdown. In this report, we will assess the potential implications of a government shutdown on the U.S. dollar. History of U.S. government shutdowns is somewhat limited, but we can infer the potential impact on the dollar by examining the most recent episodes. To that point, we examined the shutdowns that began in October 2013 (which lasted for 16 calendar days or 11 trading days) and December 2018 (which lasted 35 calendar days or 24 trading days). In our view, these most recent episodes are likely to be the most instructive for a potential shutdown in 2023. The economic and political environment in 2013 as well as 2018-2019 more resembles the current political and economic climate than the backdrop during the prior shutdown of the 1990s.

We assess the greenback’s performance using the U.S. dollar index (DXY). Our first observation is that, at least heading into these two shutdowns, the U.S. dollar’s performance is varied and driven by the prevailing economic conditions, not necessarily anticipation of the shutdown. In 2013, the U.S. dollar softened in the weeks heading into the shutdown. At that time, U.S. economic growth was subdued and Federal Reserve interest rates were steady at essentially 0%. The 2013 government shutdown occurred toward the end of the Fed’s “Taper Tantrum”, which is important to note as longer term U.S. Treasury yields had already started to stabilize and global equity markets had begun to recover. Against this backdrop, the U.S. dollar was softening as risk sentiment started to improve. During the 2013 government shutdown, the U.S. dollar index actually gained very slightly (by 0.4%) over those 11 trading days. However, U.S. dollar sentiment did take a short-term hit such that 17 trading days after the start of the shutdown, the U.S. dollar index saw the largest peak-to-trough decline of 1.2%. Nonetheless, three months from the start of the shutdown, the U.S. dollar index had recovered all of its losses.

In contrast, during the 2018-2019 period, the U.S. dollar was steadier heading into the shutdown. In this instance, the U.S. economic backdrop was firmer relative to 2013 in that U.S. GDP growth was on a clear upwards trend. The Federal Reserve was coming to the end of a rate hike cycle and, towards the end of 2018, U.S. equity markets also corrected lower, providing safe haven support to the greenback during a period of elevated financial market volatility. Over the course of the 2018-19 episode, the U.S. dollar index fell marginally (by 0.8%) during the actual shutdown episode. Once again, U.S. dollar sentiment took a short-term hit such that 12 trading days after the start of the shutdown, the U.S. dollar index saw the largest peak to trough fall, a decline of 1.4%. In similar fashion to 2013, the greenback also fully recovered its losses experienced during this period three months following the start of the shutdown.

Today’s environment is quite similar to 2018-2019. The current backdrop is defined by resilient U.S. economic growth as well as a Federal Reserve that is approaching, or has possibly already reached, the end of its tightening cycle. Also, similar to 2018-2019, equity prices are correcting lower. While it is worth noting that the current landscape is most similar to 2018-19, the greenback has followed a consistent pattern once those shutdowns began, regardless of the pre-shutdown trend. That is, a short-lived and modest decline in the value of the dollar. We would expect the greenback to behave very similarly if a U.S. government shutdown transpires this time around, and a shutdown could translate into a 1%-1.5% decline in the DXY dollar index in the weeks after the event transpires. At the same time, we believe the same pattern of a dollar rebound would be repeated this time around. In our view, any greenback depreciation will be short-lived, and we would expect the dollar to recover in the months following the re-opening. Longer-term, once the shutdown ends and is in the rearview mirror, whether U.S. economic resilience survives the shutdown, and how high and for how long the Federal Reserve keeps its policy interest rate, will likely remain more consequential to the U.S. dollar’s performance. In our view, with the Fed still leaning hawkish and a U.S. “soft landing” more possible, despite the short-term depreciation forces the dollar could experience, we would continue to forecast a stronger U.S. dollar through the end of 2023 as the broader economic environment proves to be the driving force of the greenback.