rate hike have cooled substantially. Payrolls and GDP data that show the economy coming off the boil, reflect a year and a half's worth of rate hikes doing their job to cool economic momentum. The job's not quite done yet, but with the data coming in soft this week, the BoC can feel better about how far they've come in reaching the target state.){kind=link}

U.S. Highlights

- The U.S. economy added 187k jobs in August, but revisions to the two prior months subtracted a notable 110k jobs from the previous reported tally.

- Both total and core PCE inflation rose by 0.2% month-on-month in July, equal to the monthly change seen in June for both measures.

- Hurricane Idalia, the first of the season to make landfall in the U.S., caused widespread flooding and wind damage through Florida’s Big Bend region and up through Georgia and the Carolinas.

Canadian Highlights

- Payrolls and GDP data show the economy coming off the boil, reflecting a year and a half’s worth of rate hikes doing their job to cool economic momentum.

- Markets pricing for another rate hike by year-end has come in noticeably, following the string of softening data.

- The job’s not quite done yet, but the Bank of Canada can feel better about how far they’ve come in reaching the target state.

U.S. – The Labor Market Takes a Holiday

The U.S. almost managed to escape August without a major hurricane, but unfortunately those hopes were dashed when Hurricane Idalia made landfall as a category 3 hurricane on Wednesday in Florida. Strong winds, rain, and storm surges caused widespread flooding and property damage, leaving hundreds of thousands of Americans without power across the Southeast. Although the extent of the damage is still being assessed, insurance and clean-up costs are expected to be well over a billion dollars.

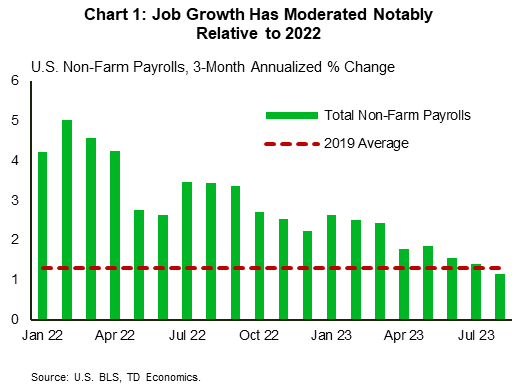

Fortunately for the national economy, sunnier skies could be found in this week’s economic data, including the 187k new jobs added in August. While this reading, in addition to the downward revisions to the previous two months, marks a continued moderation in the pace of hiring, it indicates that supply and demand in the labor market are coming into a more sustainable alignment (Chart 1). This was further evidenced by the decline in job openings in July, with the job opening to unemployed ratio falling to 1.5. While the unemployment rate did rise to 3.8%, this mostly resulted from a boost in labor force growth which could be considered a net positive if it helps to offset labor shortages. On aggregate, this progress will come as positive news for the Federal Reserve, however the most recent data on inflation was slightly more mixed.

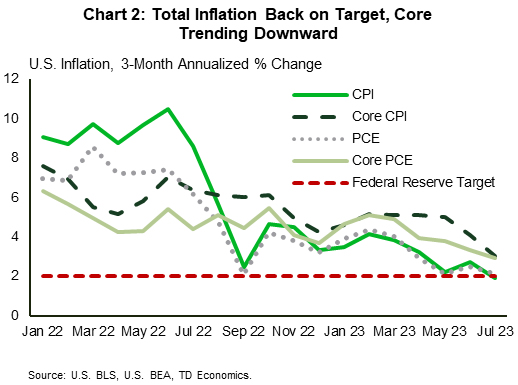

On Thursday, we saw that PCE inflation rose by 3.3% year-on-year (y/y) in July, up from 3.0% in June. This was driven by a moderation in the negative base effects resulting from the spike in energy prices last year in addition to a moderate uptick in services inflation – driven entirely by Powell’s ‘supercore’ component. Looking at the 3-month annualized trend (Chart 2), we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

Some offset to inflationary pressures continues to be provided by the goods sector, with the ISM Manufacturing Purchasing Managers’ Index (PMI) showing manufacturing activity contracted for a tenth consecutive month in August. Ten out of sixteen industries reported lower input prices, which is likely factoring in downstream to the consumer. Price growth in the services sector has been more stubborn, so next week’s update on the ISM Services PMI will offer insight into how resilient the sector remains.

With the Labor Day holiday on Monday, next week will be short both in length and in the volume of economic data that we receive. However, the release of the Fed’s Beige Book will be one item to watch, as it will feed into the viewpoints that FOMC members bring to the upcoming meeting. We expect that the progress on inflation and job market cooling up to this point will be sufficient to warrant a hold in 2 weeks’ time, but the tone will likely remain hawkish to guard against the potential for pre-mature easing in financial conditions.

Canada – Soft GDP Data Take Pressure off BoC

And just like that, concerns about the need for another Bank of Canada (BoC) rate hike have cooled substantially. Payrolls and GDP data that show the economy coming off the boil, reflect a year and a half’s worth of rate hikes doing their job to cool economic momentum. The job’s not quite done yet, but with the data coming in soft this week, the BoC can feel better about how far they’ve come in reaching the target state.

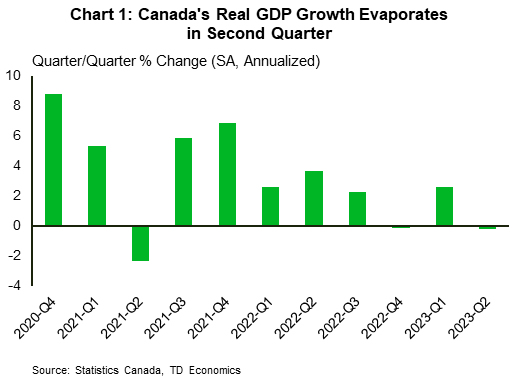

This week came as a bit of a bad news is good news moment. GDP growth in the first quarter was revised downward, easing some concerns that growth had accelerated substantially above-trend in early 2023. With a healthy hand-off from the first quarter, market consensus was that momentum in the second quarter would see the economy expand at a 1.2% quarter-on-quarter (q/q, annualized) rate. What happened was a loud thud, with the economy shrinking marginally (-0.2% q/q) amid a steep drop-off in consumption growth and a host of extreme events (Chart 1). Striking workers and a horrific fire season acted as a drag on activity – bringing the economy to a standstill.

Looking forward, there doesn’t appear to be much relief. The third quarter looks to be getting off on the wrong foot as Statistics Canada’s flash estimate shows the economy failed to grow in July. This is in line with our view that overall economic momentum will remain weak over the rest of this year. With rates set to remain well in restrictive territory for the coming months, the prospect of strong growth in the second half of 2023 seems far-off.

The news has palpably shifted investor sentiment. Market pricing that had started the week with roughly six-in-ten odds of a hike by the end of this year has pulled back to a much more moderate one-in-ten as of this morning. On cue, bonds are rallying as investors look to lock-up solid yields. Ten-year yields that started the week at roughly 3.7% have shaved off about 15 basis points as of the time of writing. The five-year yield is down nearly 25 basis points over the same time span.

That said, while the economy is cooling, it’s not cold. The labour market is still churning out jobs. This week’s Survey of Employment, Payrolls and Hours (SEPH) showed fixed weight wages still growing at 3.9% year-on-year (y/y). While the fixed weight wage gains are slightly lower than the 5% y/y print from the Labour Force Survey, they both reflect a labour market that, despite recent setbacks, still has a healthy appetite to hire – a fact supported by job vacancies that are still roughly 250k positions higher than before the pandemic.

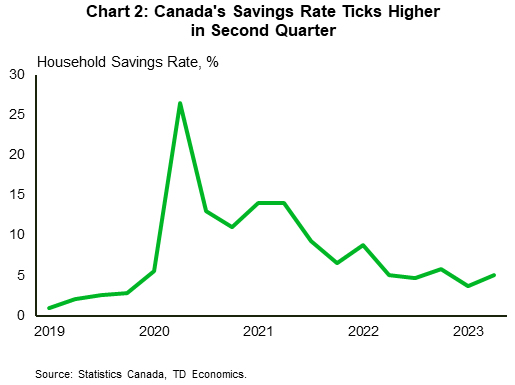

For the BoC, the totality of this week’s data suggest that things are still trending in the right direction to meet its mandate. Sure, the labour market suggests that underlying pressures persist, but spending data show consumers aren’t freely spending their wage gains – as the savings rate ticked up 1.4 percentage points (Chart 2). In totality, the case for further hikes weakened this week, helping lift hopes of a soft landing.