{kind=link}

U.S. Highlights

- Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation.

- The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown.

- The Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Canadian Highlights

- Canadian GDP growth has pointed to a new cruising speed, as the country worked through several shocks, including the public sector strike and wildfire shutdowns.

- The BoC’s summary of deliberations signaled the central bank is trying to strike the right balance between bringing inflation back to target without putting too much pressure on the economy.

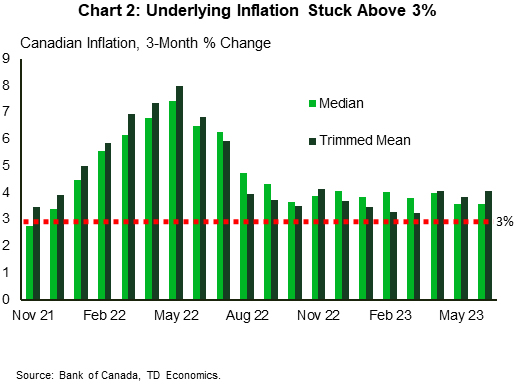

- With underlying data pointing to inflation being stuck around 3%, the BoC appears to be leaning hawkishly, which has kept yields elevated and supported the loonie.

U.S. – Preparing for Landing

Readers would be right to ask, what’s “moderate” about another upside surprise to economic growth in the second quarter? Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation. Incoming data have shown that the economy remains resilient – buoyed by healthy consumer spending growth and business investment – as fears of a recession gradually fade. What remains to be seen is whether inflation will continue to moderate in the coming months or whether the Fed will have to push interest rates higher still – thereby raising the odds the economy contracts.

The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown. However, the composition of growth was interesting. In line with our forecasts, consumer spending growth advanced 1.6% quarter-on-quarter (q/q) annualized – slowing from 4.2% in Q1. The Fed will be reassured that its rate hiking cycle is filtering through to consumer behavior as spending growth slows despite a drum-tight labor market. Moreover, with rates at multidecade highs, the housing market is feeling the force of tight financing conditions, with residential investment continuing to pull back in the second quarter – now contracting for the ninth quarter in a row. With demand growth slowing, imports pulled back again – now having contracted for the third time in the past year. The gradual slowdown is also not unique to the U.S., as plummeting export growth indicates the global economy is slowing under the weight of inflation and higher interest rates.

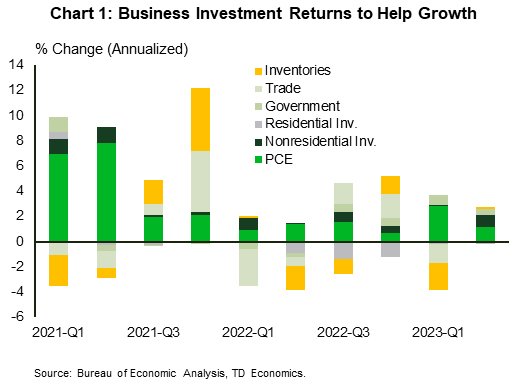

A pleasant surprise in the data was the healthy activity in the business sector that provided a meaningful lift to the economy (Chart 1). Nonresidential investment advanced 7.7% q/q – good for the strongest showing since the first quarter of 2022. The flow of federal funds to support climate friendly investments is helping fuel the ongoing strength in structures and equipment investment – the latter registering its best quarterly growth rate since 2011, outside of the post-2020 lockdown bounce.

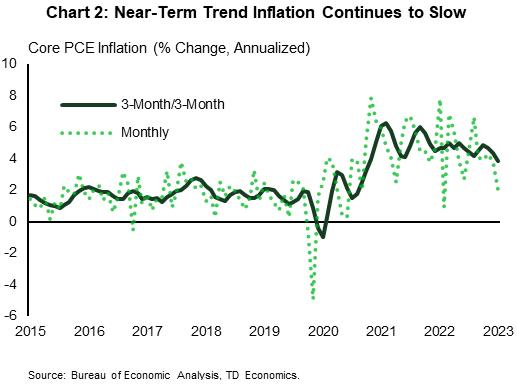

With full second quarter data showing a healthy consumer, all eyes were on June’s personal income and outlay report for signals of spending and price momentum heading into the summer months. Healthy spending held up in June and outstripped income growth, denting the personal savings rate. Between higher interest rates, strong inflation and depleting savings the pandemic era spending binge is slowing down. This is music to the Fed’s ears as it means softening inflationary pressures. Needless to say, the downside surprise on core PCE inflation (4.1% year-on-year vs. 4.2% expected) was a particularly welcome development. Even more encouraging, the near-term trend (Chart 2) has eased to its slowest pace since March 2021.

With inflation slowing and consumer spending remaining resilient the odds of a soft landing are ticking higher. However, the Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Canada – Canadian Economy Searching for Balance

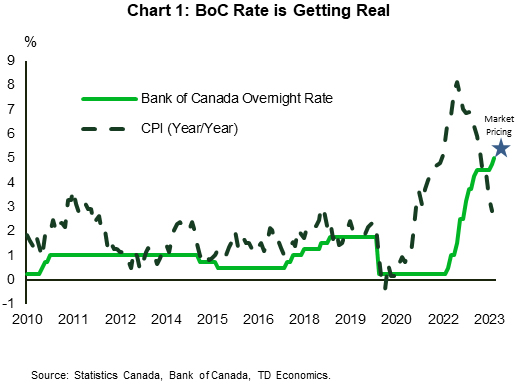

Economic momentum in Canada looks to be finding its cruising speed in spite of a number of shocks that hit the country over the last few months. With GDP accelerating in May, and payroll data bouncing back strongly, expectations for another Bank of Canada (BoC) hike have nudged higher this week (Chart 1). This has the Canada two-year yield reaching a 22 year high of 4.8%, pushing the Canadian dollar to the upper end of the 72 to 76 U.S. cent range that has prevailed over the last ten months.

After leading the G7 in GDP growth in the first quarter of 2023, tracking for the Q2 has come in right around our estimate of 1% quarter-on-quarter annualized. Not bad considering the negative impulse coming from the public sector strike and wildfires that caused many firms in the oil & gas sector to shut production. Indeed, growth remained quite broad, with 12 of 20 industry sectors in expansion. Within this, the service sector continued to drive growth, a sign that cyclical strength may persist through the remainder of the summer.

As has been the case over 2023, strong consumer demand has been the impetus for Canadian economic resilience. And it hasn’t just been people spending on ‘need to have’ items. Canadians have been spending on luxury items, such as new cars and dining out at restaurants. Such behaviour is not what occurs when people are preparing for recession. The robustness of the labour market has raised confidence. People have been seeing plenty of jobs on offer and wages rising faster than inflation. This improves purchasing power, notwithstanding the high interest rate environment. Just look at this week’s payroll data, which showed a 130k gain in May and more than offset the impact of April’s public sector strike decline.

The BoC has highlighted the resurgence in economic momentum for why it decided to execute on back-to-back rate hikes in June and July. While the BoC still thinks that consumer spending will cool on the back of past rate hikes, in its summary of deliberations, it stated that the “moderation will take longer than previously anticipated given the stronger-than-expected momentum in consumption in the second quarter and the combination of a still-tight labour market with accumulated savings by households”. In the BoC’s mind, longer lags and less sensitivity to interest rates were convincing enough to keep increasing interest rates.

This speaks to the internal debate going on at the BoC. On one hand, the 475 basis point increase in the policy rate since early last year should eventually slow economic growth. But with the economy having surprised to the upside for most of this year, the Bank has had to question whether it has done enough. As we have written about a lot, the strength in consumer demand has caused expectations for core inflation to be stuck above 3% (Chart 2). So, although total CPI has moved to 2.8% year-on-year in June, forward-looking inflation indicators are signaling that the BoC will be hard-pressed to get inflation to settle at its 2% target.