{kind=link}

With the market anxiously expecting this week’s Jackson Hole gathering, on Wednesday we will get the preliminary UK PMI survey results for August. As the pound remains one of the market’s favorites, a positive surprise at this week’s data releases could quickly reignite the BoE’s rate hike expectations and allow the euro/pound pair to record a new 2023 low.

BoE’s next steps

Contrary to the Fed, the BoE is still trying to bring inflation under control in the UK. Despite the recent easing recorded, from the double-digit CPI level last seen in March 2023, both the headline and core inflation indicators remain extremely elevated when considering the 500bps of cumulative rate hikes announced since February 2022. The BoE’s own projections have inflation dropping to their target at the two-year horizon, but the recent oil price action is complicating both the short- and medium-term picture. This development could eventually cancel out the strong expectations for a continued inflation easing globally during the remainder of 2023.

In the meantime, the BoE is facing a double-edged sword regarding earnings growth. On the one hand, strong household earnings are extremely helpful amidst the current cost-of-life crisis, supporting consumer spending, and thus somewhat boosting the anemic growth outlook. Friday’s GfK consumer confidence is unlikely to show a significant improvement, but it will remain comfortably above its mid-2022 lows.

On the other hand, there is an increasing and credible risk of second and third round effects manifesting as the higher inflation rate could become part of the public’s mindset. The latter is mentioned in the August 3 meeting’s minutes revealing a real worry from certain BoE members. This could also explain why two BoE members voted for a 50bps rate move at the last meeting, with the 25bps decision reached by a majority vote.

A busy week has just started

The Rightmove house price index showed a -0.1% year-on-year growth, confirming other house price indices, and thus depicting the continued weakness seen in this sector, which is unlikely to abate any time soon considering the current BoE rate’s outlook. The main dish of the week will come on Wednesday with the release of the preliminary figures of the Manufacturing and Services PMI surveys. The former has been a source of concern globally as it remains stuck well below its 50-midpoint in most regions.

In the UK, the Manufacturing PMI survey has been on an acute downward trend since the June 2021 high. It is now preparing to complete a 12-month period of sub-50 prints since Wednesday’s figure is expected to record another small drop to 45 from 45.3 in July. On the flip side, the Services’ PMI survey figures have globally been more positive but the same cannot be said for the UK. The July print came at 51.5, showing an expanding sector, but its recent trend has been negative and thus increasing concerns that the remainder of 2023 could be an even weaker growth period.

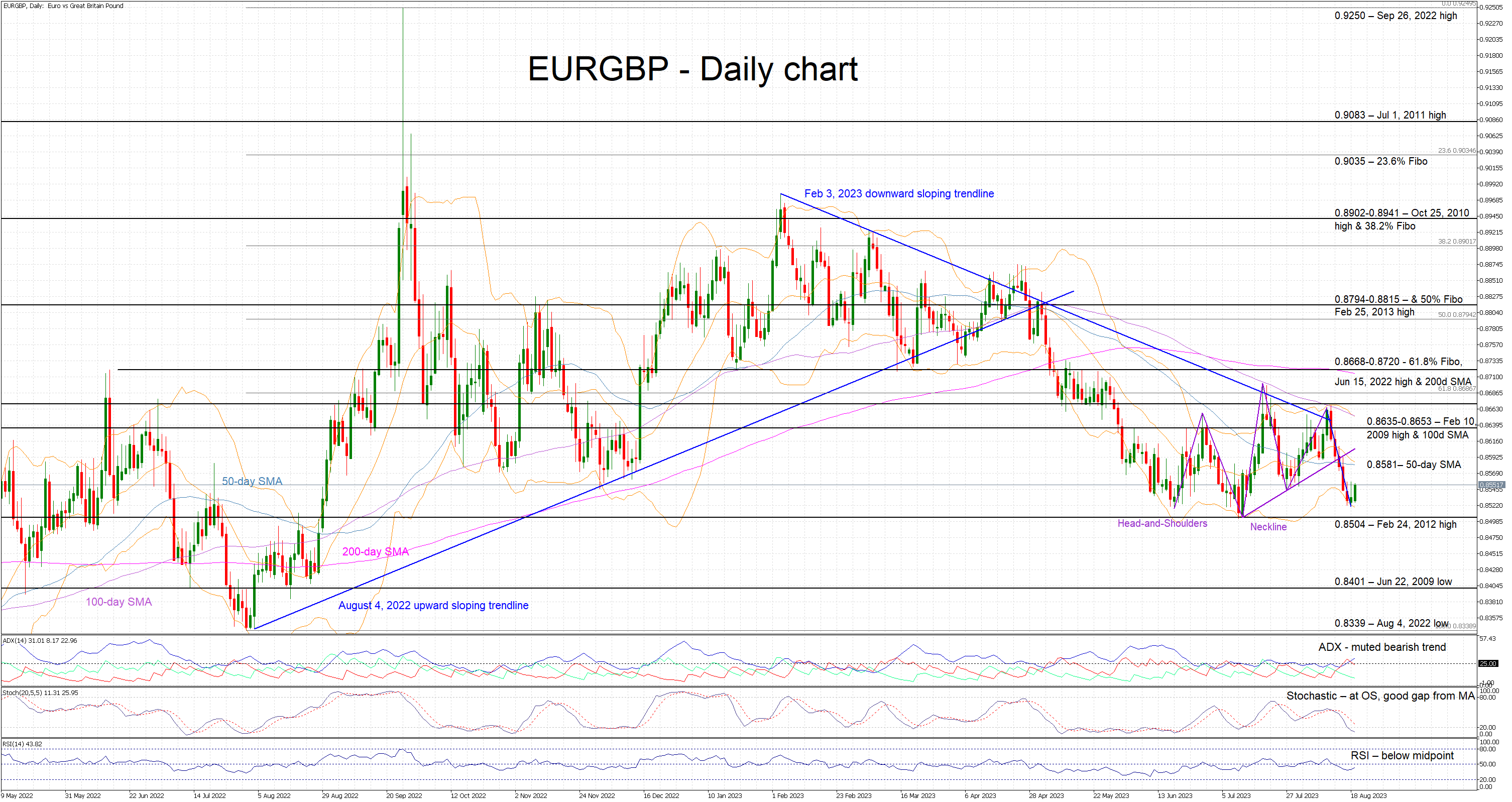

Euro/pound ready for a new 2023 low?

Despite the more hesitant BoE and the mixed data releases, the pound continued to exhibit significant strength against the euro. The overall technical picture appears to still favour the pound, especially considering the developing heads and shoulders structure. Therefore, a good set of PMI survey results on Wednesday morning could prove the boost needed for the euro/pound pair to record a new 2023 low, below the current 0.8503 low.